South Africa - Personal

South Africa - Personal

Investment views

On the brink

“When the world is running down, you make the best of what’s still around.” – Musician and actor, Gordon Sumner (aka Sting)

- Bond yields are wildly volatile in the Covid-19 economy

- SA is on the brink of a debt trap as the drop in tax revenue bites

- Interim funding from international lenders will be a temporary plug

- Firm policy action remains crucial to SA’s recovery

“When the world is running down, you make the best of what’s still around.” – Musician and actor, Gordon Sumner (aka Sting)

WE ARE ALREADY six months into 2020, a year that truly defies description, with a landscape that still presents as volatile and treacherous. At the beginning of the year, it was hard to find a pessimist in financial markets until the novel corona-virus turned into a fully-fledged pandemic. The subsequent global lockdown sent both the global and local economies into severe recession.

Global monetary and fiscal policy then unleashed a flood of money into the economy, the likes of which has never been seen before, spurring expectations for a quick recovery. Asset prices started to recover in the second quarter of the year (Q2-20) as economies across the globe started to open up from ‘hard lockdowns’. However, concerns about a second wave of infections in developed markets and escalating infection rates in emerging markets threaten to derail the recovery.

THE SOUTH AFRICAN SITUATION

The local economic backdrop is concerning, but valuations were considerably cheaper by the end of the first quarter. South Africa’s asset price recovery was buoyed by better risk sentiment in global markets. The All Bond Index (ALBI) was up 9.9% in Q2-20, but its return remains flat year to date and a paltry 2.9% over the last 12 months. ALBI performance continues to be driven by the performance of bonds in the zero- to seven-year area of the curve, as cash rates have pulled down aggressively on the 275 basis points (bps) of repo rate cuts carried out by the South African Reserve Bank (SARB).

The 12-year-plus area of the curve has continued to underperform due to the deterioration in government finances and increased public sector borrowing requirements. Inflation-linked bond (ILB) performance has been dismal, with the Composite Inflation-Linked Index down 3% over the last 12 months, led again by ILBs in the seven-year plus area. Despite poor index performance, ILBs out to seven years have still generated a return more than cash (2.9%) year to date. Overall, bond yields have had a rollercoaster year and are currently only marginally higher than they were during the ‘Nenegate’ aftermath and considerably lower than during the March sell-off, but still embed a significant risk premium.

Emerging market debt crises have traditionally occurred in countries that predominantly have foreign-denominated debt; face an accelerated decline in their currency, resulting in an increased debt burden that they are unable to service; and an inflationary problem that re-enforces the downward spiral in their currency. South Africa is slightly different in that inflation will remain modest over the next two to three years.

However, due to an incapacitated State, the poor shape of State-owned enterprises, a lack of targeted structural reform and a dearth of political direction, government finances have deteriorated to such an extent that debt service costs are the fastest rising government expenditure item. In the fiscal year 2020/21, the fiscal deficit will register a whopping -15%, the debt-to-GDP ratio will exceed 80%, tax revenue will be down R300 billion and nominal growth will be down 3.5%. Many countries around the world, both developed and emerging, will face a similar reality as the fiscal taps open to soften the fallout from the Covid-19 pandemic.

Unfortunately, due to its poor starting position, the glacial pace of reform implementation and reliance on foreign portfolio flows, South Africa is teetering on the edge of a debt trap; with local public sector borrowing requirements pushing up to almost R800 billion this year, due to the drop-off in tax revenue. Over the longer term, more steps are needed to ensure that the underlying growth engine is restarted through targeted, efficient and transparent investment into the local economy by government and the private sector. In the interim, South Africa will have to rely on funding from international finance institutions (IFIs) such as the International Monetary Fund and the World Bank, and capital markets to keep the ship afloat.

IFI funding is relatively cheap and has little conditionality but will still need to be repaid in foreign currency, while local capital market funding will have to be accompanied by a strong commitment to reel in wasteful expenditure, refocus current expenditure and implement key sector reforms (e.g. energy, labour and transport) in order to increase investor confidence and trust. South Africa has a long history of not delivering on key policies and reforms, which has resulted in the current debt nexus and erosion of investor confidence in the country.

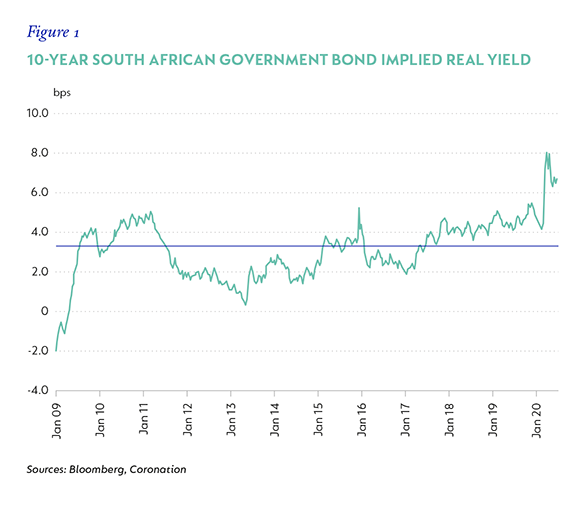

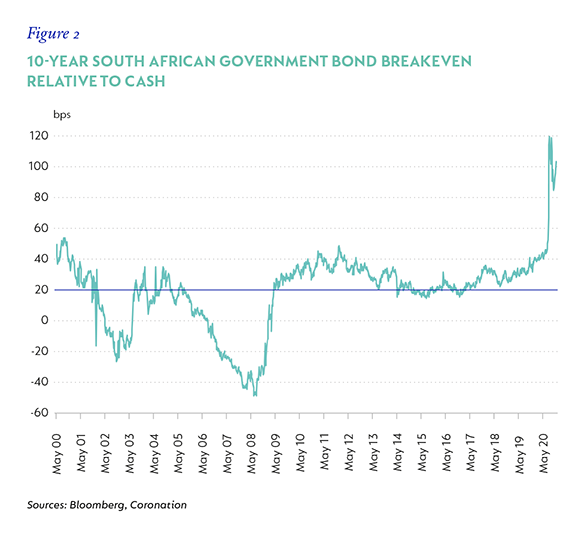

Consumer price inflation will average 2.7% over the next year and 3.5% over the next two years. Following the cumulative 275bp rate cuts since the beginning of this year, the SARB has room to reduce rates by another 50bps over the next three to six months and is likely to keep them at similar levels over the next 12 to 18 months to support the economic recovery. The 10-year South African Government Bond (SAGB) currently trades at 9.5%, which implies a real yield (return after inflation) of 6.6% and a breakeven to cash (the extent to which bond yield can widen before its return equals cash) of 93bps over the next year. In figures 1 and 2, one can clearly see that both the implied real yield and breakeven relative to expected cash remain at very extended levels relative to history and to their long-term average. This suggests that, from a local perspective, there is a significant risk premium in place due to the poor fiscal outlook.

THE GLOBAL OUTLOOK

Globally, bond yields and policy rates are testing their zero bounds. US 10-year yields, which are widely accepted as the proxy for global bond yields, are trading at historic lows. The Federal Reserve Board (the Fed) has injected massive amounts of stimulus through its open-ended quantitative easing programme, and policy rates and bond yields are not expected to move materially away from their current levels at any time soon.

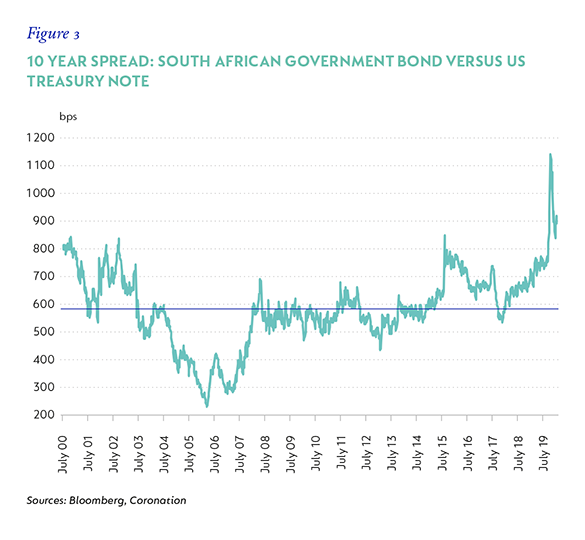

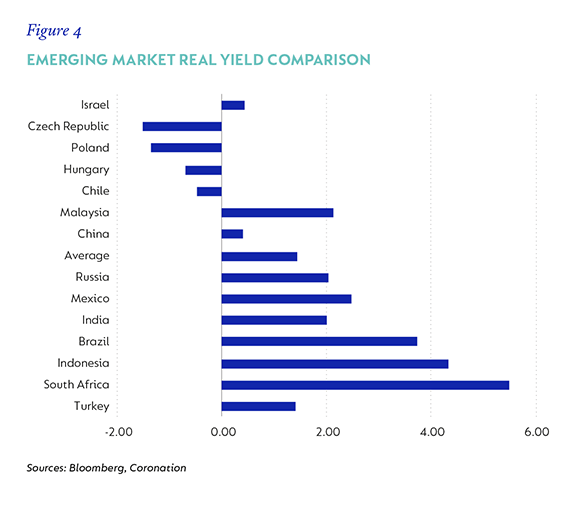

Even if bond yields do push higher due to structural changes in employment and inflation, fair value is not materially more than 1.5% on the US 10-year bond. South African 10-year bonds trade at a spread of 9% above US 10-year bonds which, once again, is considerably above historic levels and the long-term average. If US bonds were to gravitate towards the 1.5% level, unless this is accompanied by a massive inflation shock, the South African spread over US bonds does have a significant cushion to absorb this move, and would still trade at a historically wide spread (Figure 3). Add to this the fact that the 10-year SAGB trades at a significantly wider real yield than its emerging market peer group, and one can see that even from a global perspective, a significant risk premium remains in place (Figure 4).

A VOLATILE CURVE

The yield curve has been as volatile (if not more so) as outright bond yields. South Africa now has the steepest yield curve in the tradeable emerging market universe. The 10-year bond trades 1.7% above the 6.5-year bond, the 15-year bond trades 1.5% above the 10-year bond, and the 20-year bond trades 2% above the 10-year bond. Due to the higher yields on offer in the 10-year plus area of the curve, the inherent breakeven protection in these yields, both relative to cash and inflation, is attractive.

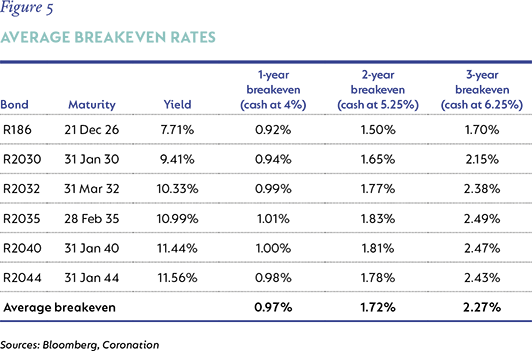

Our base-case assumption is that the repo rate settles at 3.25% over the next six months and stays there for at least the next 12 months. This implies a cash average of 3.35% over the next 12 months. If we assume inflation comes through more strongly and base rates rise more aggressively to average 4% over the next year, this implies a peak repo rate of close to 5% at the end of year one (250bps of hikes). We use similar assumptions over two and three years, and then run a total return analysis to understand how much the various bonds can sell off before their returns equal cash – illustrated in Figure 5

As can be deduced from the table, the 15-year area of the curve offers the most protection. Combine this with the fact that the 15-year point is steeper than it has ever been relative to the 10-year area (1.5% above), the five-year area (4.4% above) and cash (7.3% above), and its appeal increases.

In addition, at the Special Adjustment Budget in June, Finance Minister Tito Mboweni reinforced the point that the National Treasury plans to shorten the duration of its issuance profile to seven to 10 years, suggesting less issuance and hence less supply pressure in the >10-year area of the curve. The intentions set out in the June Budget are ambitious, and the lack of the flattening of the yield curve bears testament to that. However, if the Treasury were able to get just half of its intentions through, the result would still be more positive than current market pricing and the yield curve should enjoy significant flattening. The current valuation of the 15-year point is quite attractive due to its inherent breakeven protection relative to cash and inflation, as well as the negativity priced into its elevated spread relative to shorter-dated bonds. We therefore view it as an attractive relative allocation on the local bond curve.

The fallout from the Covid-19 pandemic will linger for some time to come. In South Africa, the impact will be felt most in a much dimmer growth outlook, which will have a severe impact on government finances. The effects of the very hard lockdown and poor policy choices will weigh heavily on the economy going forward. As it was not well positioned going into the crisis, strong reforms are needed to return the country to a structurally better growth path, although lower interest rates will lend support to the economy through this difficult phase.

SAGBs do embed a decent risk premium, although this premium has reduced slightly post the recovery in Q2-20. As mentioned, South Africa is on the brink of a debt trap and, although promises have been made to restore the country to a more sustainable debt trajectory, the implementation risks remain elevated. The valuation of SAGBs does provide some offset to this, implying that local bonds do warrant at least a neutral allocation in portfolios.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter