South Africa - Personal

South Africa - Personal

Personal finance

Overview

Investors near or in retirement face a significant inflection point in their investment journeys. Those looking to pay themselves a retirement income from a living annuity can expect to navigate a new set of risks that they may not have encountered before, and for which the mandates of their pre-retirement investment funds didn’t need to cater for.

The risks that you are likely to face when you start drawing an income in retirement are trickier to navigate, but not impossible.

This edition unpacks these risks in more detail and explains how investing in an appropriate fund that is specifically managed for this phase of your retirement, coupled with choosing a prudent starting income drawdown rate, can help make these risks more manageable. It also showcases two bespoke Coronation funds that have supported the specific needs of living annuity investors over multiple decades.

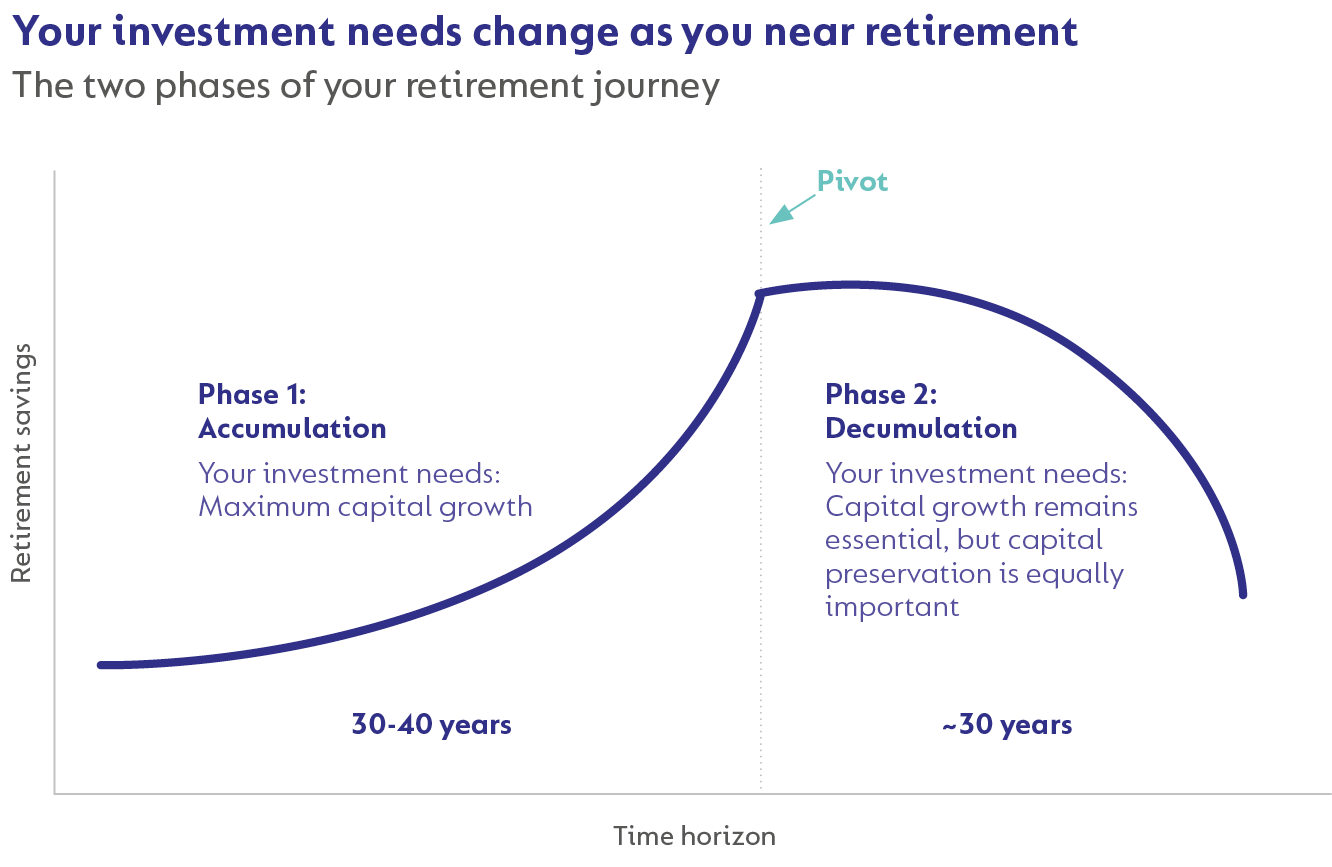

What happens to your investment needs at retirement?

Saving towards your retirement could take up most of your working life (30-40 years). If you manage to stay the course, invest sufficiently (enough) and appropriately (with adequate exposure to risk assets), history tells us there are few risks that could derail this long-term goal. The only investment outcome you need to concern yourself with is maximising capital growth in a tax-efficient manner as you build your nest egg during this accumulation phase of your retirement journey. (Read more in our Investing tax-efficiently for long-term goals edition of Corolab.)

However, as you near your retirement date, your investment objectives will start to change as you enter the decumulation phase of this journey. Your investment objectives now need to deliver on two needs simultaneously:

- Generating capital growth (that is ahead of inflation) over what could be yet another multi-decade period; and

- Equally important is capital preservation in the short term as you need to draw a sustainable regular income from your accumulated savings.

What are the risks that you need to navigate in the decumulation phase of retirement?

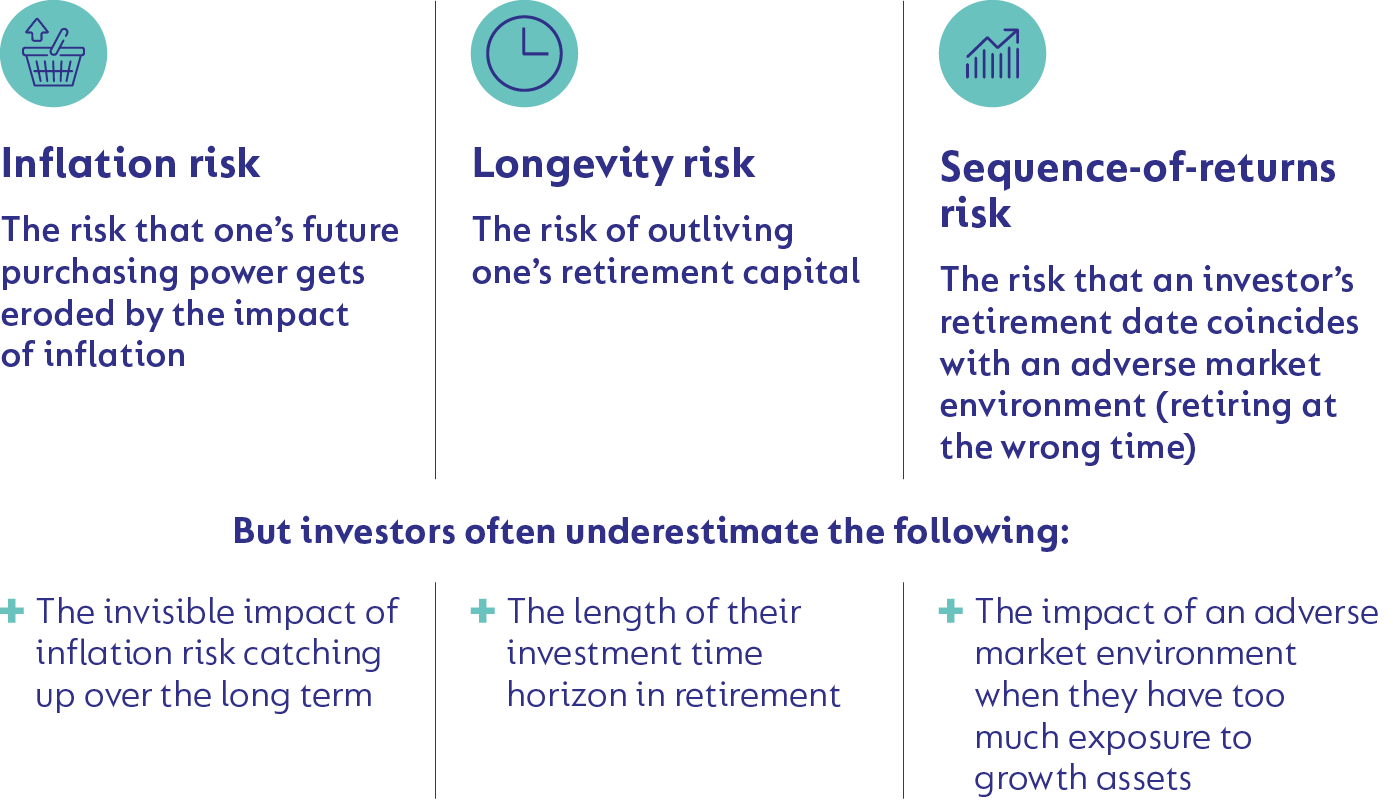

Living annuities are often the most appropriate product from which to draw a regular income in retirement, providing the benefits of flexibility and the fact that unused capital is heritable. However, because they pay a regular income, investors in these products face a number of new risks that they may not have encountered (or considered) as part of the accumulation phase of their retirement journeys. These risks (detailed below) need to be managed on an ongoing basis and in an appropriate manner.

INFLATION RISK

As the prices of the products and services we use rise, an investor’s future purchasing power may be less than what they require to maintain their standard of living throughout retirement. While the eroding effect of inflation on one’s savings may not be that noticeable in the short term, the impact over time can be devastating, as is clear from the following example:

At an inflation rate of 6% per year (a prudent financial planning assumption for inflation, informed by the very long-term average), the purchasing power of R1’s worth of savings today will reduce in value to only 17 cents over a period of 30 years (a prudent planning horizon).

WHO IS MOST VULNERABLE TO THIS RISK?

Retirees with a lengthy retirement horizon are particularly vulnerable to this risk. Especially if their investment return is:

- Less than the inflation rate (in which case their purchasing power reduces); or

- Equal to the inflation rate (in which case their purchasing power is merely protected).

This makes it very difficult to sustainably fund regular withdrawals that also need to grow with inflation.

What about a material inflation shock?

While hyperinflation in response to a crippling currency devaluation remains a tail risk, studying examples of historical hyperinflation events (such as that of Germany’s Weimar Republic post WW1) can provide some useful guidance on the range of outcomes that prevailed and the asset classes that are likely to provide protection against a material inflation shock. The key lesson for South Africans is that the traditional perception of riskiness between different asset classes is turned on its head. Foreign and locally listed equities provide much better protection against hyperinflation than cash or bonds.

LONGEVITY RISK

The prudent investor will dedicate multiple decades to accumulating their retirement savings. Yet, many investors underestimate the fact that the time they spend in retirement (and, as such, the period over which their retirement savings need to last) will likely also span multiple decades.

Investors can address this risk by:

- Planning for a longer retirement time horizon

Most people in their early 60s can expect to live another 20 to 30 years. It is thus considered prudent to plan for a longer lifespan of at least 30 years. If a 30-year planning horizon sounds unpalatable, investors may want to consider allocating a portion of their retirement capital to a guaranteed annuity where the excess contributions made by retirees living less than the roughly 20-year average end up funding the additional income required by those who live longer. In essence, you transfer longevity risk to the life office by paying them a fee. Deciding when to do that, and with how much of your retirement capital, requires a detailed discussion with a qualified financial planner.

- Invest in an appropriate fund

Lower down, we demonstrate how investing in appropriate levels of growth assets has supported long-term growth over a multi-decade time horizon. Needless to say, we continue to see investors invest too conservatively in retirement.

- Select a prudent income drawdown rate

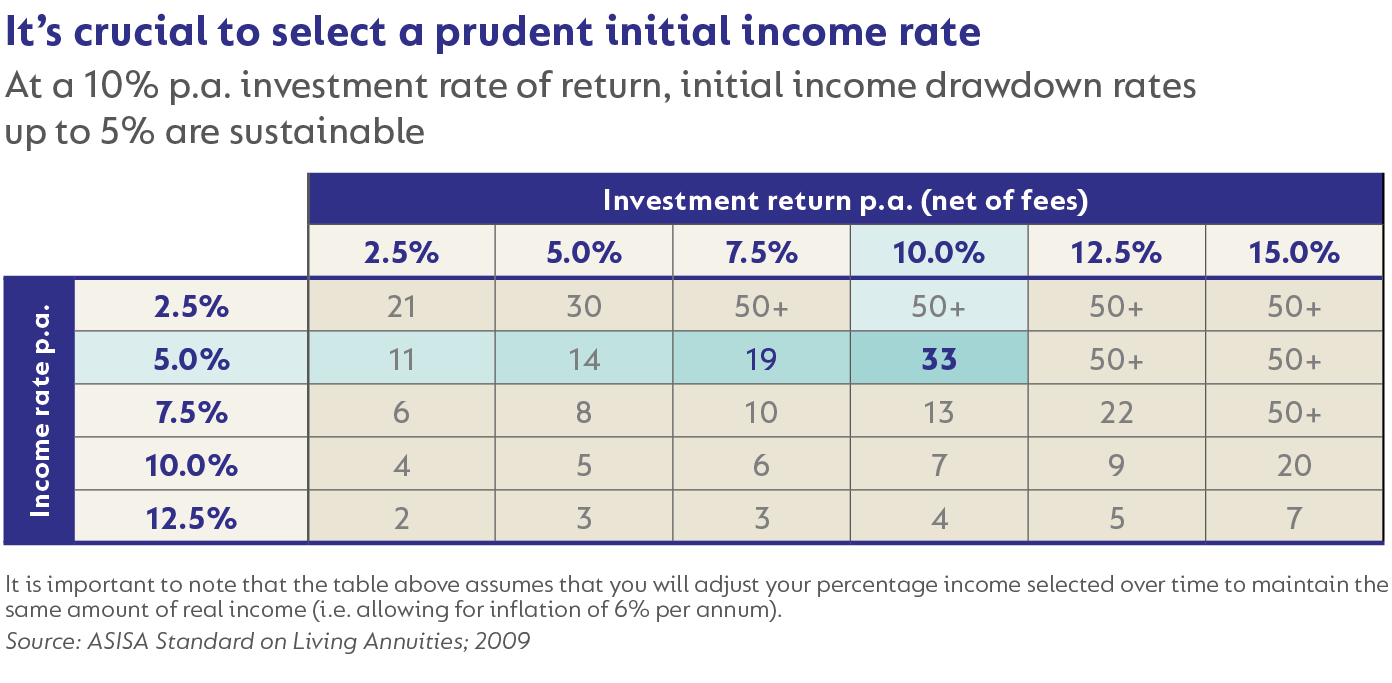

Selecting an income drawdown rate (at the start of your retirement) that is too high is as dangerous as being too optimistic about your expected investment rate of return. The following table explains why this is the case. It maps a retiree’s initial income rate (between 2.5% and 12.5% per year) against a number of potential net investment returns (from 2.5% to 15.0% per year). The value in each cell represents the number of years over which you will be able to maintain your standard of living, assuming an inflation rate of 6%.

For example, at a net investment rate of return of 10% p.a. (Coronation Capital Plus has achieved 11.1% p.a. since inception as at end-April 2023), any initial income drawdown rate up to 5% represents a sustainable level, as it will take roughly 33 years (a prudent investment horizon in terms of retirement planning) before you reach the maximum drawdown limit (of 17.5% p.a.) in your living annuity.

However, note what happens when the expected investment return drops to 7.5%: the period over which you can sustain an income drawdown of 5% p.a. drops dramatically from 33 years to 19 years.

This table illustrates how sensitive the sustainability of your chosen income drawdown rate is to investment returns and supports our view that for most investors an initial retirement income drawdown rate of 5% p.a. is prudent. (Read more about spending rules)

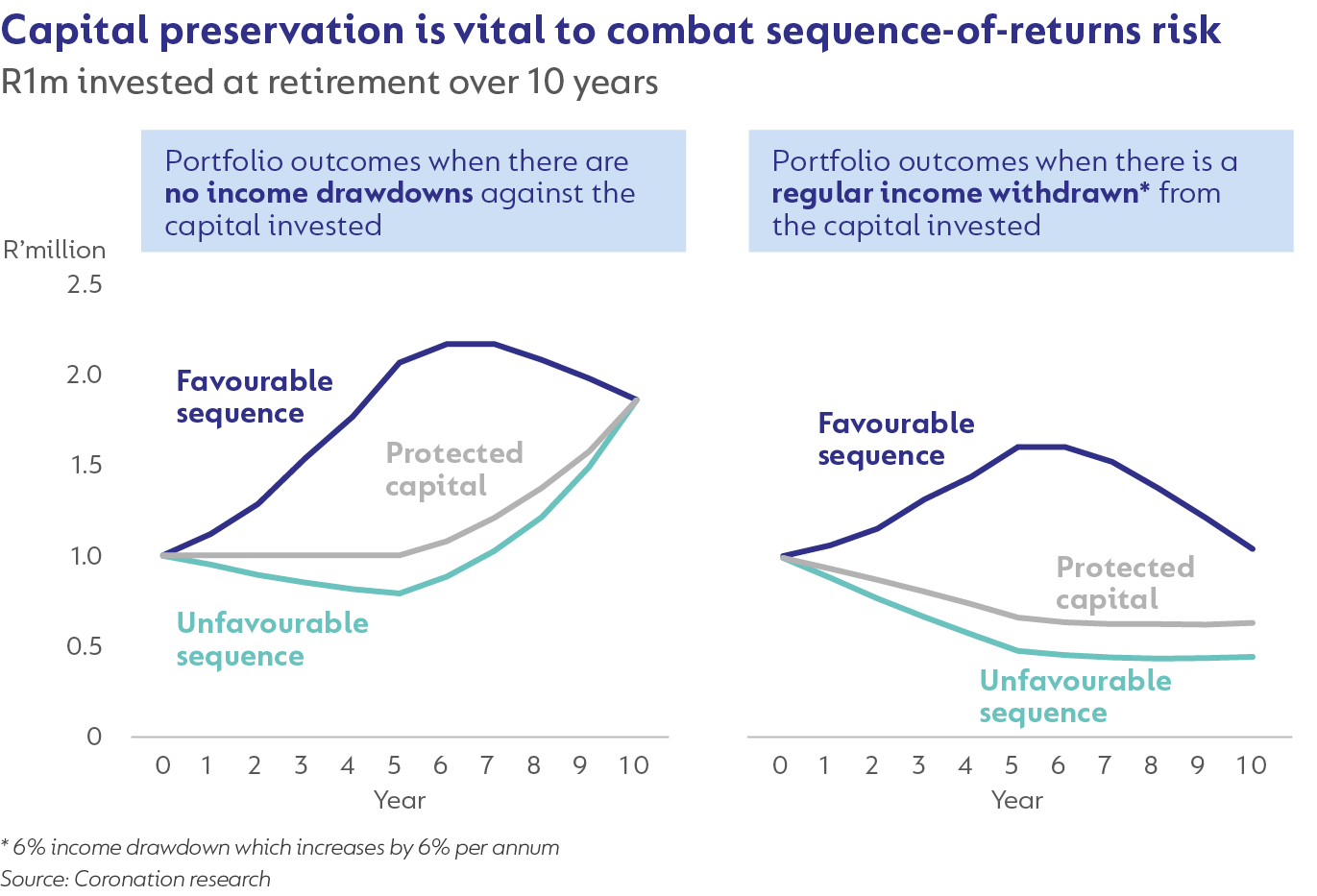

SEQUENCE-OF-RETURNS RISK

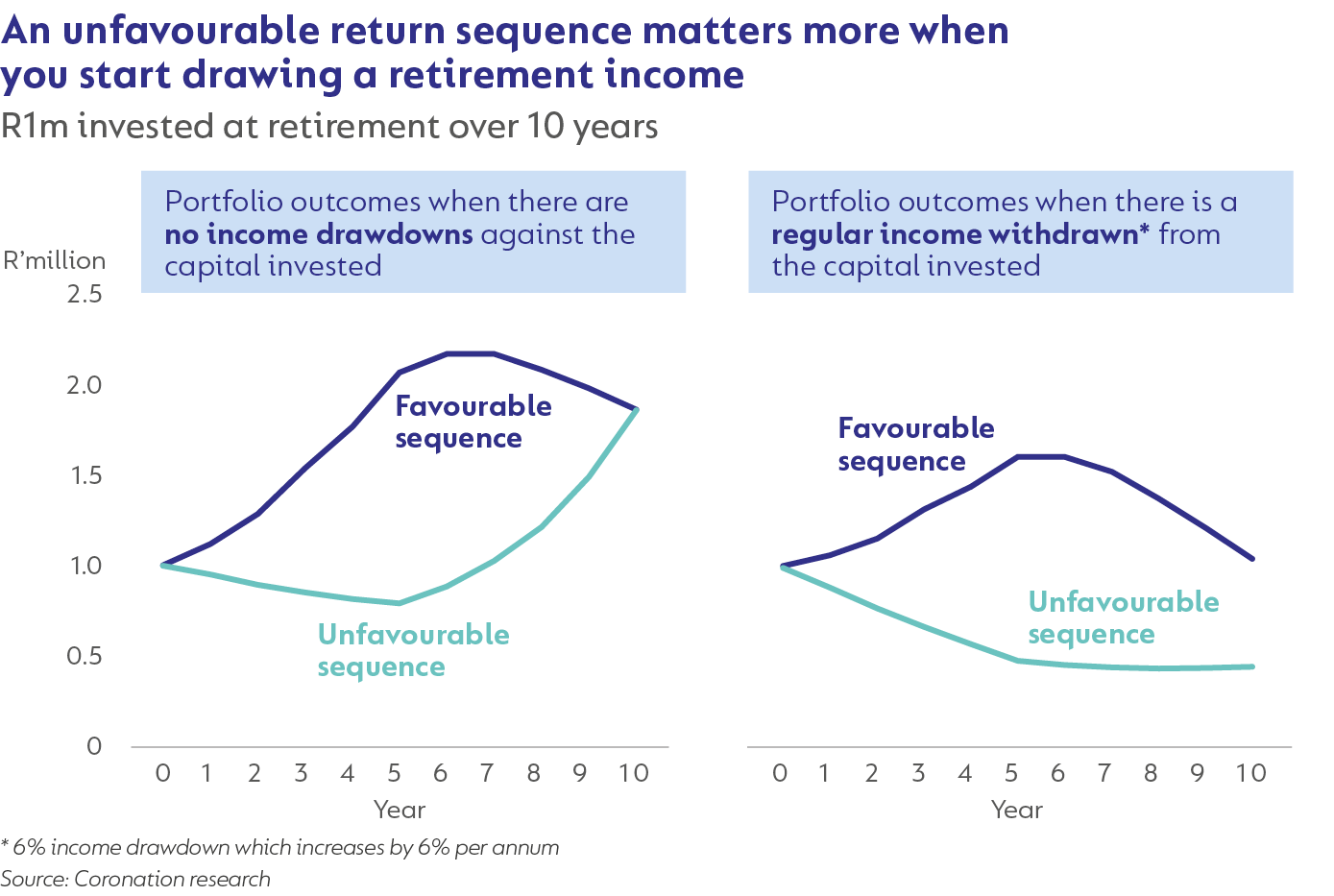

Even if investors do all the right things up to the point of their retirement, their retirement date may still coincide with an adverse market environment. This is likely to happen when a higher proportion of negative returns are earned in the early years of retirement. This will have a lasting negative effect and reduce the amount of income an investor can withdraw over their lifetime.

Consider the following exercise: The two graphs below depict two portfolios that achieve the same annualised return over 10 years but in different annual sequences. In the graph on the left, the blue line represents the portfolio that experiences more favourable returns early on, whereas the mint line represents a portfolio that suffers its worst returns first, followed by better returns towards the end of the 10-year period. Ultimately, the two portfolios end up with the same amount of capital, so the sequence in which returns are delivered is irrelevant.

The graph on the right, shows the outcomes when we add a withdrawal of 6% p.a. that escalates by 6% each year to allow for the impact of inflation on your living standard. It is immediately apparent how devastating the impact on accumulated savings can be if a retirement date coincides with an adverse market environment. The portfolio that suffers an unfavourable sequence of returns (mint line) ends the period with a capital value roughly half that of the portfolio with the better return sequence (blue line).

Although this risk of suffering an unfavourable sequence of returns at the start of your retirement cannot be eliminated, ensuring that the capital is protected during adverse market return periods can materially reduce it.

Consider the same scenario as before, but now with the inclusion of a third portfolio as represented by the grey line. In the graph on the left, this portfolio experiences the same market environment as the blue and mint lines but manages to protect capital during the early years when returns were negative, allowing the investor to end up with the same return at the end of the period.

When we add the income drawdown to this portfolio (see graph on the right), it becomes clear how vital capital preservation is during retirement in combatting sequence-of-returns risk.

The portfolio that protected capital during the first few years ends up with a final capital value around 40% higher than that of the mint portfolio, which experienced a poor initial sequence of returns.

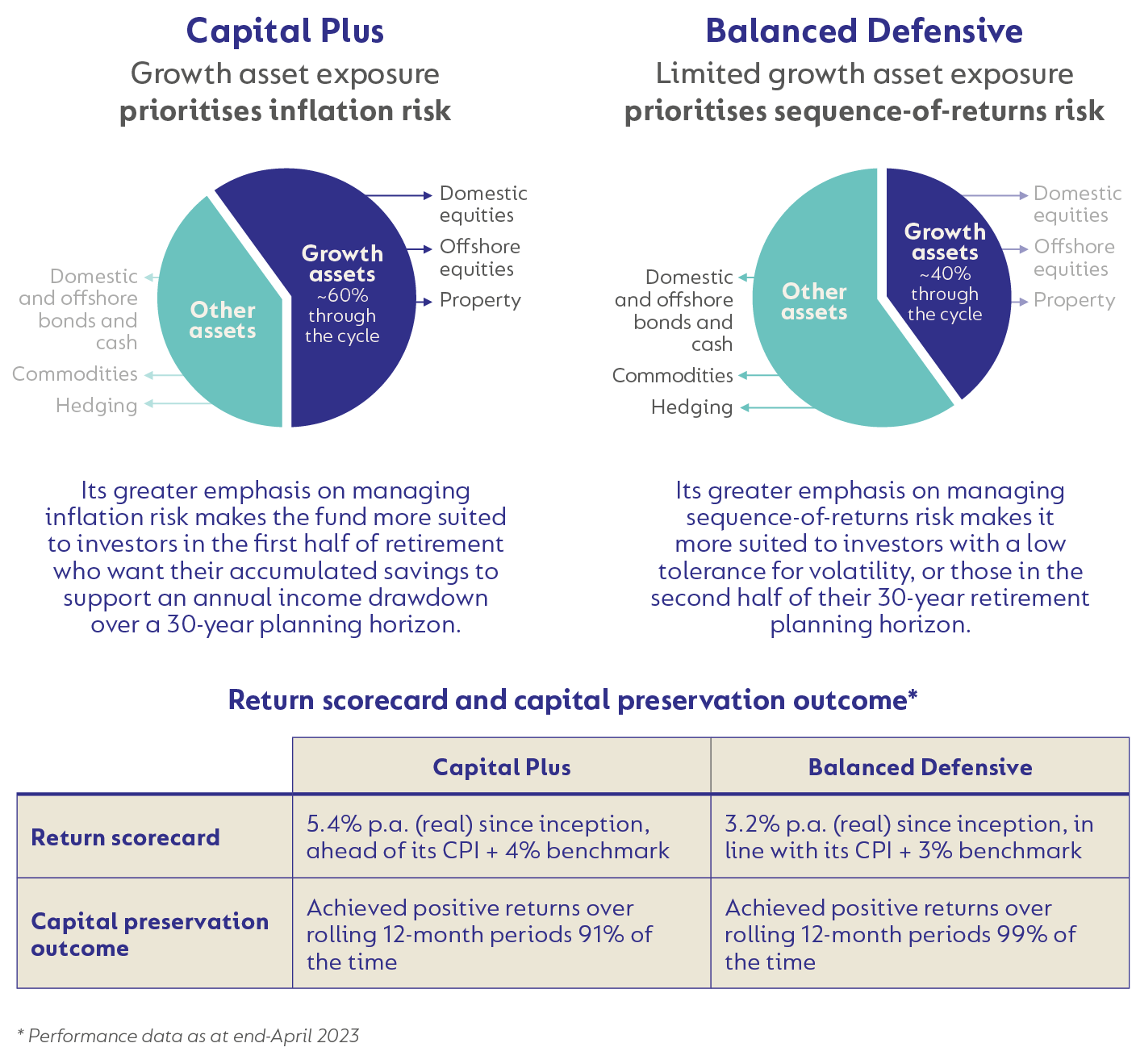

The importance of choosing the right fund for the second phase of your retirement journey

It is critical that investors identify an appropriate multi-asset class fund for this phase of their retirement journeys that allows them to stay the course.

Coronation offers two funds that are specifically designed and managed for retired investors in the decumulation phase of their retirement investing journeys – Coronation Capital Plus and Coronation Balanced Defensive.

The two funds are risk conscious, meaning that they are designed to manage all three risks faced by living annuity investors (as discussed earlier on). However, there is a difference in emphasis in these funds to cater for retired investors whose objectives may differ. The following visual will help investors align their individual risk prioritisation with the most appropriate fund.

Putting the management of these risks to the test

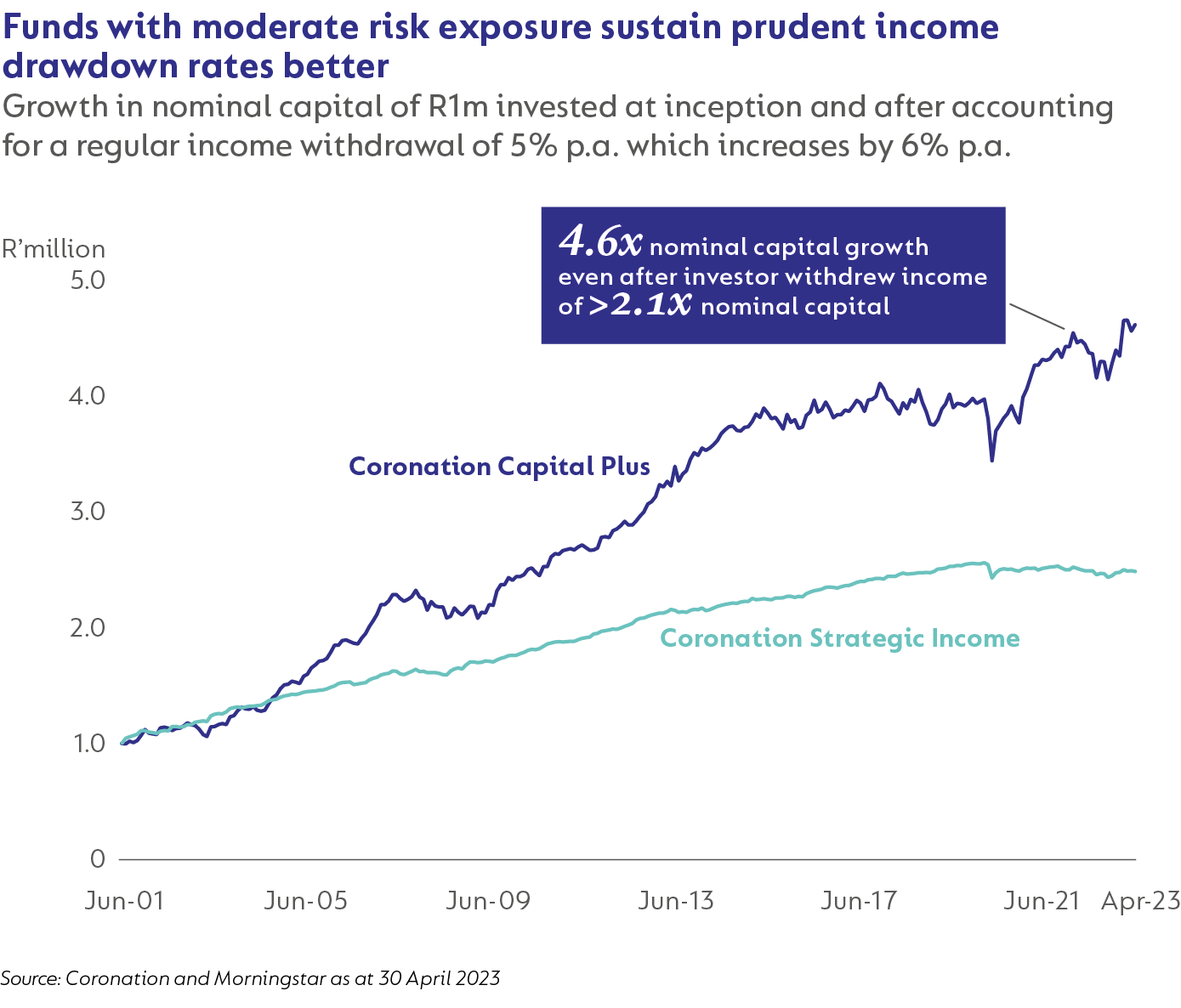

Below we demonstrate how well the appropriate multi-asset fund (with adequate exposure to growth assets but managed to achieve a smoother return path) can support a sustainable prudent drawdown income rate over a multi-decade horizon.

Case study: Sustaining a prudent income drawdown over the long term

The following chart tracks living annuity investments in two Coronation funds with different risk profiles. Our flagship living annuity portfolio, Coronation Capital Plus, has a moderate risk profile, with an expected average growth asset exposure of 60% through the cycle, while the managed income fund, Coronation Strategic Income, is a conservative portfolio, with an expected average exposure to growth assets of 5%.

The lines show the growth in nominal investment outcomes (unadjusted for inflation) over a 22-year period for a starting drawdown rate of 5% a year from both funds, which increases by 6% annually. During this time, the Coronation Capital Plus Fund has delivered a return of 11.1% per annum, while Coronation Strategic Income has returned 9.5% per annum (as at end-April 2023).

Key take-outs from this exercise

It is clear that Coronation Capital Plus, the fund with appropriate levels of growth asset exposure, is much better at supporting long-term investment growth than Coronation Strategic Income, delivering 4.6 times the initial capital amount invested, compared to Coronation Strategic Income’s 2.4 times initial capital. And that is even after the retiree has withdrawn more than double the initial capital amount invested (>R2.1m) by way of income.

Managing your income level on an ongoing basis

Further to selecting a prudent income level (as discussed on page X), it may be worth considering the introduction of dynamic spending rules.

By managing your income drawdown rates more actively in response to your investment portfolio’s performance, retirees can avoid reaching unsustainable drawdown levels that make running out of money inevitable. In other words, first earn the returns before withdrawing them.

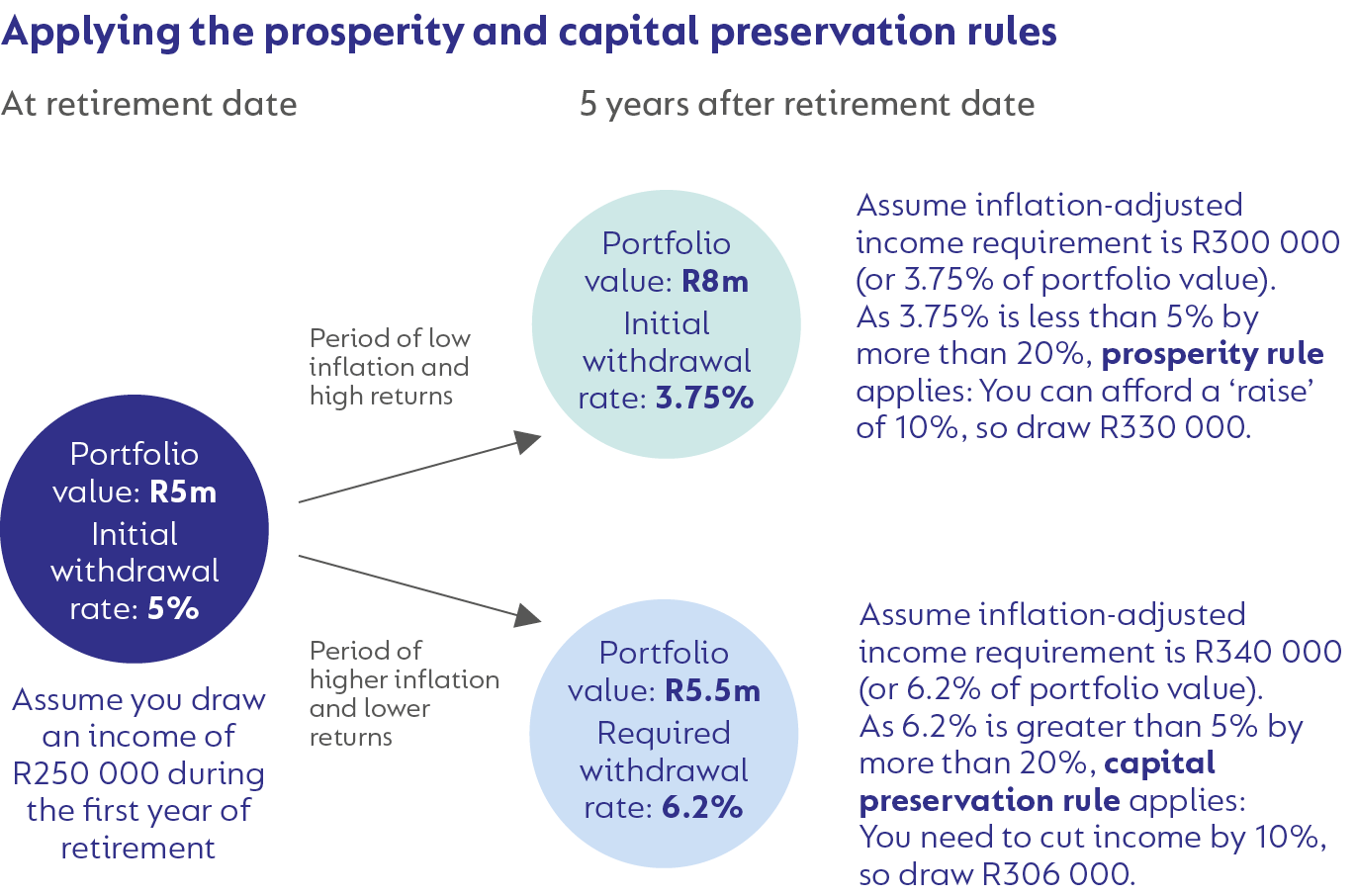

The modified withdrawal rule

Increase your withdrawal amount by inflation each year; except when the portfolio had a negative return in the previous year, and the new withdrawal rate exceeds the initial withdrawal rate.

The capital preservation rule

If the increased withdrawal rate in a given year exceeds the initial withdrawal rate by more than a certain percentage (e.g. 20%), the withdrawal rate is cut by a predefined percentage (e.g. 10%). This rule is only applied in the first half (10 to 15 years) of retirement.

This spending rule could be further refined (at the expense of giving up some safety) by adding a prosperity rule (see visual below). If the withdrawal rate falls by more than a pre-set percentage (e.g. 20%) below the initial withdrawal rate, the withdrawal is increased by a defined percentage (e.g. 10%).

Related videos

POST-RETIREMENT: INCOME AND GROWTH

Watch Head of Retail Distribution Peter Kempen provide a summary of the key take-outs from this edition of Corolab:

CORONATION CAPITAL PLUS FUND

Watch this short profile on the objectives of this fund and it's compelling track record:

Disclaimer

SA retail readers

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter