South Africa - Personal

South Africa - Personal

Economic views

Taking stock

He who is not prepared today, will be less so tomorrow – Ovid

The Quick Take

- Globally, inflation is easing, but in a disjointed manner due to differing in-country dynamics

- With recession still possible in 2024, the outlook for the already-challenged SA economy is strained

- It’s one step forward and two steps back in SA, as amelioration in one sector is offset by deterioration elsewhere

- Underlying resilience and an engaged private sector are providing some nascent reasons for hope

- But the fiscal deterioration will be extremely challenging to remedy in the absence of stronger growth, and large funding requirements are a growing challenge

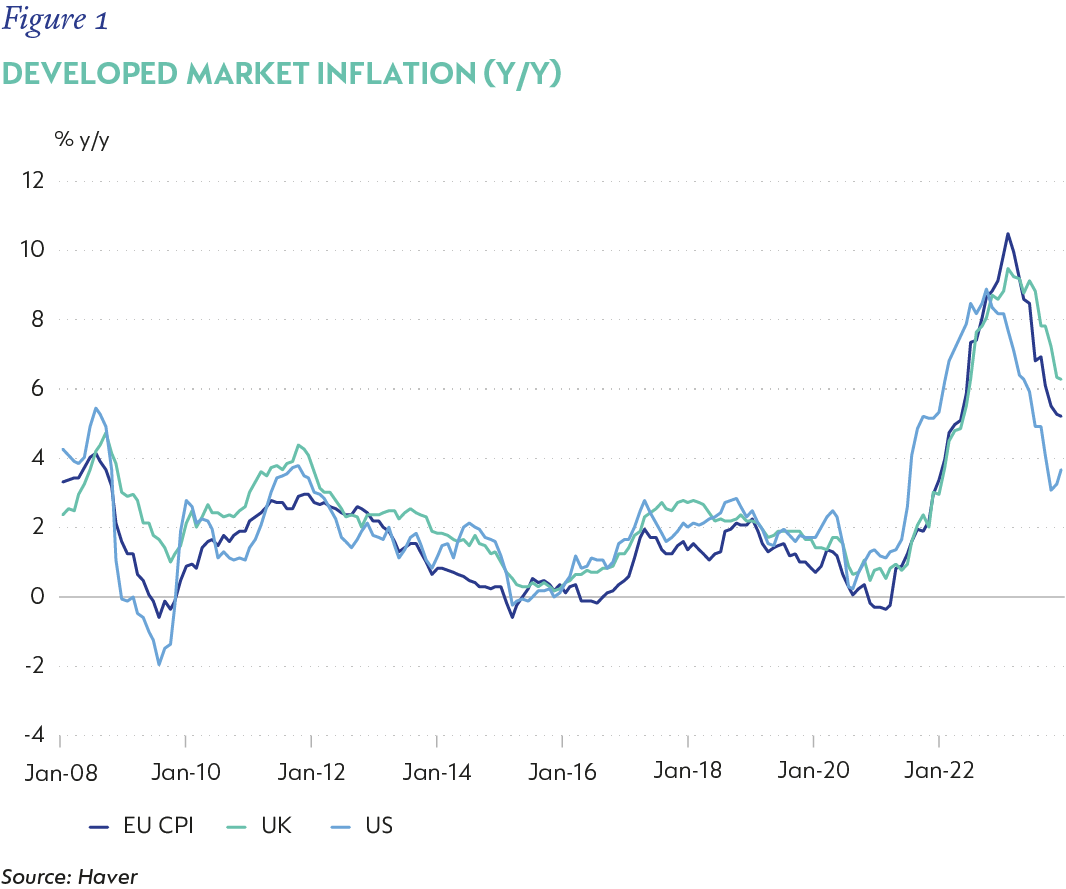

Taking stock of 2023 as we head into the end of the year highlights the degree to which the events of the past three years continue to shape economic outcomes, both globally and at home. In developed markets, inflation remained stubbornly high at the start of the year but has since shown more convincing signs of moderation. Figure 1 shows that headline measures, which capture food and energy prices, slowed the most, but core measures, which include both goods and services, have also started to ease. The challenge remains that underlying economic dynamics within developed economies – as well as many of their emerging peers – differ, and, as a result, the path and pace back into target ranges will vary by country.

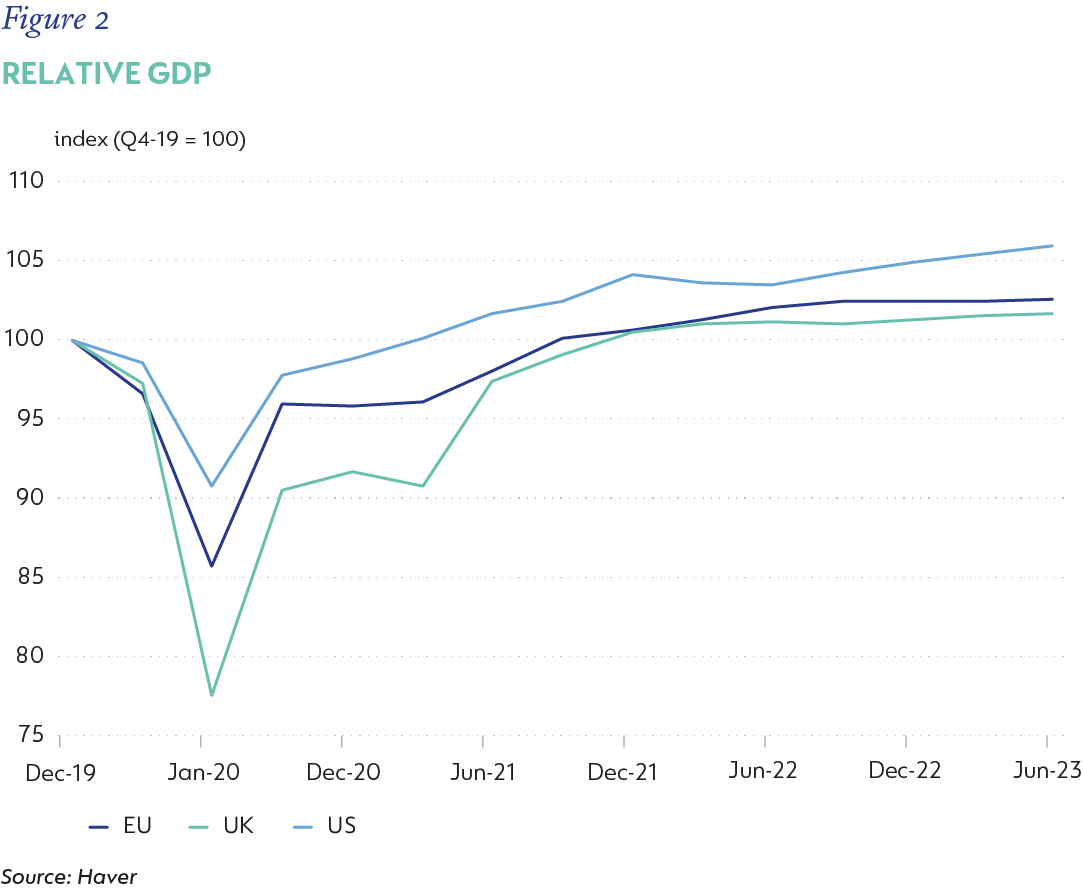

At the same time, economic growth in developed markets has been more resilient than anticipated. High inflation and rising interest rates were expected to dampen demand, erode profitability, and loosen labour markets. This has not fully materialised. Labour markets remain relatively tight, unemployment low and wage growth persistent. In some cases, government funded programmes have also provided a boost for capital expenditure. While growth continues to be weak in Europe, the US is expected to see GDP for the year at about 2.3% (Figure 2).

These dynamics have created a challenging environment for central banks. After relatively committed monetary policy tightening since early 2022, most developed economy central banks are seen to be at or close to peak rates. They have also signalled not only their willingness to raise policy rates further should data suggest it be necessary, but also that policy rates will remain higher for longer to ensure that inflation remains within target. In many cases, such a cautious stance not only reflects uncertainty about the course of inflation, but also changes in post-pandemic economic dynamics, especially tight labour markets, and acknowledges higher levels of government indebtedness.

At this stage, the risk of recession has receded from 2023 but remains live for 2024. This is because the lagged impact of a prolonged cycle of monetary policy tightening coupled with increasingly stringent financial conditions (spurred by stricter bank lending standards, and some risk aversion) could still see economic activity contract. This is an unfavourable backdrop for emerging markets, especially South Africa (SA), which comes with its own idiosyncratic challenges.

SOUTH AFRICA – SO MUCH TO WORRY ABOUT – AND A FEW THINGS WHICH BRING LIGHT

When loadshedding intensified meaningfully at the end of 2022 and into early 2023, economic projections for a modest recovery in growth to about 2% were shattered, and forecasts were revised sharply down. We moved to 0.6%, but views ranged from an outright contraction to broadly flat in 2022.

Despite a nine percentage point reduction in energy availability since late 2022, the domestic economy has also been more resilient than expected: GDP grew 0.4% q/q in the first quarter of 2023, and 0.6% q/q in the second quarter, and could reach 1% this year. A look at the growth drivers shows this remarkable resilience has been the result of a strong pick up in investment spending by the private sector, largely reflecting investment in energy alternatives. Restocking and government spending added to the positive momentum from private investment, but public investment spending continues to drag.

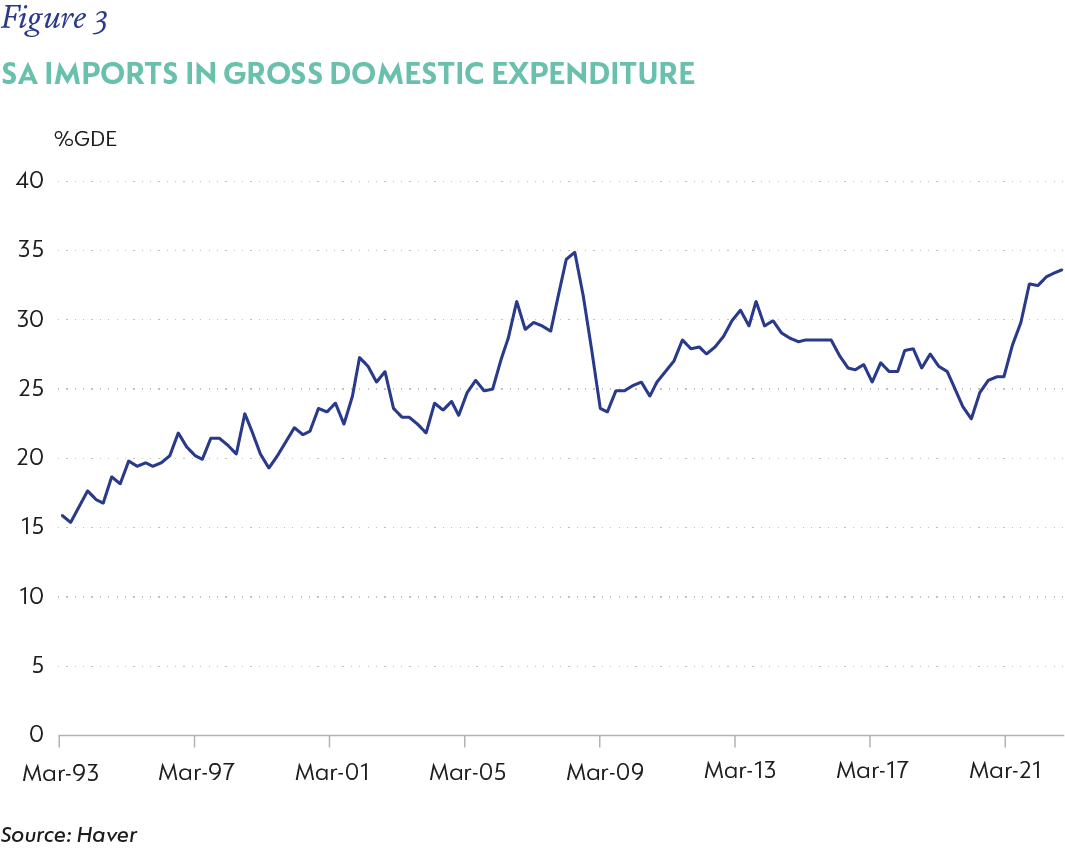

Household spending remains insipid amidst weak employment and below inflation remuneration but has been supported by some credit growth. Net exports suffered the double whammy of weak export performance, hampered by network and logistics failures, and strong import growth associated with private investment. Figure 3 shows that imports are now at their highest as a proportion of domestic expenditure at 33.7% since the 2008/2009 Global Financial Crisis. Unlike then, the rise in imports has not been offset by strong underlying activity, and the increase detracts from growth.

The pace of private energy-related investment is expected to remain elevated, while global growth is unlikely to support either export volumes or prices in coming quarters. It is possible that relieving some of the energy constraints and lower intensity loadshedding will buoy activity and sentiment, perhaps offering some lift to private employment. However, we believe potential momentum is largely capped by the poor working condition of state-owned entities (SOEs), the deterioration in local infrastructure and the slow pace at which these constraints are likely to be effectively addressed. In addition, high interest rates, low earnings and a rising debt burden are expected to continue to weigh on household disposable incomes.

We see these interactions characterising growth dynamics in 2024 and 2025, with a steady easing in energy-related constraints over time. More efficient and effective policy interventions and arrangements with the private sector could materially improve the outlook for broad-based growth recovery. But, while green shoots are emerging in power, pressure is building in transport and water-related services. Overall, these factors cap the rate at which the economy can recover and will continue to weigh on confidence. We see a muted recovery, with GDP growing 1.4% in 2024 and 1.6% in 2025.

PERSISTENT INFLATION CONTINUES TO WEIGH

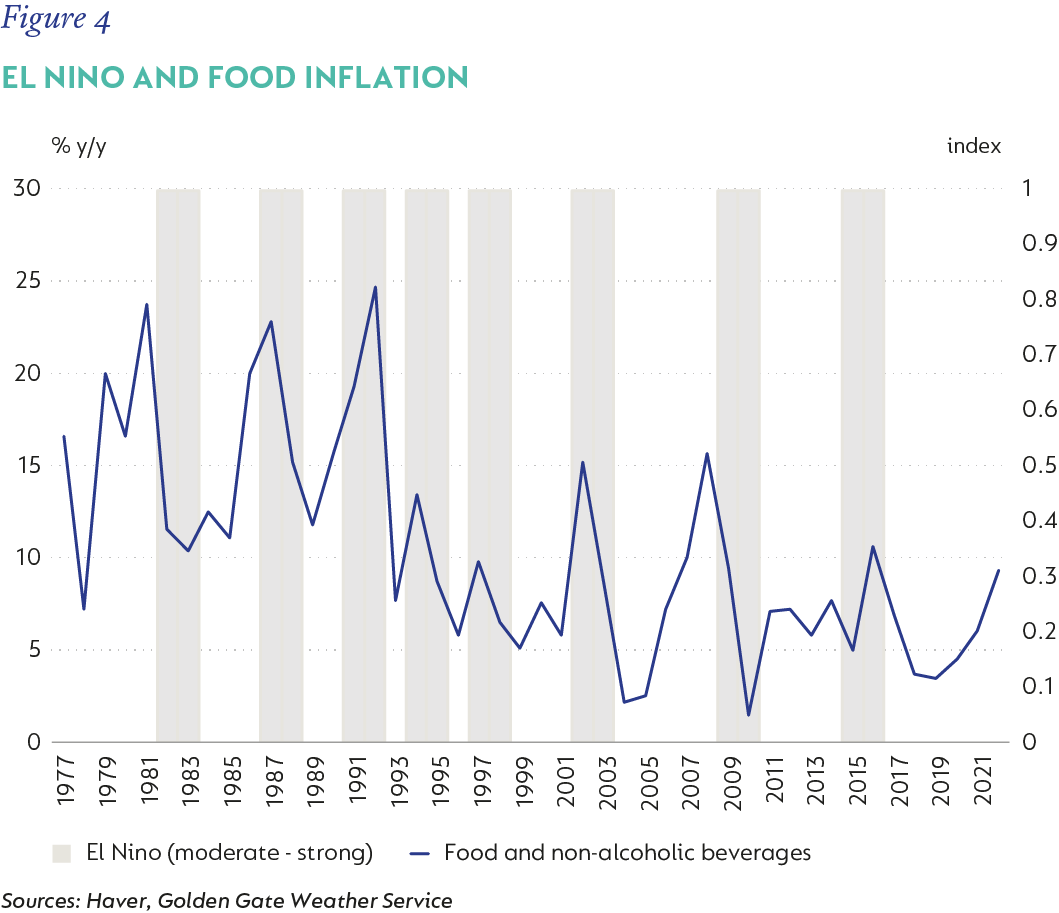

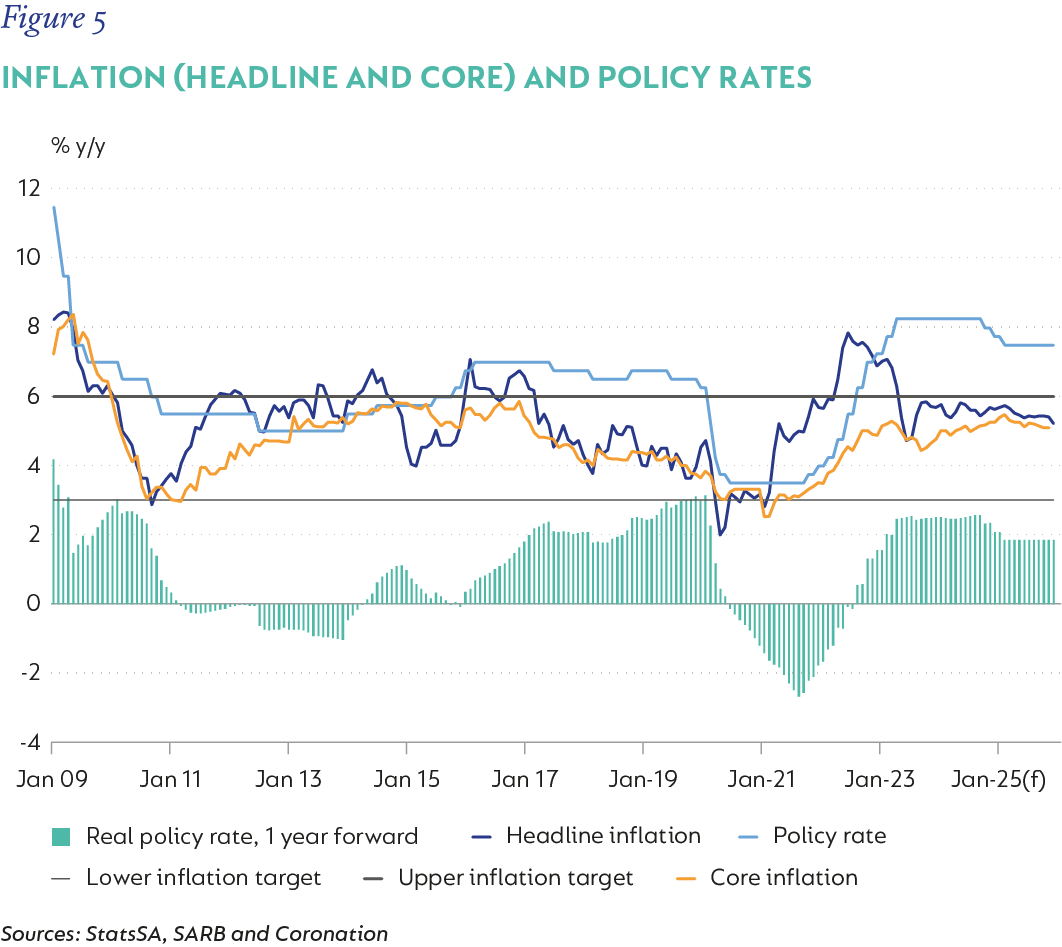

Inflation has slowed from a peak of 7.8% y/y in July 2022 to a low point of 4.7% y/y in July 2023. The moderation has been driven by falling fuel prices and a sharp slowing in food inflation. Figure 4 shows how past El Niño episodes have seen food prices spike either early, or after the weather impact has faded, depending on domestic grain stocks. While current maize stockpiles are more than adequate, these would be materially undermined by a weak harvest next year.

Core inflation has ticked up slowly, from a low point of 2.5% in mid-2021 to 4.8% in August, anchored by weak rental inflation. Despite this relatively benign outcome, risks have started to emerge: the weak currency and surging oil prices have raised retail fuel prices and will impact public transport costs. Core goods prices persist above the 4.5% target, and outside of housing, core services inflation has been relatively high. Price pressures along the supply chain, mostly related to the costs of electricity, transport and anything imported, are likely to contribute to persistence in inflation. As referenced above, evolving weather-related risks could also put pressure on food prices from the second half of 2024.

We expect headline inflation to average 6% in 2023, moderating to an average of 5.5% in 2024.

Figure 5 shows how this unforgiving inflation outlook leaves little room for monetary reprieve. While inflation expectations have turned down from their peaks, they have not reverted to target levels and rising non-core prices could see the recent moderation adapt again. The host of risks to the South African Reserve Bank’s benign baseline forecasts are coming into sharper focus, coupled with a weaker fiscal position may see the central bank ease late in 2024 and will likely limit the cutting cycle to 75 basis points over the next two years.

A STRUGGLING FISCUS

With growth still weak and inflation coming down, the government’s financial position has deteriorated meaningfully this year, from an already vulnerable place. After three years of commodity-related tailwinds, revenue growth is underperforming the expectations set out in the 2023 National Budget. The biggest losses have come from corporate income tax, largely reflecting the decline in mining profits, but also the generally weak operating environment. VAT performance has also been poor, mostly because energy investment-related rebates have picked up sharply, but, at headline levels, weak consumer spending has also weighed. Interestingly, personal income tax has held up well – an unexpected source of resilience. In aggregate, we expect revenues to underperform the Budget estimate by about R45-50 billion in 2023/2024.

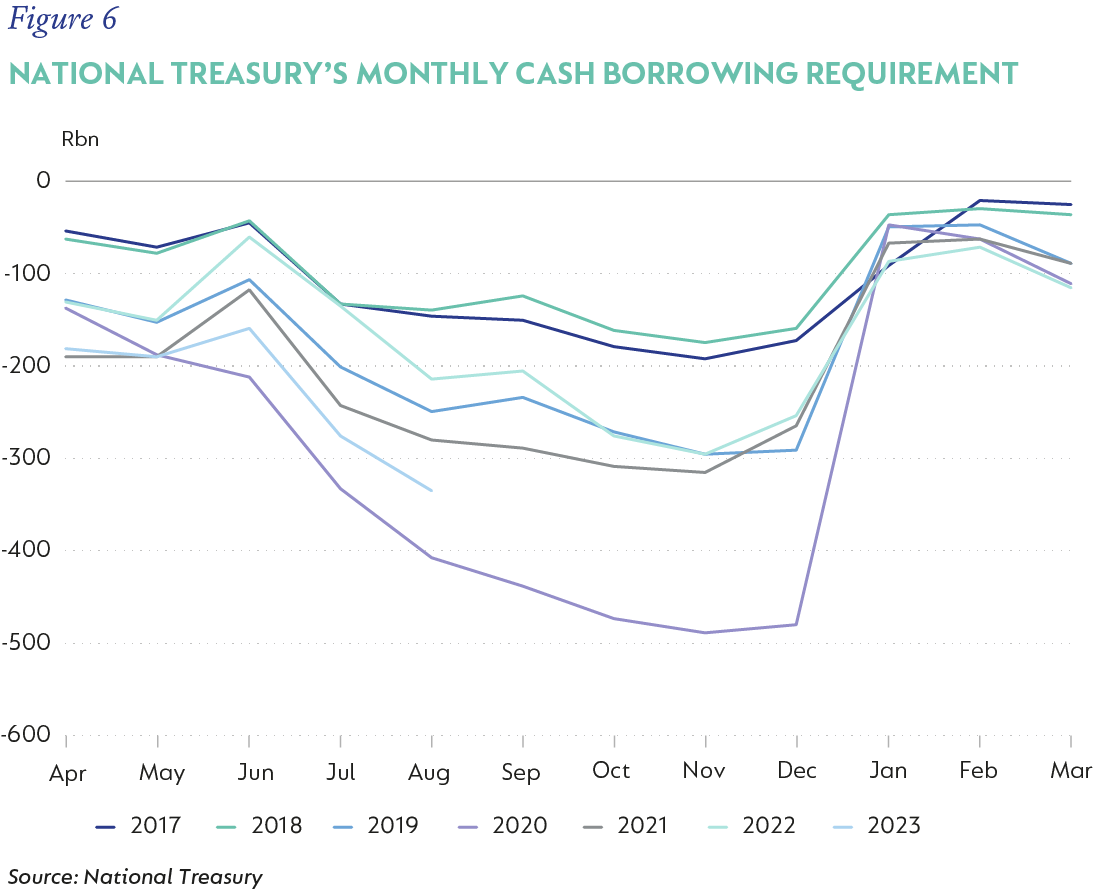

Spending is running ahead. Most of the excess is due to the wage agreement that was signed after the tabling of the 2023 Budget, and which exceeded the allocated envelope. This could add about R40 billion to this year’s baseline. Next up is a sharp rise in debt service costs, boosted by discounted issuance and adjustments to inflation-linked bonds, likely to be joined by some additional SOE assistance, and, later in the fiscal year, the risk of an increase in election-related spending. Reallocations may offset some of the shortfall, but we see a deficit measuring 5.6% of GDP, excluding the allocation to Eskom, and 6.7% when this is included. Borrowing has risen materially as a result (Figure 6).

Prospects for a material consolidation – in the absence of a strong recovery in growth – are relatively limited. The multi-year wage agreement adds R140 billion to the baseline over three years, including the current one. Departmental ability to adequately manage headcount or other costs is not immediately clear and may lead to a further deterioration in service delivery.

Provisional allocations for SOE support ex-Eskom are almost non-existent, and the baseline makes no itemised allocation to the extension of the Social Relief of Distress Grant, or a possible successor. There is also no room for election spending, emergency interventions for Transnet or additional provision for crumbling water infrastructure. The proposed National Health Insurance is largely unfunded, and free tertiary education may again exceed budgeted amounts in the future. National Treasury has made some provisions in the contingency and unallocated reserves, but these are not likely to be enough. Savings from allocations made but unspent are possible offsets, but National Treasury will be unable to maintain the trajectory of the projections in the 2023 Budget. We expect the main budget deficit to be between 5.5% and 6% of GDP (excluding financial transfers to Eskom) over the next three years, which will see debt continue to accumulate to over 80% of GDP by 2025/2026.

More worryingly, the ease with which government can fund the budget shortfall is coming under pressure at a time when the public borrowing requirement, which not only includes the main budget deficit but maturing debt too, is set to grow. This means government will bring more and more paper to a market whose own resources are shrinking.

CRITICAL DECISIONS AHEAD

This increasingly precarious juncture focuses attention on the critical issues which need deliberate and dedicated attention: the provision of core economic services, including some electricity, aspects of transport and, possibly, critical water services will by necessity move more to the private sector. It is possible this trend will replicate in other parts of the public service. By the end of 2024, an additional 2043 megawatts of private power should supplement Eskom’s availability factor, which could eliminate about two stages of loadshedding. The mining sector is in ongoing negotiations with Transnet to run and manage critical rail infrastructure. There have been initiatives to open port operations to the private sector. Thankfully, the agricultural sector has been an ongoing positive contributor to growth, and tourism is expected to continue its slow recovery, aided by the activation of direct routes to Cape Town International for the summer season.

On balance these dynamics should be employment accretive and should underpin an improvement in confidence. The election in the first half of next year remains a risk to sentiment, but we expect that if there are any resultant policy-related changes to growth, they will still be relatively slow.

SA has been on a long road of decelerating growth, undermined by disintegrating infrastructure, poor service delivery, weak policy execution and great uncertainty. The pandemic exacerbated these trends. But underlying resilience, adaptability and a willing private sector remain critical drivers of a slow recovery.

Disclaimer

SA retail readers

SA institutional readers

Global (ex-US) readers

US readers

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter