South Africa - Personal

South Africa - Personal

LIKE IT OR hate it, South African investors have had a long affair with tobacco. It could be likened to an addiction. The visionary behind this was Anton Rupert who founded the Rembrandt Group. Without any special favours, special mineral rights or dispensations, Rupert raised capital, built businesses, did strategic deals and carved out a significant position as a South African business that could compete on global terms. To his credit, Rupert always appreciated his minority investors, and made sure the good fortune was spread equitably.

A decade ago, we started buying our first equities in the Coronation Africa Frontiers Fund. Looking back it felt like a lonely time. The Coronation process is one rich in debate, research and interrogation - something our broader team thrives on. Once we started researching companies north of the Limpopo, the opportunities to do this fell away quickly. There weren’t many industry experts, Bloomberg numbers and reports were stale. There just weren’t that many people to talk to with real knowledge and this upped the required margin of safety. We were also attracted to what we knew best. And so tobacco got a lot of attention.

One stock in particular caught our attention - Eastern Tobacco. The Egyptian monopoly cigarette producer was an unloved business trading at mid-single level earnings multiples. Intrinsically, the business had so much going for it - strong cash flow earnings, regulatory barriers to entry, and a growing early stage market in a massive population. But there was a lot not to love.

The business had spent a fortune duplicating production facilities with the intent of relocating its factories. The project had taken longer and cost more than expected, and the production cost line had blown out. Investor interaction was non-existent. There was no communication in English. Government was a controlling shareholder, and the business behaved accordingly. Most frustrating was that the stated strategy seemed to confuse the resilience of the business with the impression that management was responsible for the business successes. And commitments were being made to numerous capital projects that would swallow up free cash flow, leaving minority shareholders with the short end of the stick.

I clearly remember the first meeting in 2008 with the chairman - or what we would call the CEO. It was one of the most surreal encounters I have experienced. Setting up the meeting required a great deal of pushing. I was struck by how busy the site was or, more specifically, how many people were busy on the site, down to the lift operators dedicated to manning the lifts over just three floors. It took an hour to move through security, the reception and waiting rooms, until we finally arrived in the chairman’s office.

And what an office! It wasn’t much smaller than a tennis court sans the tram lines. The walls were wood panelled and, centre stage, was a raised platform on which a massive desk sat, behind which the chairman took court. I had naively prepared a long list of questions which I soon found to be superfluous. For the next ninety minutes, I listened to the interpreter singing the praises of Eastern and explaining why it was such a remarkable business, all while the chairman smoked a massive Cohiba cigar and nodded vigorously in agreement. It was blindingly obvious there were levels upon levels of trapped value. But we had time to uncover it.

We made a modest investment in 2008 which was increased over the years, both in absolute terms by way of value, and in relative terms by way of the size in the portfolio.

While a decade is a long time, it can also be rather fleeting. And in Eastern’s case, much has changed and much has stayed the same.

The cigar-smoking chairman has moved on and his replacement is a good improvement. The government holding company has become less government-like and more institutionalised. There is more English on the website, and shareholder interaction has improved greatly.

The capital sapping projects have been cancelled. Free cash that is generated is paid out as dividends. And more recently, there is a move to change the company structure from a state-owned entity to a joint stock company (like any other) which allows for minorities to appoint directors.

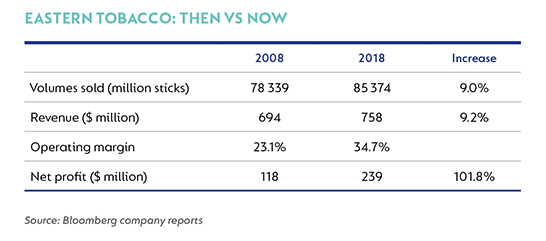

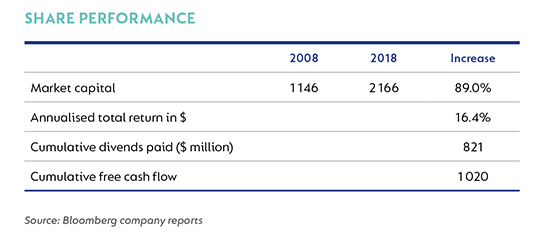

The direct benefit to investors has been the following:

We believe this business is about to enter a new stage in its life. The Egyptian government is set to sell down its holding to just above 50% as part of further institutionalisation of the business. The company today trades at single digit multiples yet is a very different business to the one we met a decade ago. Seldom are we able to invest in a business that is growing revenue and improving margins, and yet trades like an ex-growth company. Eastern is just one of the companies we have journeyed with over the last decade. There are many more similar examples. Here’s to the next ten years.

Disclaimer

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter