South Africa - Personal

South Africa - Personal

Deciphering the world of investment is not about having the fanciest quantitative model or being a mathematical genius; rather, it is about being able to separate emotion from decision-making. To quote Warren Buffet: “The most important quality of an investor is temperament, not intellect”. Over the last quarter, there has been quite an increase in volatility, due to both global and local factors. Globally, there has been a complete about-turn by central banks on monetary policy normalisation, leading to an inversion of the US yield curve which has stoked concerns of an imminent US recession, not to mention the continuing uncertainty about the outcome of US/China trade negotiations and total paralysis surrounding the Brexit process.

Emotions have also been running high in South Africa over the last quarter. The Zondo Commission continues to reveal shocking levels of corruption prevalent in government and associated institutions. Years of mismanagement and looting are now resulting in the intensification of load shedding, contributing to an already somber mood locally. Consumers and corporates have continued to tighten their belts, deepening concerns of continued low growth in South Africa. In these times, it is important to separate fact from emotion, and let valuation guide investment decisions.

The All Bond Index (ALBI) returned 3.8% over the last quarter, bringing its return over the last 12 months to 3.5%. Inflation-linked bonds continued to lag nominal bond performance, producing 0.6% over the last quarter and -3.1% over the last 12 months. In dollars over the quarter, South African bonds returned 2.8%, in line with the 2.9% returned by other emerging markets (as measured by the JP Morgan Government Bond Index – Emerging Markets Global Diversified Composite). However, they remain quite a laggard over 12 months (-15.6% versus -7.5%). The 10-year benchmark bond traded in quite a narrow range over the quarter (9.47% to 9.08%) before breaking lower to sub-9.0% after the end of the quarter, following rating agency Moody’s decision to keep South Africa’s credit rating stable at investment grade.

BURDEN OF THE STATE

The sustainability of South Africa’s investment grade rating will remain a key concern. Credible monetary policy has caused inflation and inflation expectations to gravitate towards the midpoint of the band (4.5%), yet it remains adequately accommodative given the subdued growth profile. Growth, or the lack thereof, remains at the core of South Africa’s structural problems. Cyclically, growth should pick up to approximately 1.3% in 2019 and 1.8% in 2020. However, the risk to this outcome is to the downside, given the threat of load shedding, the effect it has on business and consumer confidence, and how rising electricity-related costs affect corporate profitability. The burden of low growth and state-owned enterprise (SOE) support weighs heavily on fiscal policy. Until more concrete structural reforms are put through, it is up to fiscal policy to provide a supportive growth environment and support for SOEs in a manner that does not widen the fiscal deficit or increase South Africa’s debt burden. Up to now, this has been well managed, as is evident in the February budget, where despite the R23 billion per year capital injection for Eskom, National Treasury still managed to limit fiscal slippage by cutting expenditure, primarily through a reduction in the wage bill. Unfortunately, given Eskom’s precarious financial and operational position, the SOE still poses immense risk to both the fiscus and the economy.

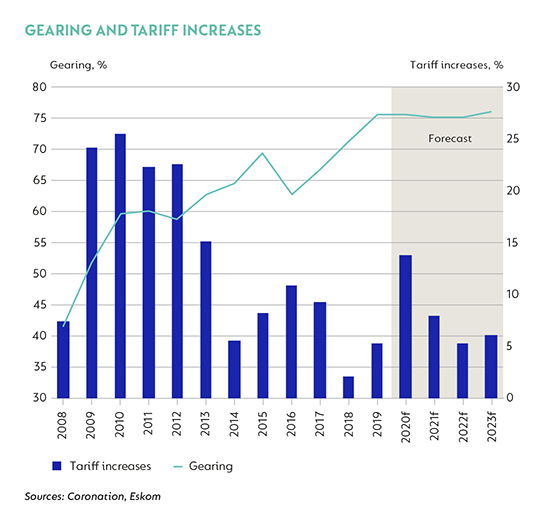

ESKOM - THE GREAT UNKNOWN

Eskom’s key areas of concern are the appropriateness of the magnitude of capital support that Treasury has set aside, the merit of the turnaround plan that has been proposed, its operational ability to keep the lights on and its financial sustainability. Given the current available information, the R23 billion annual capital injection and the framework outlined in the turnaround plan, one should expect the entity to stabilise. Implementation risk remains elevated, which is not helped by the omission of a timeframe and the apportionment of responsibilities within the turnaround plan. Operational efficiencies and cost saving will have to be realised quite quickly if the entity is to return to any form of stability. In the graphs below, we show Eskom’s gearing levels, taking into consideration the new tariff increases, the annual capital injection and increased diesel costs due to the use of open cycle gas turbines (OCGTs) to help increase electricity production because of failures at coal plants. Key areas of risk include the halving of maintenance during the next six months to bring up energy availability, which will remain below the norm (refer to Mauro Longano’s article) and financial gearing that does not decrease despite the immense amount of support rendered, placing pressure on the need to cut costs. More concerning unknowns that will continue to weigh on outcomes is the current state of Eskom’s plant fleet – how bad deterioration has been, the significance of design deficiencies at the new power plants Medupi and Kusile, and the cost to bring this back to norms. Given its poor baseline (both operationally and financially) and the large number of obstacles Eskom needs to overcome, chronic load shedding is something that the South African economy will have to deal with for at least the next two to three years, posing downside risks to both the fiscus and expected growth outcomes.

When the lights go out, there will always be a tendency for emotions to take over and all hope to be lost. When it comes to investment, it is vital to step back to observe the bigger picture, separate emotion from the research process and let valuation guide investment decisions.

GOLDILOCKS OR THE BEARS?

Global monetary policy has again turned accommodative. Following the US’s about-turn on monetary policy, the European Central Bank followed suit a few weeks later. Global bond yields have plummeted, with the US 10-year Treasury Note continuing to rally to below 2.4%. An amazing 20% ($10.3 trillion) of all issued government bonds now trade with yields below zero. In previous periods, this proved to be quite supportive for emerging market government bonds; however, this time around, given the inversion of the US yield curve (10-year rates trading below cash rates), more caution has been exercised. An inverted US yield curve has been a successful predictor of all recessions over the last 30 years; however, the period between curve inversion and the onset of recession varies between 12 and 24 months. Therefore, over the short term, we might see this ‘goldilocks’ period for emerging markets continue, supporting their currencies and bond yields.

Over the longer term, we still see fair value for US bond yields being above 3%. Growth in the US has come off in the shorter term due to the government shutdown at the beginning of the year and the tax cuts of 2018 coming out of the base, but is still expected at 2.5% for 2019 and 2.0% in 2020. Furthermore, wage inflation has continued to prove quite sticky, which should keep headline inflation close to the 2.0% level. Market expectations of interest rate cuts in the US seem premature at this stage, with the economy growing at 2.5% and inflation at 2%. A 1.0% real policy rate still seems appropriate given the prevailing conditions, which suggests a 3.0% nominal long bond rate at the minimum (2.0% inflation plus 1.0% real policy rate). The risks posed to global bond yields are therefore to the upside.

Does the rating matter?

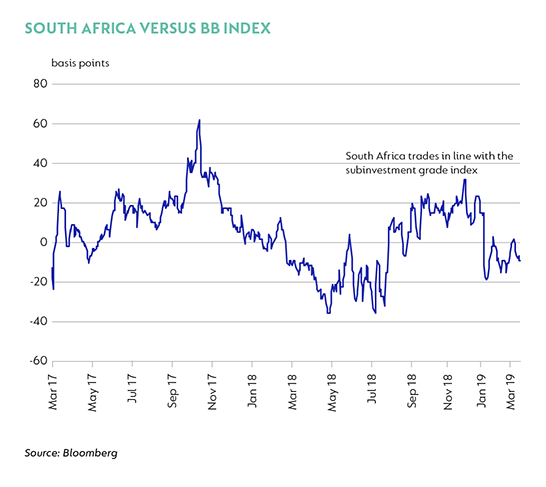

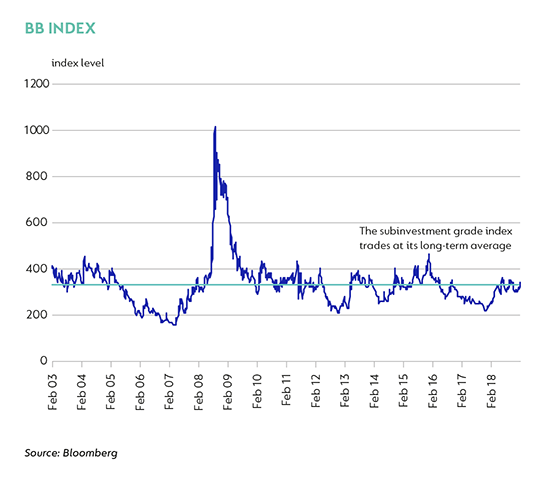

The key consideration for a South African bond investor is whether the yield on offer by South African government bonds compensates them for the underlying risks that the economy faces. The main areas of concern are the effect of South Africa losing its investment grade rating, the impact of higher global yields on South African bond yields and how South African bonds fare relative to their emerging market peers. South Africa’s credit rating has and continues to trade at subinvestment level. The graphs below show the South African credit spread relative to the BB Spread Index (the index representing the credit spread of the first rung of subinvestment grade) and then the BB Spread Index (right) over a long period of time. The graph on the left shows that South Africa trades in line with the subinvestment grade index (10 basis points [bps] more expensive than current index levels), while the graph on the right shows that the subinvestment grade index trades pretty much at its long-term average. Both metrics suggest that South Africa, even if Moody’s were to move the country to subinvestment grade, at worst could see a widening of between 10 bps and 20 bps.

PEER REVIEW

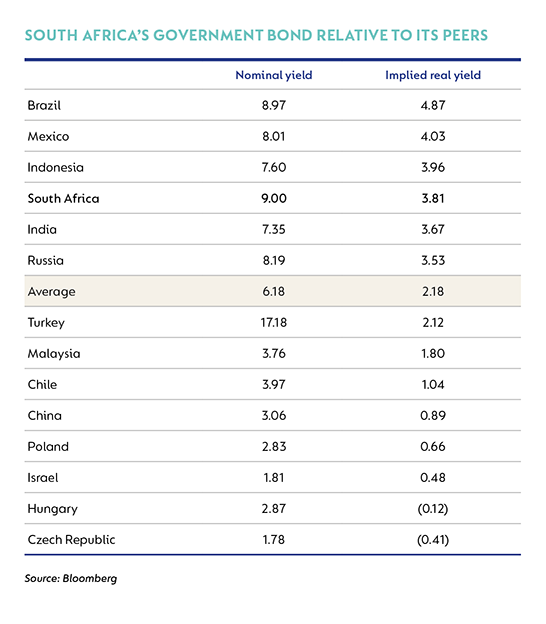

In the table below, we show South Africa’s government bond relative to its emerging market peers, both from a nominal bond perspective and an implied real perspective (using two-year expected average inflation). Once again, South Africa features as quite attractive relative to its peers, especially considering that Brazil has yet to pass a massively unpopular pension reform initiative to reduce its debt to GDP ratio from 80%, while Mexico’s largest SOE (petroleum company Pemex) is in dire need of further financial support that will weigh on the Mexican fiscus and, hence, creditworthiness

LIMITED APPEAL

If we construct a fair value for South African 10-year bonds using the global risk-free rate (US 10-year yields), the expected inflation differential (between South Africa and the US) and South Africa’s credit premium, the result is 8.92% (3.0% + (5%-2%) + 2.92%). Current levels of 9.0% on South Africa’s 10-year government bond therefore compare quite favourably to our fair value estimate. Given the long-term risks the local economy faces, predominantly from a further deterioration in Eskom, one would look to move to a more neutral to slightly underweight allocation to South African government bonds, as levels move through our fair value estimate.

Chronic load shedding and poor local sentiment will continue to weigh on South Africa’s growth outcomes. Inflation should remain under control, allowing policy rates in South Africa to, at worse, remain stable. Global monetary policy has once again turned more supportive for risk sentiment, which should help buoy emerging market valuations over the shorter term. At current levels, South African government bonds trade cheap to fair value estimates. However, given the longer-term risks posed to the economy from further SOE deterioration, allocations should be kept at a neutral level.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter