South Africa - Personal

South Africa - Personal

THE CORONATION STRATEGIC Income Fund is our flagship managed income fund that has secured its place as a stalwart of the South African savings landscape with consistent performance and an enviable track record. The fund outperformed by 2.5% per annum since inception in 2001 (after fees), while delivering positive monthly returns 93% of the time.

By leveraging off the depth of our fixed income team and the breadth of Coronation’s entire investment team, portfolio managers Nishan Maharaj and Mauro Longano are able to invest across the full range of income-generating asset classes such as government, corporate and inflation-linked bonds, listed property, offshore bonds, money-market negotiable certificates of deposit and preference shares.

The main aim of the fund is to produce a consistent and reliable return for investors with immediate income needs and, as a result, the fund is well diversified, conservatively positioned and aims to limit investor downside. We believe in making small adjustments to the portfolio over time rather than taking big, portfolio-defining views so that we can deliver consistent returns to the fund’s conservative investor base. To reflect a low risk tolerance, we only invest a combined maximum of 25% of the fund in what we define as more volatile assets, such as listed property (maximum 10%), preference shares (maximum 10%), international assets (maximum 10%) and local hybrid instruments (maximum 5%). The fund will typically have no exposure to equities.

ENSURING THE FUND IS RIGHT FOR YOUR NEEDS

The fund is a good option for investors looking for an intelligent alternative to cash or bank deposits over a period of 12 to 36 months and who seek actively managed exposure to income-generating investments. The aim of the fund is to enhance yield as interest rates decline and to protect capital in a rising interest rate environment. It’s a great option if you need access to your investment over the short term, which means you don’t want to take on much short-term risk.

Investors may need to keep a portion of their capital in cash for different reasons. Business owners with lumpy cashflow may need to park some capital in a conservative asset with a higher expected return than cash to pay monthly bills such as salaries. Individuals may be saving for a near-term goal such as paying a deposit on a house, or retirees may wish to keep the next two or three years’ income in a fund that is not exposed to equity market risk.

Whatever the reason for needing access to your capital in the short term, a managed income fund may be a good option, as it aims to deliver a better return than a deposit at a bank, without materially increasing the risk of capital loss.

Managed income funds are typically not suitable for longer investment periods. Their limited exposure to growth assets constrains their ability to provide adequate protection against the eroding effects of inflation on one’s purchasing power.

The Coronation Strategic Income Fund is therefore unlikely to be suitable if you can invest for periods longer than 36 months, you need income to cover your everyday living expenses over an extended period of time, and you want to grow your capital to protect your purchasing power.

RETURNS AND RISK

We take an active approach to fixed interest portfolio management and all our investment decisions are driven by proprietary, in-house research that allows us to dynamically respond to changing market conditions. The fund’s benchmark is 110% of the STeFI 3-month Index, while our internal return target is cash plus 2% through the cycle. STeFI is an abbreviation for the Short Term Fixed Interest Index, and the three-month version is the most common benchmark used for more conservative money market funds.

To have a chance of achieving a better return than that of a money market fund or a short-term deposit at a bank, investors need exposure to assets with a higher expected return than cash. Unfortunately, a higher expected return comes with an associated increase in risk, requiring a careful trade-off between adding to the return potential of the fund while keeping risk exposures at an appropriate level. The Coronation Strategic Income Fund is managed to achieve this balancing act by taking considered interest rate and credit risk, where appropriate, and through moderate increases in exposure to alternative sources of return when the likelihood of outperformance is high.

Our approach to managing the fund remains focused on outperforming cash over the long term, but over short measurement periods, capital at risk can fluctuate and, as a result, the fund will not have a linear return series, as is the case with a money market fund. While cash plus 2% is not always achievable in the short term, the fund has consistently outperformed cash and the benchmark over the longer term.

UNDERSTANDING QUOTED INTEREST RATES

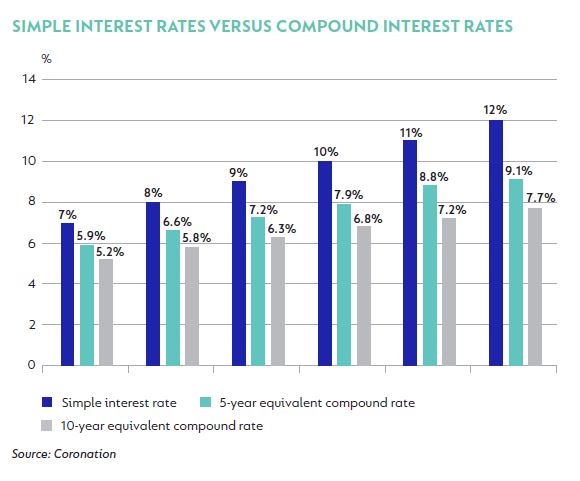

When making any fixed deposit investment, it’s important to understand that the quoted interest rate and the potential return may not be the same. Adverts for fixed deposit products can be misleading and often quote simple interest rates rather than compound interest rates. Simple interest is calculated only on the original investment amount, while compound interest is calculated on the original amount as well as the accumulated interest of previous periods. The power of compounding is critical to long-term wealth creation.

To highlight the effect that compounding has over long periods of time, consider the following scenario: R1 million invested at a 7% simple interest rate means that you get a yield of R70 000 every year, regardless of the capital value and period. With compound interest, this R70 000 is reinvested annually and you then earn 7% on the original amount as well as on the reinvested amount, which grows your investment at a faster rate over time. The graph below compares a simple quoted interest rate with the equivalent compound rate over five and 10 years. It is useful to keep in mind how the power of compounding has a meaningful impact on the effective rate over time. For instance, if you are quoted a simple interest rate of 10% per annum over 10 years, it means that you only require a compound interest rate of 6.8% per annum over the same period to get the same return.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter