South Africa - Personal

South Africa - Personal

Economic views

Half-year stocktake

Shifting growth dynamics and inflation uncertainty

- Economic recovery varies per region, shaped by vaccine strategies and policy support

- The Delta variant of coronavirus is a potential threat, but not yet enough to offset strong recovery tailwinds

- Inflation risk is broadening, but markets are not yet convinced of its persistence

- Stability will be threatened should inflation continue to surprise expectations

VACCINE STRATEGIES HAVE dictated regional growth recoveries. Mid-year stocktaking reveals that the world is recovering fast from the pandemic, but the recovery is starkly uneven, and the dynamics are shifting. Growth leadership passed from China to the US, and more recently from the US to the UK and Europe, as staggered vaccine strategies and degrees of policy support have dictated the pace of each region’s economic reopening. In countries where vaccinations lagged – initially in Europe and now visibly in emerging markets – so has growth, although this should start to converge in the second half of this year (H2-21). The emergence of the Delta variant is an unknown headwind to the recovery, but not yet enough to derail it, as a combination of broadening vaccinations and policy support remains a considerable tailwind.

Accompanying this uneven recovery has been a broad-based surge in inflation in both developed and many emerging economies, where data has surprised to the upside. While rising inflation has generally reflected base-related price normalisation, the surprises were not limited to a strong recovery in affected components. Reopening has seen pent-up demand for both goods and services collide with constrained supply lines that have led to bottlenecks and soaring prices for select goods and services. Also, the extension of income support in some countries has fuelled labour shortages, pushing up wages in some sectors. Base effects and bottlenecks should moderate, but booming asset prices and wage pressures could be more durable, which raise the risk that inflation may be elevated for some time.

While regional variances are stark, the broader shape of the recovery is becoming clearer. Economies with headroom to provide ongoing fiscal and monetary support, accompanied by well-executed vaccine strategies, have recovered first, fast. Those that have not managed to provide either the additional support or that have lagged in vaccine rollouts are still struggling to fully re-open – although many have still benefited from rising global trade volumes and commodity prices. These laggards should move forward in the growth pack as more people are vaccinated, while the leaders are increasingly likely to have inflation and policy uncertainty to manage.

GROWTH OUTLOOK: LAGGARDS TO LEADERS?

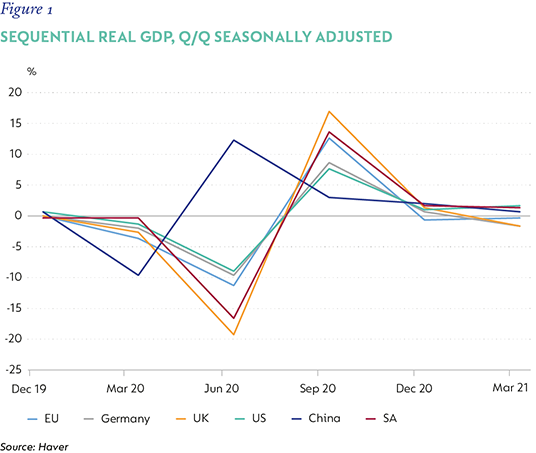

GDP data at mid-year shows that China’s economy peaked in late-2020, and growth is now slowing sequentially. Overall, GDP growth looks set to continue ahead of the pre-pandemic rate, but consumer spending has slowed in line with tighter policy settings and a falling credit impulse. Using JPMorgan forecasts, growth is expected to moderate from 5.3% quarter on quarter (q/q), seasonally adjusted annualised (saa) in the second quarter of 2021 (Q2-21), and from 8.8% in 2021 to 5.5% in 2022, as government refocuses policy from support to deleveraging and de-risking China’s highly leveraged economy.

Figure 1 shows China’s early exit from recession, but fading growth momentum as stimulus fades. Growth has been supported in the US, while the UK and EU suffer a weaker recovery on extended Q1-21 lockdowns.

In the US, growth surged 1.6% q/q in Q1-21, on a recovery that is fueled by full-bodied monetary and fiscal support, and an aggressive vaccine rollout. Specifically, the newly elected Biden-Harris Administration extended income support through both the Coronavirus Aid, Relief, and Economic Security Act and the Emergency Covid Relief Act (passed in December 2020), and then the broader fiscal stimulus package, the American Relief Plan of $1.9 trillion, passed in March 2021. Following an aggressive vaccination programme, the economy has opened, and a large, accumulated cushion of savings has helped to boost spending and employment. The pending passage of the Infrastructure Bill should also give the recovery longevity, as growth moves from consumption to investment.

A similar pattern has played out in Europe. With a hard Wave 2 lockdown in many core countries, and patchy vaccine strategies, the growth recovery in Europe lagged that of the US. However, with initial vaccinations now nearing completion and an accelerated easing in mobility restrictions since June, and opening to tourism from late-July, European GDP growth is expected to accelerate into Q3-21, reaching 5.4% for the year as a whole, before slowing a little in 2022 to 5%.

Importantly, this plan allocates €2 trillion from the EU Budget to member countries, mostly earmarked for spending on green technologies and digitisation, and should boost EU GDP by more than one percentage point through 2022. The relaxation of fiscal rules in Europe as economies recover from the pandemic should also provide additional fiscal headroom and help leveraged economies, like Italy and Spain, avoid a sudden stop in fiscal support and a sudden moderation in growth.

In the UK, an aggressive vaccination drive has been somewhat hobbled by a slightly less smooth reopening strategy. Nonetheless, GDP growth, after contracting again in Q1-21, is set to rebound strongly in Q2-21, as monthly tracking data points to an increasingly strong rebound.

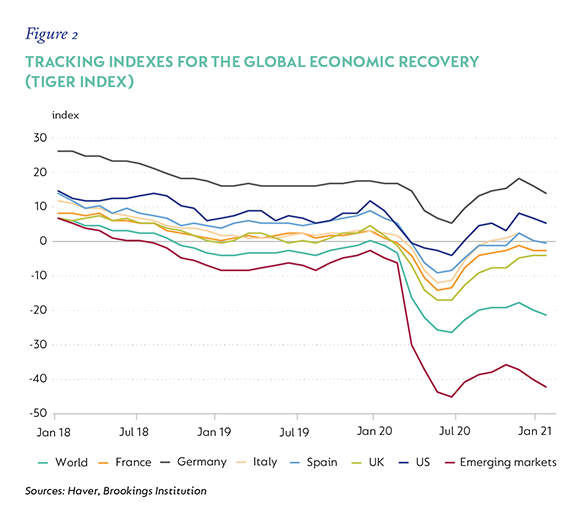

Elsewhere – and most notably in emerging markets – vaccine strategies have lagged, and so has growth. This is in part a function of local logistics, and in part the inability to secure enough stock of vaccines (not to mention individual supply issues), as developed market strategies took precedence. While the evolution of variants is likely to be more damaging in countries where there have been limited vaccinations, emerging market vaccinations are now gathering momentum. Notably, vaccinations in Brazil, Turkey and India have picked up visibly in past weeks, supporting a stronger growth outlook in H2-21 (Figure 2).

As these economies are able to open, so too should the recovery in previously constrained services sectors begin. Global growth is set to converge in H2-21 and into 2022. JPMorgan forecasts global growth of 6.4% in 2021 and 4.5% in 2022.

VACCINATIONS AND VARIANTS

The evolving virus remains a persistent threat. Available information shows that the newly emerged Delta variant of the coronavirus is significantly more transmissible than its predecessors, but it is not yet clear whether, outside of the higher infection rate, it is more deadly. Also, people who have been vaccinated seem to suffer fewer extreme symptoms and do not require hospitalisation. That said, the higher transmissibility means that for countries where vaccination rates are low, the risk of hospitals being overwhelmed and associated deaths rising meaningfully is much higher. Emerging markets are very vulnerable, and there remains considerable risk that low vaccination rates will further delay recoveries and impose longer-term scarring on weakened underlying economies.

There is not a lot of reliable information about the threat posed by the Delta variant in Africa, where vaccinations have been the lowest and where testing rates are, perhaps, not as good as elsewhere in the emerging market universe. As the situation develops, it highlights the need for more aggressive and committed vaccine strategies in countries where these have, so far, been poor.

INFLATION RISK REMAINS ELEVATED

The economic reopening has been accompanied by a broad-based surge in inflation. The initial increase was widely forecast and well anticipated by markets as base- and fuel-price-related adjustments emerged visibly from April and May. Prices that were depressed by the pandemic, such as in the tourism and other services sectors, are now normalising, but many have some way to go, given the growth dynamics outlined above.

However, increases have not been limited to base effects. Bottlenecks have emerged where pent-up demand has created shortages for inputs and final goods alike, exacerbated by rising commodity prices. Policy-driven income support has seen labour shortages emerge, mostly in hospitality, but wage growth is also becoming more evident across other sectors, mostly in the US. Developed market business surveys are now, almost uniformly, highlighting price pressures, while housing markets are also heating up and rentals are starting to rise in key economies. This means that it’s not just relative prices that are rising, but the broader base, extending to housing and wages (most visible in the US), which suggests a more durable upside risk to inflation (Figure 3). This risk is potentially compounded by a seeming tolerance of key central banks – notably the Federal Reserve Board (the Fed) and the European Central Bank (ECB) – of higher inflation.

The slower growth recoveries in emerging markets have not immunised them to rising price pressures. Inflation surprises in Turkey, Mexico, Brazil and Russia have already prompted their central banks to start raising policy rates.

It is possible that a shift in price pressure from goods to services will see inflation peak and then slow, as bottlenecks unravel and labour shortages ease, but the broadening growth dynamics materially increase the risk of inflation persistence. Labour market dynamics in developed economies will play an important role in determining the duration of price pressures, but most visibly and critically in the US and to a lesser degree, the UK. By September, most furlough schemes will end, schools will be reopening, and vaccinations should be well advanced in most economies. If this prompts stronger labour participation and eases pressure on wages, markets will reprice inflation and policy uncertainty.

THE DRIVER IS POLICY

Policy settings have also reached a sort of ‘half-time’ review, and decisions over their direction will further shape the recovery. In developed markets, fiscal support has broadly been extended into 2022 and, in some cases, beyond. There is some lingering uncertainty as to the US proposal of additional fiscal packages of $4 trillion over 10 years, but the EU has acted firmly, with the urgent deployment of the Next Generation EU recovery plan. This leaves the weight of policy adjustment to monetary policy, and, here too, the outlook is increasingly uncertain. The Fed’s new ‘flexible average inflation target’ implies tolerance for inflation to overshoot the target for limited periods, while the ECB is currently reviewing its mandate. But, when the Fed met in June and delivered a more hawkish statement in the face of strongly higher inflation, the Bank of England and the ECB, no doubt, took note. Markets made a sharp adjustment to policy rate expectations at the time, but have since shifted gear again, apparently again less concerned about inflation risk. But more persistent upside surprises in inflation, driven by wage pressure, most at risk in the US and UK, could severely challenge this stability in coming months. +

Disclaimer

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter