South Africa - Personal

South Africa - Personal

Optimum Growth declined 0.6% in the first quarter of 2021 (Q1-21), yet we believe that the collection of assets held by the Fund still offers compelling, long-term risk-adjusted returns with which to deliver on its goal of compounding capital well ahead of inflation. Over the past five years, the Fund has generated a positive rand return of 11.1% p.a. over 10 years, a return of 16.2% p.a. and since inception over 20 years ago, 14.3% p.a.

The Coronation Global Emerging Markets Fund returned 2.4% in Q1-21, 0.1% ahead of the benchmark MSCI Emerging Markets (Net) Total Return Index. Over the last 12 months, the Fund has returned 64.1%, 5.8% ahead of the benchmark’s return. The very high absolute returns from both the Fund and the benchmark should be seen in the context of the market selloff during March 2020, the early stages of the Covid-19 pandemic, from which the markets subsequently recovered very strongly. Over two years, the Fund has outperformed the benchmark by 4.8% p.a., over five years by 1.7% p.a. and over 10 years by 1.6% p.a. Finally, since inception, the Fund has returned 6.9% p.a., which is 2.4% p.a. ahead of its benchmark. We are pleased with this level of outperformance and continue to believe that focusing on higher quality undervalued assets, and being disciplined in buying them at an attractive margin of safety (and selling them when they are expensive), will generate outperformance for our investors over meaningful long-term periods of time.

Optimum Growth

The largest positive contributors to the performance of Optimum Growth in the quarter were Naspers (+15%; 0.49% positive impact on Fund performance), Alphabet (+20%; 0.45% positive impact) and Tencent Music Entertainment (+10%; 0.35% positive impact). The Fund incurred unrealised losses on a collection of put option and short index positions that provided valuable protection historically but detracted from performance this quarter due to a buoyant market. Collectively, these put options and short index positions had a 0.7% negative impact during the quarter; however, they continue to provide the Fund with protection should there be a market selloff. Outside of this, the other notable negative detractors were Unity Software (-34%; 0.38% negative impact on Fund performance), our physical gold position (-9%; 0.34% negative impact) and the London Stock Exchange Group (0.28% negative impact).

Optimum Growth ended the quarter with 77.8% net equity exposure, roughly 5% higher than at the end of December 2020, as we found compelling equity opportunities.

Notable buys/increases in position sizes during the quarter were Nintendo, Porsche and Vinci.

Nintendo is a gaming company founded in 1889 as a Japanese playing card business but moved into video games in 1977. It has a long history of releasing successful video game titles, and it owns leading franchises such as Super Mario, The Legend of Zelda, Animal Crossing and Pokémon. Nintendo creates both the games and the hardware on which these games are played, which have often driven innovation in the gaming hardware space. The company is obsessed with quality and, as such, has been slower than its peers in monetising its world-class intellectual property (IP). This provides Nintendo with a significant opportunity, and there have been some positive indicators that the business will take advantage of this opportunity. The business's new CEO (since 2018) appears more flexible and willing to open monetisation avenues compared to his predecessors, and this approach is evidenced by the company’s more aggressive moves into film, theme parks and mobile games – all-important monetisation touchpoints for its IP. We believe the business is underearning versus its long-term potential and currently trades on 17 times our estimate of 2022 earnings, which should continue to grow at a high single-digit rate and is further supported by an approximately 3% dividend yield.

Porsche is a holding company, with its major assets being its 53% ownership in carmaker VW common stock. VW is the second-largest auto manufacturer globally and owns brands such as VW, Audi, Porsche and Lamborghini. We are positive on VW's underlying business, with a key element of the investment case being the business’s transition from an internal combustion engine auto manufacturer to an electric engine auto manufacturer. Management is confident that in this transition, notwithstanding huge investments ($86 billion between now and 2025), electric vehicle sales growing in the mix will not be dilutionary to margins. Based on our financial year 2022 estimates of free cash flow (FCF), VW is trading on an approximate 8% FCF yield. Porsche is then trading at a 24% discount to its shareholding in VW, which we don't believe is fundamentally justified.

Vinci is one of the world's largest concessionaires and construction contracting companies. It owns irreplaceable, high-quality toll roads (with a non-commuter focus), with high visibility due to the long-term nature of the concession contracts. The business also operates a collection of airports, which are currently under pressure due to the travel disruption caused by Covid-19, but which we believe are still attractive assets that should rebound and be supported by the continuing structural growth trend of leisure travel. Finally, Vinci has a highly efficient and risk-control-obsessed building contracting business that contributes 80% of group revenue but 24% of net income. More recently, the company acquired a business that gives it exposure to renewal energy concessions, which are expected to grow rapidly in the future. Due to the nature of its customer contracts, Vinci is a business that should deliver highly visible earnings and FCF, driving healthy double-digit total shareholder returns in hard currency, which is attractive, especially considering the inflation-linked nature of earnings.

Our negative view on global bonds remained unchanged, as a large portion of developed market sovereign bonds offers negative yields to maturity, with the follow-on effect that most corporate bonds also offer yields that do not compensate for the risk undertaken. Only 1% of the Fund is invested in bonds, which is largely made up of a 0.51 % position in L Brands (owner of Victoria's Secret) corporate bonds.

The Fund also has c.1.85% invested in global property – largely Vonovia (German residential). Lastly, the Fund has a physical gold position of 3.4%, a 1% holding in AngloGold Ashanti and a 0.8% holding in Barrick Gold Corp, the largest gold miner globally. The gold price is down approximately 13% in US dollars year to date, but we continue to hold the position for its diversifying properties in what we characterise as a low-visibility world. The balance of the Fund is invested in cash, primarily offshore. As has been the case for many years, the bulk of the Fund (over 90%) is invested offshore, with very little exposure to South Africa.

The markets remain volatile as the Covid-19 pandemic continues to cause disruption around the world, with various governments responding in different ways; with some achieving rapid success in their vaccination drives while others falter. This will potentially result in a world where the paths to normalisation worldwide are quite different, which can continue to create a disruptive operating environment for many businesses. However, the pandemic will only end when the world is vaccinated at an individual country level, and thus, notwithstanding real issues surrounding equitable access to vaccines, there is hope that access will improve in the coming months. This future scenario, however, still has many unknowns associated with it, creating an environment characterised by uncertainty and disruption.

As the outlook for the future remains uncertain and hard to predict, we take comfort in the fact that the Fund holds a collection of businesses that we feel are attractively priced and can operate in what we deem a highly complex and fast-changing environment. Also, because the Fund is a multi-asset flexible fund, we have access to additional tools to take advantage of dislocations in the market, with the increased equity exposure being an example.

As vaccines roll out across the world (with initial real-world data indicating they are working well to reduce the hospitalisation and fatality risks associated with Covid-19), there is reason to be optimistic that the devasting effects of the pandemic are closer to ending. However, there remains uncertainty as to when the entire world will reach a level of vaccination that allows life to return to normal. However, against this backdrop, we remain positive on the Fund's outlook, which has been built bottom-up, with a collection of attractively priced assets providing diversification in order to achieve the best risk-adjusted returns going forward.

Global Emerging Markets

The biggest contributor to outperformance (alpha) in the quarter was the Naspers and Prosus combined position, which returned an effective 13% in the period. Naspers and Prosus are owned in preference to owning Tencent outright, due to the discount at which Naspers trades to the look-through value of its stake in Prosus and the onward discount at which Prosus trades to the value of its stake in Tencent. At the beginning of the year, these discounts effectively allowed a Naspers shareholder to own Tencent at an approximate 40% discount to the value of its Tencent stake alone, with all other assets valued at zero. During the quarter, the discount narrowed a few percentage points (Naspers outperformed Tencent by about 8%), and this, coupled with the overweight position, contributed close to 1% of alpha alone. Not holding Tencent directly cost 0.3% of alpha, resulting in a net alpha contribution of 0.7% overall. Management of Naspers and Prosus has undertaken to unlock this discount over time and is heavily incentivised to do so.

Another significant contributor was a member of the Tencent family – Tencent Music Entertainment (TME; 57% held by Tencent). TME rose by 65% from the start of the quarter to 23 March, but then declined precipitously over the next three days and did little thereafter, to end only 6.5% higher. The proximate cause for this decline was the massive unwind in many stocks caught up in the much-publicised Archegos fiasco. TME was a 2.4% position at the start of the quarter, and we sold regularly as the share price increased until, at one point in March, the position size was down to 1.3% of the Fund as a result of the sales. In our view, there was no significant change in the underlying value of the business after the share price sold off, so we bought back sufficient stock during the tumult to leave the position size at quarter-end almost unchanged at 2.3% of Fund. The realised return from TME for the Fund was almost double the reported 6.5% price appreciation and the overall alpha contribution amounted to 0.7%.

Brazilian retailer CBD also contributed, in a positive example of value unlock by management. At the turn of the year, the Fund held a 2.0% position in CBD, whose ADRs* were priced at $14.30. This was over a third lower than the share price at the start of 2020. Although part of this was driven by the decline in the currency, this was one of the few food retailers under our coverage to see such marked share price weakness, particularly when one considers that food retailers faced among the least business disruption worldwide as ‘essential service providers’, and much of the spending that would otherwise have taken place in restaurants and bars migrated toward them. CBD’s management team, with whom we have engaged extensively over the years, announced and carried out a plan to separate the business into its two constituent parts in order to realise better value for the underlying parts of the business.

This separation was announced last year but only came to fruition in early March after the business received all the requisite regulatory and shareholder approvals. At this point, CBD spun out its lucrative cash-and-carry business, Assai, to shareholders, with the core supermarket and hypermarket business remaining in the original CBD. The spin-off was possible since the businesses had very separate management and supply chain structures, and their underlying drivers differ significantly. The original CBD remains have rallied significantly off the post-spin-off ADR price, and this, coupled with appreciation in the Assai ADR price, has seen the combined value increase by 31.5% to $18.83. The combined alpha from CBD/Assai during the quarter came to 0.8%. We have retained both constituent stocks in the Fund, although the CBD position was trimmed in response to the share price moves.

The last two significant contributors to alpha were Naver and China Literature. Naver returned close to 24% in the quarter, while China Literature returned 26%. They each contributed around 0.4% to alpha. In the case of Naver, our conviction levels have increased significantly due to market developments. Naver is the number two ecommerce player in Korea. The number one player, Coupang, came to market in an IPO that was heavily oversubscribed and beyond valuation metrics that made sense to own in the Fund after it jumped 40% on its first day of trading. The additional information gleaned during the IPO process on the market opportunity, coupled with better disclosure by Naver, resulted in us increasing both our estimate of fair value and the overall conviction in the investment case. As an example, Naver disclosed that its ecommerce gross merchandise value already amounted to $25 billion in 2020, and it has targeted a 30% market share by 2025, which would comfortably establish the business as a strong number two player, if achieved, in what will likely be a two-to-three player market. South Korea has the highest ecommerce penetration in the world (30%-32% estimate), a function of its high degree of urbanisation and technologically savvy population. As a result, its ecommerce market is already the fifth largest, despite the country being the 12th-largest economy overall.

On the negative side, the biggest detractor was Magnit, down 12% for a -0.4% contribution to alpha. This was in spite of decent 2020 results for both the company and X5, its main competitor and the largest player in Russian food retail (also held in the Fund). As expected, traffic declined significantly in stores during the year, but a 15% like-for-like increase in average basket size allowed like-for-like sales to increase by 8% in Magnit’s mature stores, far in excess of inflation. Great cash generation allowed Magnit to reduce its debt burden in absolute terms, and the improvement in profitability saw leverage decline to 1.1 times net debt to earnings before interest, taxes, depreciation and amortisation (EBITDA). Magnit trades on 13.5 times forward earnings and offers an 8.5% dividend yield, which in both absolute and relative terms is very attractive.

The other material detractor (-0.4%) was New Oriental Education, which declined 25% in the quarter. In an almost carbon copy reaction to previous regulatory intervention in 2018 (which allowed us to buy New Oriental after a 40% share price decline), various levels of the Chinese government (both national and regional level) enacted rules aimed at curbing abuse by smaller tuition providers. The trigger for the intervention was the news that many small providers, having taken tuition payments upfront, then went out of business, leaving parents with no recourse to the funds paid in advance. The regulatory authorities now require money to be suitably deposited at a bank, with parents ranking as secured creditors. Additional changes include restrictions on sales and marketing, as well as tighter approval processes for awarding business licences. These changes should all benefit the established credible players, such as New Oriental, as they raise barriers to entry and make it more difficult for smaller, sub-scale players to use temporary cash flows to stay afloat.

We added to New Oriental on the price decline and also bought TAL Education into the Fund. TAL is another leading tuition provider that we owned many years ago but sold out as it reached fair value. We have long wanted to own it again as the business has executed incredibly well in the intervening years, but it had always been too expensive. The share price declined from $90 to $50 between mid-February and late-March, which provided a good buying opportunity. TAL differs from New Oriental in that it is focused on small class offerings or one-on-one tuition, and predominantly covers maths and science. This compares to New Oriental, which offers larger classes and a wider variety of subjects, particularly English.

Additionally, TAL has expanded more aggressively into the online space than its peers and has achieved a double-digit market share. The promotional spend to get there has affected its profitability, a situation we expect to reverse over time. The different operating models of the two businesses allow them both to take market share without necessarily coming into direct competition with each other.

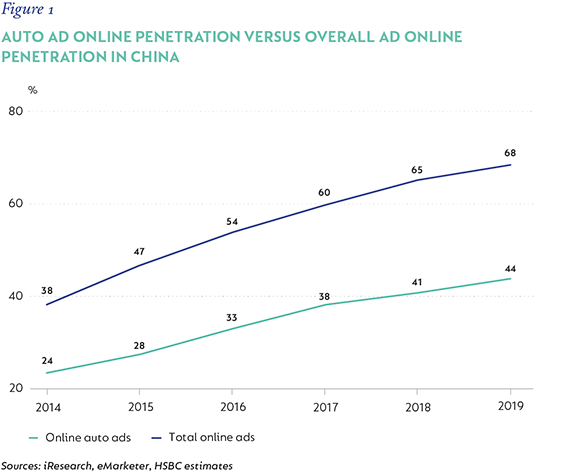

Other than TAL, there were four small new buys. The first of these, Autohome (0.9% position), is the leading online destination for automotive information in China. The site is a ‘one-stop shop’ that helps users to research, buy and sell cars. Users can also access finance and insurance through the site, thereby covering the full value chain. Purchasing an automobile is an infrequent event for most users, and it typically requires significant groundwork in order to navigate through the multitude of options available. A specialist auto site with independent reviews offers greater value to consumers than general sites and/or those with predominantly sponsored content. Like most internet portals, the feedback loop between a large number of users or traffic creates an ecosystem of greater value than what the competition offers and raises barriers to entry for competing sites. With 62 million monthly active users, Autohome is larger than the next three largest apps combined. The site makes money through advertising, generating leads for dealers, providing demand data (colours, models, etc.) to manufacturers and matching buyers and sellers of used cars. Additional commission is also earned by facilitating financing and insurance for vehicle purchases. The tailwinds for growth for Autohome are very strong. In addition to rising income levels, there are the twin benefits of low vehicle penetration and low online advertising penetration in automobiles relative to other sectors (see Figure 1). The used car market is also relatively new (the existing vehicle fleet in the country is not particularly old), and this will change over time. Autohome is capital light and generates returns on invested capital above 35%. Due to the very-high cash conversion (>100% of earnings converted to cash), Autohome has almost a third of its market cap in cash and trades at 16 times forward earnings, excluding this cash. The company also benefits from having Ping An as an anchor shareholder (45%), as Ping An brings strong strategic skills and significant network benefits from its large customer base.

The second new buy, AngloGold Ashanti (0.5% position), is the first gold miner we have owned in the Fund. This is the most attractive of the major emerging market gold miners in our view (if one excludes the marginal ones) and trades on eight times forward earnings and a spot FCF yield of almost 5%. Aside from the standalone attractiveness of the stock from a valuation perspective, we believe it brings something different to the portfolio due to the role of gold as a hedge against elevated valuations, something we had become concerned about early in the quarter, but which is less of an issue now in the subsequent market pullback. We also bought small positions in XP Inc. (0.4%), a highly innovative Brazilian wealth manager and investment bank, and Xiabuxiabu Catering (0.3%), which operates Hot Pot restaurants across China.

The second new buy, AngloGold Ashanti (0.5% position), is the first gold miner we have owned in the Fund. This is the most attractive of the major emerging market gold miners in our view (if one excludes the marginal ones) and trades on eight times forward earnings and a spot FCF yield of almost 5%. Aside from the standalone attractiveness of the stock from a valuation perspective, we believe it brings something different to the portfolio due to the role of gold as a hedge against elevated valuations, something we had become concerned about early in the quarter, but which is less of an issue now in the subsequent market pullback. We also bought small positions in XP Inc. (0.4%), a highly innovative Brazilian wealth manager and investment bank, and Xiabuxiabu Catering (0.3%), which operates Hot Pot restaurants across China.

Finally, due to continued share price strength and reaching of our estimate of fair value, we sold the small remaining positions in Hong Kong Exchanges and Midea Group (a Chinese appliance maker). Each was a 0.4% position at the beginning of the year.+

* American Depositary Receipt: When a company with a listing in one country has a secondary listing in America to make it easier for people to invest. Particularly if it’s difficult for foreigners to invest in the local listing.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter