South Africa - Personal

South Africa - Personal

Naspers has formed an integral part of our client portfolios for more than 15 years. Since we last wrote about it in our September 2015 edition of Corospondent, it has been the best-performing share on the JSE (generating a return of almost 20% p.a.) and has contributed significantly to the performance of our portfolios. While the natural temptation after such a strong run is to lock in some of this outperformance, we continue to believe that Naspers is a company that is trading at a substantial discount to its intrinsic value and is one of the most attractive stocks in our market. As such, it remains the largest equity position across our domestic equity and multi-asset class portfolios.

THE CREATION OF PROSUS

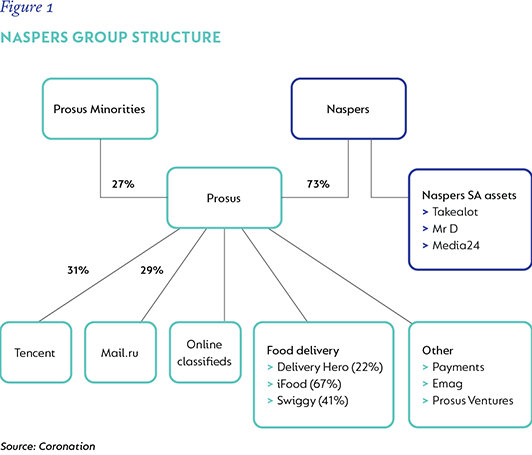

In September 2019, Naspers undertook a major internal restructuring and injected all of its international internet assets (including Tencent, which comprised the bulk of its intrinsic value) into a new vehicle, Prosus, which is separately listed in Amsterdam with a secondary listing on the JSE. Naspers then proceeded to unbundle 26% of its shareholding in Prosus directly to its shareholders. We thought this restructuring initiative was a positive step, because, apart from providing Naspers with access to international capital markets, it also created a very tax-efficient entry point for investors to gain exposure to Tencent, as well as a portfolio of other high-growth internet assets in the online classifieds, payments, etail and food delivery sectors. Furthermore, the structure provides Naspers with additional tools to manage the large discount to intrinsic value at which it currently trades. This was highlighted when they recently sold a portion of their Prosus holding to execute a Naspers share buyback – thereby unlocking over R3 billion in value for Naspers shareholders. Naspers currently owns 72% of Prosus, which comprises virtually all of Naspers’ intrinsic value.

TENCENT – THE JEWEL IN THE CROWN

Weixin (or WeChat), Tencent’s main social network, is central to the company, as it is to Chinese life. It has over one billion monthly active users, and used for business and personal communication, content consumption, payments and utility services. It has become an indispensable tool for everyday life in China. The average user spends 77 minutes per day on the app and Weixin has a roughly 30% share of total internet time spent in China. Weixin’s value to Tencent is primarily as a powerful distribution platform for its various other business lines, including gaming and payments.

Tencent has become the leading developer and publisher of PC and mobile games globally, and gaming currently generates c.30% of its revenue and 40% to 50% of its earnings before interest and tax, respectively. The company has been very successful in developing and publishing hit games such as ‘Honour of Kings’ and ‘PlayerUnknown’s Battlegrounds’ (PUBG, or Peacekeeper Elite as it’s called in China), both of which have exceeded a massive 50 million daily active users (DAUs). As the Chinese market leader, Tencent has a formidable position in gaming, but what many people underappreciate is that they now also own stakes in four of the most successful mobile game development studios in the world – Riot Games, Supercell, TiMi and Quantum, and currently has five of the top 10 DAU games in the world sitting in their portfolio. While the gaming business is undoubtedly exposed to increasing regulatory oversight in China, we still believe the business can grow earnings in the mid-teen percentages over the next few years and, importantly, generate substantial free cash flow to fund Tencent’s other growth initiatives.

The most exciting area within Tencent at present is undoubtedly its digital payments and financial service businesses. We believe that there is still a huge misperception in the market that Tencent can’t be profitable in payments. Our view is that Tencent is currently in an incredibly strong market position versus its competitor, Alipay, and has recently taken steps to increase commission rates and reduce channel fees to ramp up profitability. We think this business will contribute significantly to group profits over the next three to five years. Similarly, Tencent is rolling out other financial services products, such as banking, wealth management and insurance. Given Tencent’s distribution capabilities, together with their enviable treasure trove of user data, we think they are very well positioned to build a substantial and very profitable business.

Tencent also owns a number of nascent businesses that are still being significantly under-monetised, as detailed below:

- It operates the largest online video, music and literature platforms in China, all of which are growing very strongly. It has a near monopoly in music and literature, but vies for leadership in video with iQiyi, a Baidu subsidiary. Video is still heavily loss-making, as Tencent is investing in premium content, and competition has kept subscription fees abnormally low (around $2 per month). However, we believe it can be profitable over time as Tencent gains leverage on its content investments and the competitive environment stabilises. Netflix, which currently has 167 million users (versus Tencent Video’s 106 million users), has a market cap of $167 billion, highlighting the value that can be unlocked from this business in time.

- Weixin remains a largely untapped advertising opportunity. Tencent monetises Weixin at around 20% of Facebook’s monetisation of their Asia Pacific audience, despite their much higher levels of engagement, suggesting signi-ficant upside potential.

- Cloud remains a very fast-growing segment within Tencent. Although they lag the market leader (Alibaba), they are particularly well placed to capitalise on the growing demand for cloud services driven by the gaming and online video industries. As this business scales, it will also turn to profitability.

- Tencent has quietly built up the largest internet/ tech investment portfolio in China, with over 800 investments. This is currently contributing very little to group profitability, despite the company owning stakes in Chinese internet behemoths like Meituan-Dianping (food delivery), JD.com and Pinduoduo (etail),

- 58.com (classifieds), Didi Chuxing (taxi) and Kuaishou (video sharing), and also some global names such as Tesla and Snap. Over time we believe Tencent will realise significant value from this portfolio.

The Tencent share price has proven remarkably resilient this year (flat in US dollars and up 22% in rands). As the world’s largest videogame company, their core business will be boosted by China’s measures to contain the spread of the Covid-19 pandemic. While their advertising, payments and cloud businesses will not be immune to the short-term negative economic effects caused by Covid-19, we see these as transitory hurdles and we believe that recent events, which are a consequence of the pandemic (such as working from home, video meetings and online education), will actually accelerate China’s shift to a digital economy. Furthermore, given Asian countries’ relatively efficient handling of the pandemic outbreak, we expect economies like China to recover relatively more quickly than most other countries in the West, and therefore believe that the risk of Covid-19 undermining the Chinese economy and Tencent’s business to be relatively low.

Tencent is currently trading on 28 times one -year forward earnings (23 times excluding its investment portfolio). This is attractive for a business that we believe can continue to compound revenues and earnings at 20%+ over the next five years.

ATTRACTIVE OPTIONALITY IN THE REMAINING PORTFOLIO

Outside of Tencent, Prosus primarily invests in three key areas – online classifieds, food delivery and payments/fintech. As a collective they are currently loss-making; however, we believe that this masks the true quality and long-term profit potential of this portfolio of assets:

- Online classifieds: Prosus has one of the broadest online classifieds’ portfolios globally, with a presence in most major emerging markets, and dominant positions in Russia, Brazil and Poland. We believe the classifieds model is very attractive, as strong network effects, once dominant, allow the winner to enjoy high margins and low capital expenditure, and therefore high free cash flow conversion. The shifting of advertising budgets from offline to online continues to provide a structural tailwind for the business. In this vertical, there are also a number of consolidation and bolt-on merger and acquisition (M&A) opportunities that we believe can add significant value.

- Food delivery: This is the vertical that will attract the majority of Prosus’ future capital investment. In food delivery, Prosus has three major assets: a 22% stake in Delivery Hero, a 41% stake in Swiggy (India) and a 67% stake in iFood (Latin America, primarily in Brazil). Many of the markets in which these businesses operate lend themselves to a successful food delivery model, i.e. high-income inequality and a well-developed culture of eating out. Food delivery has a large total addressable market and the runway for future growth is certainly long, but as yet unestablished. We also see the food delivery platform model as becoming a natural monopoly once clear leading positions are established; we are therefore very excited about the portfolio of assets that Prosus has established.

- Payments (PayU): Prosus has been growing its portfolio of payment service companies through the acquisition of regional gateway players and technology platforms that facilitate cross-border transactions, and by expanding into adjacent verticals such as lending, remittances and wealth management. India has now become PayU’s largest and fastest growing market, and it offers merchants a solution that can accept and process many different forms of payment with the highest approval rates. The big opportunity for PayU is to leverage its strong position in payments into the large consumer and small to medium credit opportunity sets currently available in the Indian market. While many in the market might disregard the value of this vertical within Prosus, we think it could be a very attractive acquisition target to large global payments players.

THE NOTORIOUS DISCOUNT

Due to its holding company structure, many market participants believe that Naspers (and Prosus) should trade at a large discount to the value of its underlying assets. Our view is quite different. While a small discount can be justified to account for certain frictional costs inherent in the structure, we think it’s important to remember that this is a company that is run by a management team with a proven ability in identifying and capitalising on major media and technological trends. Naspers pioneered pay-TV services in South Africa and was a founding investor in MTN, the largest mobile operator in Africa. It went on to become a major investor in Tencent and Mail.ru, two of the largest internet companies in China and Russia, respectively. More recently, they have embraced ecommerce and built fantastic online classifieds and food delivery portfolios. Furthermore, we think that capital allocation discipline under CEO Bob van Dijk has been excellent. Some examples of this include:

- They have refined their investment portfolio and focused on verticals with the most attractive economics, large addressable markets and where they have the assets with which they can build market-leading positions. In this process they have exited the majority of their etail investments, specifically Allegro, Flipkart and Souq – all at very attractive prices.

- In 2019, Naspers unbundled 100% of Multi- Choice and 26% of Prosus to their shareholders.

- In 2018, they sold a small portion of their Tencent stake at a good price and raised US$10 billion. They have been extremely disciplined in how they deployed this capital and today still have $4.5 billion in cash on their balance sheet. This cash pile is incredibly valuable in the current environment and gives them significant financial flexibility, should attractive M&A opportunities arise.

- Naspers recently sold a portion of their Prosus stake (c 1.5% of Prosus) and used the proceeds (amounting to R22 billion) to fund a buyback of Naspers shares that were trading at a much larger discount to its intrinsic value than Prosus.

ESG ENGAGEMENT DRIVING SHAREHOLDER VALUE

As a large Naspers shareholder, we have engaged extensively with management and the Board of Directors on a number of environmental, social and governance (ESG)-related issues in recent years. One particular area of focus has been on executive remuneration and engaging with the Board in order to improve remuneration structures, and transparency and disclosures around the Remuneration Policy.

In this regard, we note the significant improvements that have been made to date:

- management incentivisation is now more balanced between the value created within Tencent and the value created within the rest of the investment portfolio;

- significant improvements have been made with respect to disclosure and providing a clearer link between strategy, performance, remuneration design, and remuneration outcomes; and

- a share buyback programme has been implemented in order to neutralise the shareholder dilution of share options granted to management.

One ongoing point is that Naspers continues to use long-dated options in order to incentivise management. We believe such long-dated options are significantly more expensive for shareholders than shorter-dated options, and therefore continue to engage with the Board in order to shorten the tenure of such instruments.

CONCLUSION

Prosus currently trades at a c.35% discount to its intrinsic net asset value, while Naspers trades at c.50%. We find these discounts puzzling, given the long-term investment track record as discussed above. As such, we think the market is grossly mispricing these stocks at current levels and has therefore created a fantastic opportunity for long-term investors.

Disclaimer

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter