South Africa - Personal

South Africa - Personal

The Fund returned +15.4% in the final quarter of 2022 (Q4-22), outperforming the benchmark MSCI Emerging Markets (Net) Total Return Index by 5.7%. For the year as a whole, the Fund returned -28.3%, underperforming the benchmark’s -20.1% return by 8.2%. Naturally, this underperformance is disappointing and was driven entirely by the Fund’s exposure to Russian assets, all of which were written down to zero in the aftermath of Russia’s invasion of Ukraine and the resultant imposition of sanctions on the country. As we have stated previously, our view is that these written down assets have significant real value, and this view is supported by current market prices trading in Russia (with good trading volumes). We hope to realise value in the future from these holdings when the situation normalises.

The near-term improvement in performance means that a number of the longer-term performance numbers that had turned negative after a tough 2021 and early 2022 have started to improve significantly. Over five years, for example, the Fund has now underperformed by 3.8% p.a. (which whilst still being very disappointing, had reached almost 5% p.a. underperformance in March 2022). Since inception, the Fund has returned 2.3% p.a., ahead of the benchmark’s 2.0% p.a. return. We believe the Fund holds a collection of very undervalued assets, and we look forward to further improvement in the longer-term numbers.

There were significant developments over the past few months in two of the countries (China and Brazil) to which the Fund has material exposure. These developments ended up having an impact on the Fund’s Q4-22 returns. Arguably the biggest news in Emerging Markets was the effective end of China’s isolation from the world – with the unexpected (in terms of timing and scope) easing of “zero- Covid” protocols in the country. Having secured his position as leader of the Chinese Communist Party for a third term, and with the country facing the first widespread protests by the population since 1989, it appears that Premier Xi Jinping eventually realised the futility of continuing with the zero-Covid policy and allowed local and provincial governments to decide how to deal with Covid in their areas, which eventually resulted in the huge testing and quarantine system breaking down astonishingly quickly. China has even moved to end quarantine for international visitors and its own citizens can now freely travel in and out of the country for the first time in almost three years.

Heading into Q4-22, the Chinese market had underperformed other large Emerging Markets significantly as investors grew increasingly sceptical about China’s appeal as an investment destination, with many even concluding that China was “uninvestable”. The regulatory interventions we saw in many sectors – education and technology in particular – coupled with a prominent entrepreneur being “cut down to size”, meant that Chinese stocks were priced at a substantial discount to peers in other regions. The internet-related stocks, in particular, rebounded sharply as it became apparent that China would be reopening to the rest of the world far quicker than people expected and many of these stocks had been badly hampered operationally by zero-Covid. Statements from Beijing that the regulatory interventions were coming to an end also assisted. Even after the significant recovery in Chinese equities, we believe that many are still significantly undervalued in our view, with a number of holdings still having upside in the 50-100% range.

The largest contributor to the Fund’s relative performance in the quarter was the Naspers/Prosus position, which returned 31% and provided 1.5% of relative outperformance/alpha. Even deducting the negative impact of not owning any Tencent directly (Naspers/Prosus derive the bulk of their NAV from Prosus’ Tencent stake), the overall impact from these stocks was still a net +0.8%. Just behind Naspers/Prosus was Tencent Music Entertainment (TME), which returned 103% (its share price more than doubled) and also provided 1.5% of alpha. TME was actually the Fund’s 2nd largest detractor in 2021: this is not an uncommon occurrence. Due to our long-term approach (whereby we often don’t sell and even add to positions as a share declines), a big detractor in one year is often a big contributor in the next year or two. TME’s closest Western equivalent would be Spotify and we have written previously about why we like TME – low penetration of music streaming in the country and significant opportunity to monetise existing customers. This, coupled with a decent social media business (although the main attraction for us is the music streaming business), and valuable stakes in listed businesses like Spotify, Warner Music Group, and Universal Music Group meant that TME was trading on 7x 2023 earnings (ex-cash and listed assets) at the beginning of the quarter despite having years of significant earnings growth ahead of it. Even with the doubling in the share price, it remains one of the most attractive internet assets in our investment universe and hence a top 10 position in the Fund (2.5% position).

Other material positive contributors to relative performance were AngloGold, which returned 40% and provided +0.8% alpha, as well as Delivery Hero (+29% return, +0.6% alpha) and Airbus (+36% return, +0.6% alpha).

Partly offsetting China’s positive impact on the Fund was Brazil (-1.4% relative detractor in total), which did poorly in the quarter after Lula da Silva won the presidency in a runoff against the incumbent Jair Bolsonaro at the end of October. Initial signs from the incoming administration suggest a loosening (at the margin) of the fiscal taps in spite of Brazil’s government debt metrics looking quite poor. Also likely is greater use of the government’s control of Petrobras to the detriment of minority investors, with a combination of interference in pricing (away from benchmarking against international prices), a reduction in dividends and/or an increase in capital expenditure. For these reasons we sold the remaining position in Petrobras (which we had consistently been reducing in the past few months) in December. For the year as a whole, Petrobras was actually the 2nd biggest positive contributor (after Sendas, the Brazilian cash and carry retailer), having returned large dividends to shareholders (which in turn made up the bulk of its +54% total return for the year), but in our view the investment case has now changed, and very much for the worse.

Several Brazilian and broader Latin American (Latam) stocks feature prominently in the detractors for the quarter. The largest of these was dLocal, a pan-Latam payments processor that returned -25% and cost -0.6% of relative performance. A recent new buy Petz (a premium pet-related retailer in Brazil) returned -36% and cost -0.4% alpha, whilst the three financial services holdings XP (a brokerage), PagSeguro (fintech), and Nubank (digital banking) cost a combined -0.9% alpha. Other than the zero weight in Tencent mentioned above, the only other top 5 detractor that was not Latam-related was Coupang, a Korean e-commerce retailer that returned -12% in the quarter and cost -0.4% alpha.

Even though the upside to fair value (FV) for the Brazilian holdings is significant (130% upside to FV on a weighted average basis), we are being measured in the Fund’s overall Brazilian exposure, having learnt from past experience (2015) the damage that can be done by Brazilian politicians to both the economy and the currency. In this regard, the Fund’s overall Brazilian exposure is 12.5%. Of this, MercadoLibre is the largest position (3.5%) with significant operations outside of Brazil, so this isn’t pure Brazilian exposure (the same would hold true for another Strategy holding – Ambev). Part of our investment case for MercadoLibre is also structural in nature (increasing penetration in both e-commerce and fintech in Brazil and broader Latam), which provides some protection against a potentially poorer economic outlook. The 2nd largest Brazilian holding, Sendas (cash and carry food retailer), a 2.4% position, is very much economically insulated – it typically is a beneficiary (market share gainer) in tougher times and, in addition to this, is partly driving top-line growth through new store roll-out, and driving both top-line and profitability through conversion of acquired hypermarkets into cash and carry stores, with both of these factors being independent of the economy.

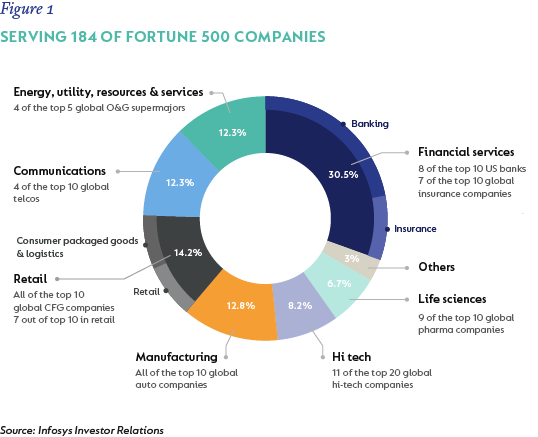

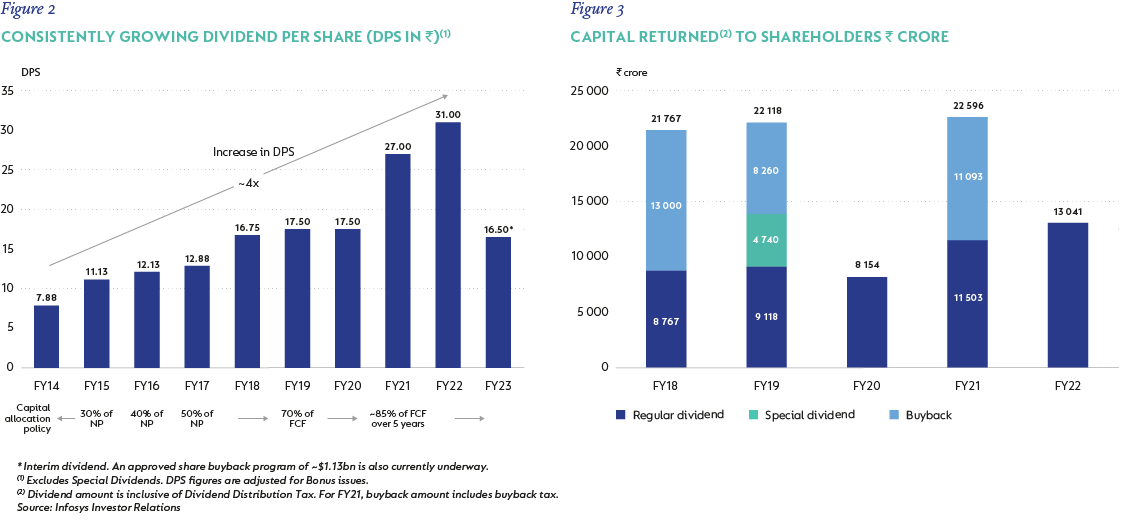

There was only one new outright buy in the quarter, with the purchase of a 0.5% position in Indian IT outsourcer Infosys. We have owned Infosys a few times in the past and the purchase was primarily due to the share starting to offer good upside and being attractive on a risk-adjusted basis after it sold off by around a third from levels reached earlier in 2022. We believe Infosys, like its Indian counterpart Tata Consultancy (TCS, 1.4% of Strategy), offers a valuable service in the global outsourcing industry as medium to large corporates upgrade their IT infrastructure, digitise their businesses and increasingly move to the cloud. Infosys is the second largest of the Indian IT giants (after TCS) that have taken significant market share from Western peers and boast a wide array of global businesses as its customers (Figure 1), with a consistent track record of growing earnings and cash flows, while returning cash to shareholders via dividends and buybacks (figures 2 and 3).

The lack of new buys is not indicative of low portfolio activity, as there were some material changes in position sizes for existing holdings. We added 1.2% to the FEMSA holding to take it close to a 2% position at year end. FEMSA is a Mexican holding company with the country’s largest convenience store chain (Oxxo) as its main asset. Additionally, it owns 15% of Heineken and a 47% stake in Coca Cola FEMSA, the largest bottler of Coke products in Latam. FEMSA has been trading at an increasing discount to the value of its underlying (high quality) assets, having traded at a premium for most of the decade prior to the beginning of 2020. We also added 0.6% to the Pinduoduo (#3 e-commerce operator in China after Alibaba and JD.com) position before the share price appreciated significantly, and we kept the exposure to oil from falling materially after the sale of Petrobras by increasing the exposures to 3R Petroleum (Brazil) and Total (global multinational with 74% of production from Emerging Markets) by 0.5% each. Other notable position size increases were Indian Online Travel Agency MakeMyTrip (+0.4% increase) and Asian insurer AIA (+0.3% increase). The above buy and the position size increases were funded by selling the likes of Petrobras (a 2.2% position at the beginning of the quarter) and trimming of AngloGold and Housing Development Finance Corporation (India).

Aside from Petrobras, the most notable sale in the quarter was Alibaba (a 0.9% position at the end of September). Although it appears very cheap on valuation metrics, our conviction in the long-term moat around the business has deteriorated over time (and the position size had accordingly already been reduced some time ago). Their cloud business, whilst the largest in China, is up against significant competition from the likes of Tencent and Baidu, plus several other government-backed cloud infrastructure providers. The core e-commerce business continues to lose market share to JD.com, Pinduoduo and other players that are moving into e-commerce like ByteDance (owner of Tiktok). Finally, the regulations passed on its fintech lending business, Ant Financial, have greatly increased its capital intensity and therefore decreased potential returns for shareholders. With most other Chinese internet assets looking exceptionally cheap and not facing these headwinds, we used the proceeds to rather concentrate our e-commerce exposure in the higher conviction names: JD.com (5.8% of Strategy) and Pinduoduo (2.1% of Strategy).

The weighted average upside in the Fund remains very attractive in our view (around 75%), as does the 5-year IRR (annual 5-year earnings growth + annual dividend yield, adjusted for a re/de-rating from current levels) of 19% p.a. The Fund, as is typically the case, looks very different to the Index (active share of 87% currently and 47% in off-benchmark exposure) and these 2 factors combined bode well for future absolute as well as relative returns in our view.

Disclaimer

SA retail readers

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter