South Africa - Personal

South Africa - Personal

Investment views

Addendum 3: Stress testing worst-case scenarios

- assessing asset class performance in weak state regimes

ZAMBIA

After a solid period of growth in the 2010s, Zambia experienced a deceleration generated by deteriorating confidence, a worsening business environment, growing authoritarian/nationalistic tendencies by the government and, very significantly, consistent fiscal deterioration. Heavy external borrowing, coupled with an extremely poor efficiency rate and a lack of real political commitment to fiscal sustainability, finally resulted in a sovereign default in 2020. This has yet to be fully worked through, although a change of government, sustained austerity, and a much more constructive approach to reform and credibility are laying the foundation for a medium-term recovery of the economy.

From a relative asset class performance perspective, there are a few elements to highlight:

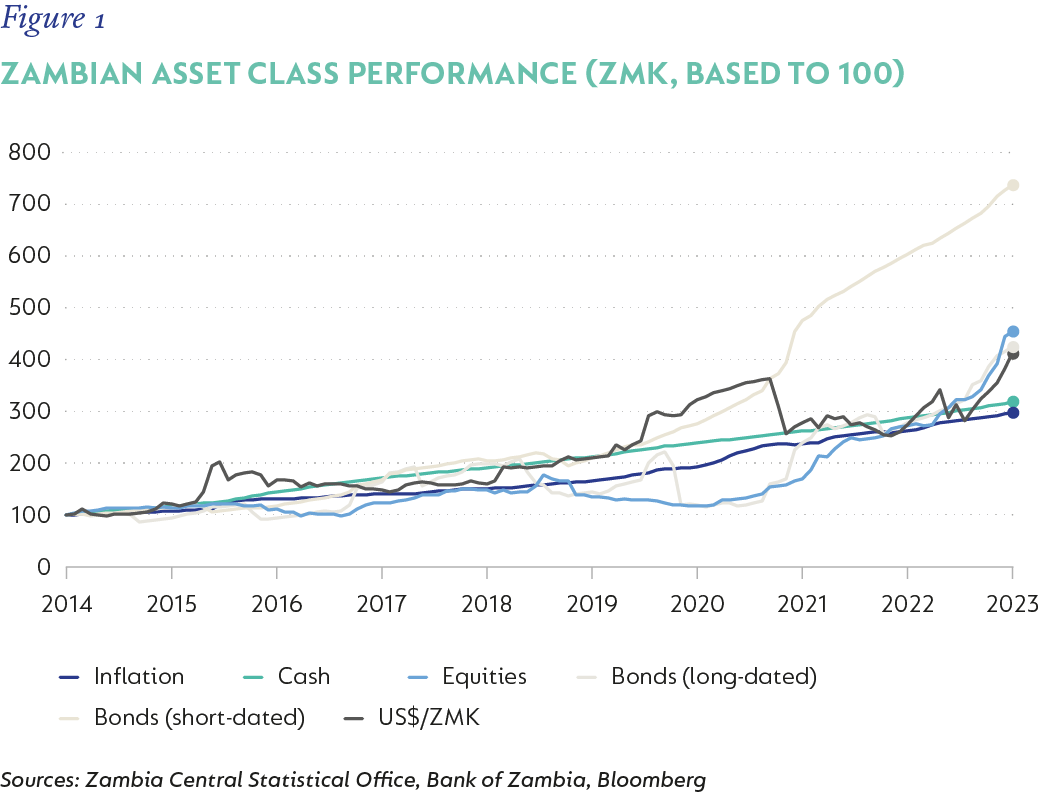

- Figure 1 shows how relative asset class performances in Zambian kwacha (ZMK) have largely been a wash on a cumulative basis since 2014.

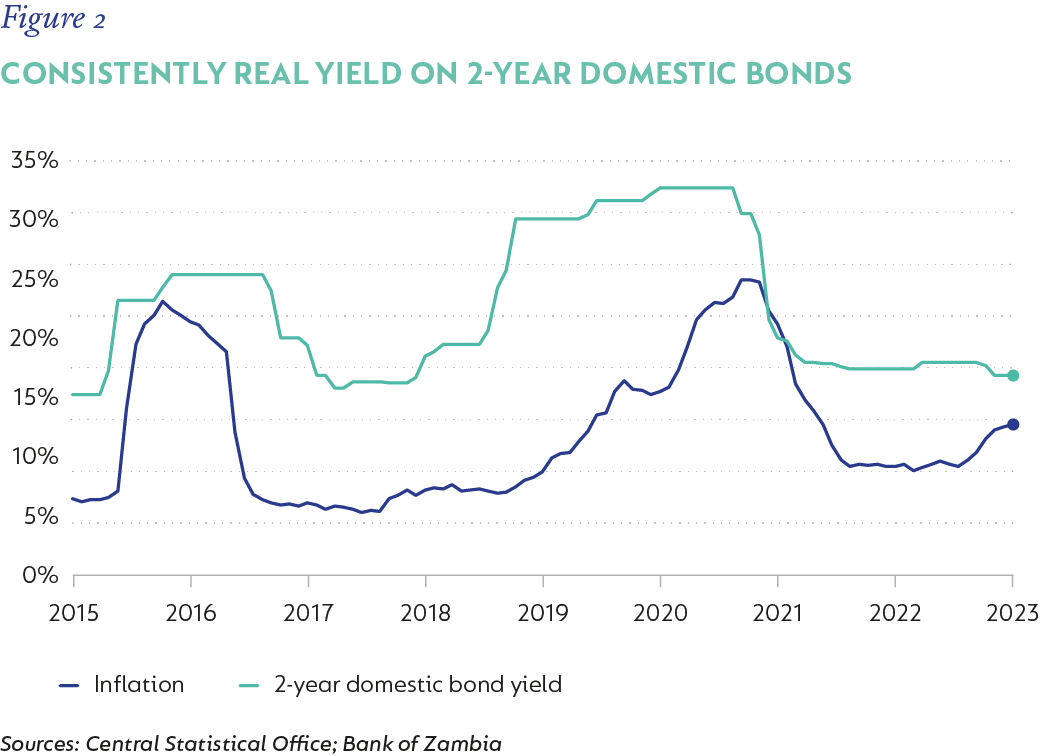

- Figure 2 highlights that the notable exception has been the empirical performance of a persistent allocation to short-dated local Zambian bonds. There are a few contributing factors here. The most important was the explicit and forthright rejection of the debt restructuring of domestic currency sovereign bonds, despite domestic Treasury bonds comprising c. 30% of the total public debt stock. This allowed for a substantial re-rating of local bonds, producing a much steeper yield curve than before. But it’s really been high real rates for sovereign borrowing in kwacha that have served short-dated exposures particularly well. Indeed, between 2015 and December 2023, real yields here averaged over 10% – with minimal duration risk, and mostly quite slim term premia in Zambia in the past. This has proven an especially potent combination to ensure a persistent, steady compounder in domestic terms.

- Yet, the continued longevity of such a favourable absolute and relative outperformer is undoubtedly questionable. The high level of real rates in Zambia is appealing to a wide investor base – yet isn’t economically sustainable for an extended period. The curve has a much more normal shape now; hence long-dated Zambian sovereign exposure should provide a return pick-up over short-dated maturities over time. And, the avoidance of a domestic debt restructuring was essentially a windfall for Zambian bonds – much of the additional real bond performance over the entire holding period is a result of this favourable outcome.

Disclaimer

SA retail readers

SA institutional readers

Global (ex-US) readers

US readers

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter