South Africa - Personal

South Africa - Personal

Personal finance

Promising upside from global equities

Current valuations relative to history point to attractive future return prospects.

The Quick Take

- The upside to fair value (FV) for the equity component within our global funds is amongst the highest it has been relative to history

- Our historic portfolio experience shows that in subsequent 1- and 2-year periods, the return on the equity component of our Global Managed Fund was double that of its average return over similar periods

- This gives us comfort that our global funds are currently set up to do well

One of the most challenging things to do as an investor, is to take the appropriate action at a time when you are most concerned about a fund’s performance. However, all things being equal, this typically is the best time to invest. And the reason is simple. Underperformance, backed by long-term conviction in the portfolio make-up, typically means that the fund holdings have become cheaper relative to the market (and often in absolute terms too), increasing the probability of earning higher future returns. Here’s why we are particularly excited about the return prospects for our global multi-asset funds.

A WINDOW PERIOD FOR UPSIDE

The start of 2022 saw global markets flip from strong equity returns to a period dominated by fear as Russia unexpectedly invaded Ukraine, resulting in a slowdown in global growth expectations and rising inflation and interest rates.

Market participants passed a set of known risks very hard, giving way to an aggressive derating, with all of the potential downside being discounted in the share prices – something that resembles a worst-case scenario.

However, what often follows over time is something a little more benign. And because the derating has been so aggressive, a window period for recovery has been created.

ASSESSING THE FUTURE RETURN OPPORTUNITY IN OUR GLOBAL MULTI-ASSET FUNDS

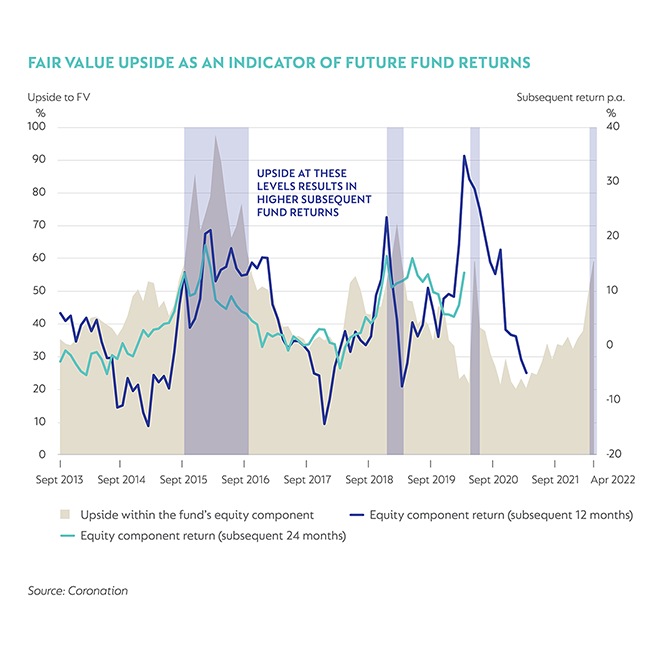

One of the metrics we use to assess the future return opportunity embedded within our funds is upside to fair value (FV). This figure represents our view of what a business is worth (compared to its current market price) several years out into the future, based on our proprietary research.

We currently see upside of around 60% for the equity component of Coronation Global Managed, which translates to an internal rate of return of 15% p.a. This is essentially the FV upside expressed as an annualised rate of return over our research horizon, typically 5-7 years.

The upside for the equity component of the Coronation Global Optimum Growth Fund is even greater at around 75% as a result of higher exposure to emerging markets, specifically China, that has sold off more aggressively.

However, looking at the FV upside figure in isolation means very little. A more useful assessment of this figure is relative to history, which we have demonstrated in the graph below.

What one would expect to see (if your investment research is correct and the market agrees with your assessment of FV) is a correlation between the subsequent fund returns and expected level of upside. Where our upside to FV expectations for global equities (the key building block of Coronation Global Managed) were higher, the fund delivered higher returns in the period that followed. Likewise, where our upside to FV expectations were lower, the fund delivered lower returns.

WE DON’T OFTEN COME ACROSS THIS LEVEL OF UPSIDE

A key takeout from the graph above is how attractive the current upside to FV figure is. Compared to historic observations for the Fund, we have only seen this level of FV upside (>60%) 13% of the time. Furthermore, in the periods that followed FV upside at north of 60%, the Fund's equity component produced, on average, double the average return it achieved over similar measurement periods of 1 and 2 years. This confirms a very strong correlation between return expectations and the level of upside as measured through the aggregation of our research output.

CAVEAT EMPTOR

As with any forecast, it is important to emphasise that there can be no guarantees. As we’ve highlighted before, achieving this level of upside is subject to our investment research being correct and ultimately that market prices for the securities we hold adjust to our level of FV over our research horizon.

What we do know is that the current upside to FV is a very rare occurrence for the Fund, and one that is consistent with higher expected future returns. This gives us comfort that our global multi-asset funds are currently set up to do well, offering attractive entry points for new investments into the funds.

For more detail about the current fund holdings and supporting views, click on the links below.

Or for more detail about the funds, visit the comprehensive fact sheet also available on the links below:

Disclaimer

SA retail readers

SA institutional readers

Global (ex-US) readers

US readers

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter