South Africa - Personal

South Africa - Personal

The Fund returned -4.7% during the third quarter of 2023, 1.7% behind the -2.9% return of its benchmark, the MSCI Global Emerging Markets (Net) Total Return Index. The Fund is behind the benchmark year to date (by 1%) but 4.7% ahead over the last year. Over longer-term periods, performance is still negatively affected by the tough period experienced from April 2021 to mid-2022, with the result that over five years, performance is 2.0% p.a. behind the benchmark. Since inception, the Fund has delivered 0.3% p.a. outperformance. We believe that our investment process is capable of delivering outperformance in excess of 3% p.a. over meaningful periods of time and have exceeded this for most of the Fund’s 15-year history. During the almost 13-year period from inception in July 2008 up until 31 March 2021, the Fund had, in fact, outperformed the market by 2.4% p.a. We believe that our investment process is capable of delivering outperformance in excess of 3% p.a. (before fees) over meaningful periods and are very focused on returning the Fund’s long-term performance numbers to this level.

The biggest contributors to Fund performance during the quarter were two of the Russian stocks that had been written down to zero in the aftermath of Russia’s invasion of Ukraine. The value recovery in Magnit amounted to a 2% positive impact (both absolute and relative, as the index has removed all Russian stocks) and was achieved partly due to action taken by Magnit early during the quarter. Magnit received permission from regulators to buy back shares from foreign shareholders at a discount to the share price at the time on the Moscow Exchange. The company needed this permission because, even though it had adequate financial resources for the buyback, the foreign shareholders had to be paid outside Russia in US dollars, which was not easy to navigate within the framework of the existing sanctions. While many foreign shareholders were unable to take part in this offer, due to the tight timeline to tender shares, we were able to meet the deadline and sell all the shares in Magnit in the Fund. The other Russian stock sold during the quarter was Yandex, with execution taking place via the over-the-counter market at a similar discount to Moscow prices (50%) to that achieved in the Magnit tender. Yandex contributed 0.9% to return (again, both absolute and relative) in the quarter, taking the total Russian positive attribution for the quarter to 2.9%.

These sales, together with the sales of X5 and TCS earlier in the year, mean the total amount recovered so far from the Russian holdings has contributed 3.7% alpha this year. There is no timeline for a resolution to this conflict, and we believe strongly that realising reasonable value, even at these discounts, is in the best long-term interest of investors. Part of this reasoning comes down to opportunity cost: emerging market valuations are very low right now in both absolute and relative terms, with the result that we are finding significant value today, as reflected in the current 85% upside to fair value in the Fund. We continue to explore avenues to sell the remaining holdings in Moscow Exchange, Lukoil and Sberbank. At current spot prices on the Moscow Exchange, these three holdings would total approximately 4.3% of the current Fund value. A recovery rate of 50% on these holdings, in line with what has been achieved so far, would therefore add another 2.1% of recovery, and take the total Russian recovery contribution to approximately 5.8%. As context, the negative attribution from Russia in 2022 was 7.2%, which accounted for all of the Fund’s relative underperformance in 2022.

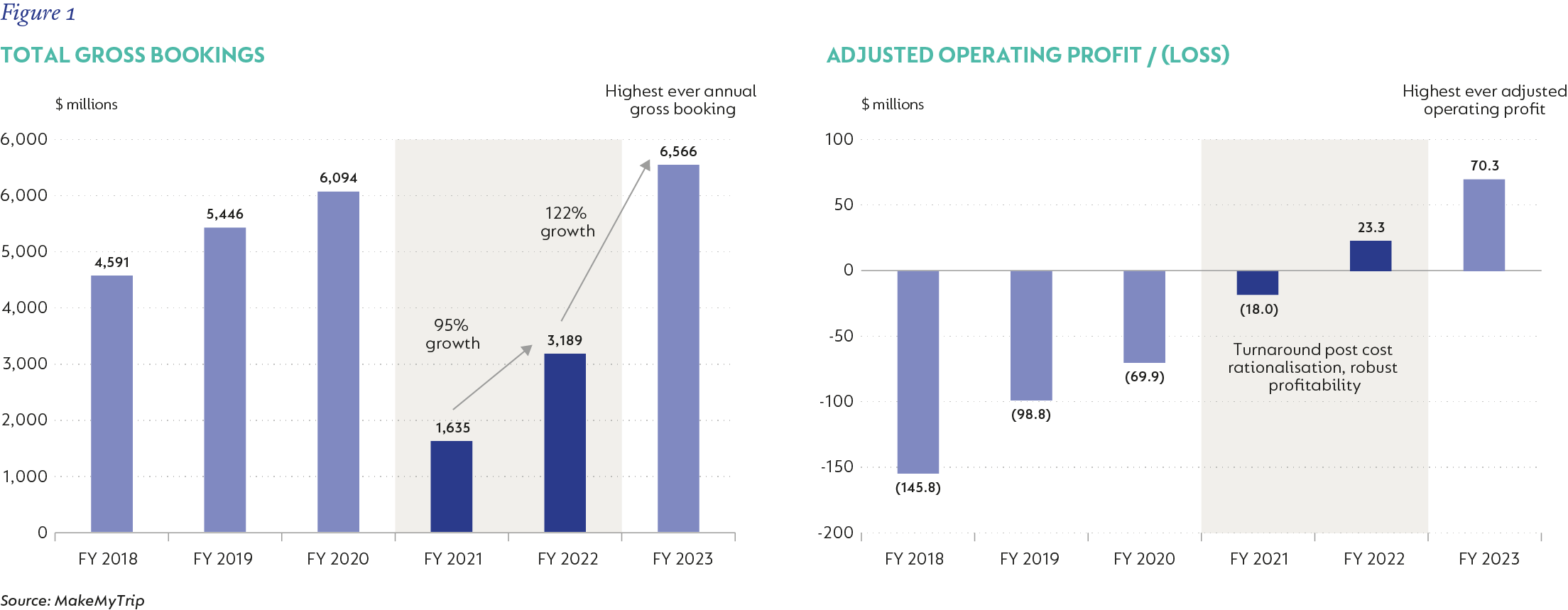

The third largest contributor after the two Russian holdings was MakeMyTrip, an Indian online travel agency, which returned 50% in the quarter for 0.8% alpha contribution. The travel sector was decimated during the Covid pandemic but is recovering strongly now with several consecutive quarters of robust growth, which is driving the share price upwards, as is profitability. Air ticketing revenue already exceeds pre-Covid levels for the comparable quarter prior to the onset of the pandemic, in spite of take rates having declined slightly since then. Hotels and packages revenues are also close to pre-pandemic levels. What has really turned for the company has been the big improvement in profitability, with marketing spending having halved from the levels they used to spend a few years ago. This, together with good cost control on operations, has allowed the company to post three consecutive quarters of operating profits and also positive operating cash flow in the latest quarter.

Also, within the internet sector, Pinduoduo (ecommerce, China) returned 42% and contributed 0.6% alpha to the Fund. Operating results have been excellent – the company’s second-quarter revenue was up 66% year on year, more than 50% higher than the market growth rate as a whole and beating consensus estimates by 20%. From nothing six years ago, the company has reached 15% market share, predominantly at the expense of Alibaba. Despite experiencing some gross margin pressure from higher fulfilment costs, Pinduoduo saw limited impact on its overall operating margins thanks to excellent cost control, particularly in selling and marketing. The company is also converting its earnings fully into cash. The results of Pinduoduo are just one example of the large disconnect between the narrative on China and the operational results that many of the Strategy’s China holdings are producing. Pinduoduo, as with any investment, is not without risk – the company is expanding rapidly internationally with its TEMU offering (low-cost ecommerce merchandise shipped from China) and spending large amounts promoting this offering. However, for now, this division is a small part of the potential company value and should TEMU fail to make headway against Shein, Shopee and other similar offerings, it will not have a material impact on our estimate of the company’s intrinsic value. At the same time, there could be material (additional) upside if Pinduoduo succeeds in its TEMU strategy.

The biggest detractor in the quarter was Delivery Hero, which took 1% off quarterly relative performance. The key driver of the share price decline was somewhat weak quarterly results, albeit with negative currency movements in operating countries (relative to the euro) playing a role in this regard. The company continues to grow group revenue in the double digits (and in many countries by >20%), has already made good progress towards being profitable and is in discussions to potentially sell some (unprofitable) Asian assets. The company’s equity is substantially undervalued in our view - applying a 10x multiple to our free cash flow estimates for next year generated by the company’s Korean business alone (less than one-third of group revenue) would give you the current market value of its equity. This is a conservative multiple for a dominant player in the very attractive Korean market and also ignores Delivery Hero’s other substantial assets in more than 70 countries.

PEPCO also took a percent off alpha following a large share price decline in the past few months. We continue to do detailed research on PEPCO, with a view to ultimately challenge our conclusion that nothing has structurally and materially changed. The company has definitely made missteps (so-called own goals) that we can identify (expanding store footprint too quickly, losing focus on cost control, etc.), but the size of the opportunity within Eastern Europe (and select Western European markets) remains significant, and the offering of PEPCO (value retail with a focus on general merchandise and household goods) remains compelling. We also have high regard for the Chairman/former CEO, who, in turn, has a significant part of his wealth invested in the company. With the share price decline, the company now trades at around 12 times forward earnings, and we have added to the position to retain its size at around 1.5% of Fund.

Other detractors were food retailer Sendas in Brazil (-15% return, -0.4% alpha impact) and Macau hotel and casino operator Melco Resorts (-19% return, -0.4% alpha impact). Worth noting for the quarter was the completion of the merger between HDFC and HDFC Bank, with the Fund receiving shares in the bank upon completion. HDFC Bank is now the second largest position in the Fund (5.0%) as a result of the merger.

A new buy for the quarter was Turkish hard discount retailer BIM (1% at quarter end). Whilst we have long believed that BIM is a great business, we sold it entirely one and a half years ago after the country’s authorities resorted to unorthodox monetary policy, which led to inflation peaking at close to 90% year on year. Since winning re-election earlier this year, President Erdogan has appointed market-friendly individuals to head the Central Bank of Turkey as well as the Ministry of Finance and has largely refrained from his previous rhetoric. The result is that interest rates have gone up substantially, and the economy is stabilising. Through all this, BIM continues to execute excellently operationally, with discount food retail benefiting from high inflation as cash-strapped consumers trade down to more affordable retailers. BIM now trades on 10 times next year’s earnings with a 4% dividend yield.

The Fund also purchased a new position in India, TVS Motors (0.5% at quarter end). TVS is a meaningful player in the two-wheeler scooter/motorbike market in the country, with the third-largest market share in domestic sales and the second-largest export market share. In an otherwise very expensive Indian market, TVS is relatively undervalued and offers an IRR in the high teens.

Finally, at 4 times forward earnings and offering a 16% dividend yield, the Fund also bought a 1.4% position in Petrobras, which we had sold out of last year. We also have almost 4% in aggregate in the two privately-owned and run (not State-owned) Brazilian oil “juniors” PRIO and 3R Petroleum, taking total weight to the Brazilian oil sector to around 5.4%.

There were several sells in the Fund, too (aside from Magnit and Yandex), the biggest being Chinese food delivery platform Meituan (1.3% position at the start of quarter). We also sold Total Energies (1%) Anglo American (0.9%), ENI (0.9%) and Zomato (0.5%).

OUTLOOK

The Fund is very attractively valued today in our view, with the weighted average upside of the stocks in the Fund being around 85%, well above the long-term history in the low 40s. Furthermore, the weighted average IRR (an internal measure of potential annual return over a five-year period comprising 5-year earnings growth, annual dividend yield and a re/de-rating) is a very compelling 24% p.a. - close to an all-time high.

Note: This is the US dollar fund

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter