South Africa - Personal

South Africa - Personal

The Fund returned -0.28% in September, bringing its 12-month total return to 9.63%, ahead of cash (7.30%) and its benchmark (8.06%) over the same year. We continue to believe that current positioning offers the best probability of achieving the Fund's cash + 2% objective over the medium to longer term.

Global markets received a rude awakening towards the end of the third quarter of 2023 (Q3-23). The rise in oil prices to above US$100 per barrel, inflation prints pointing to a slower deceleration in core inflation and increased central bank rhetoric of keeping rates higher for longer caused a surge in global bond yields. Stubbornly wide budget deficits, already-high debt loads and an almost doubling of funding costs also added fuel to the bond sell-off. Although slightly better placed due to higher embedded risk premium, emerging markets did not escape unscathed and moved weaker in sympathy with the global bond and risk sell-off.

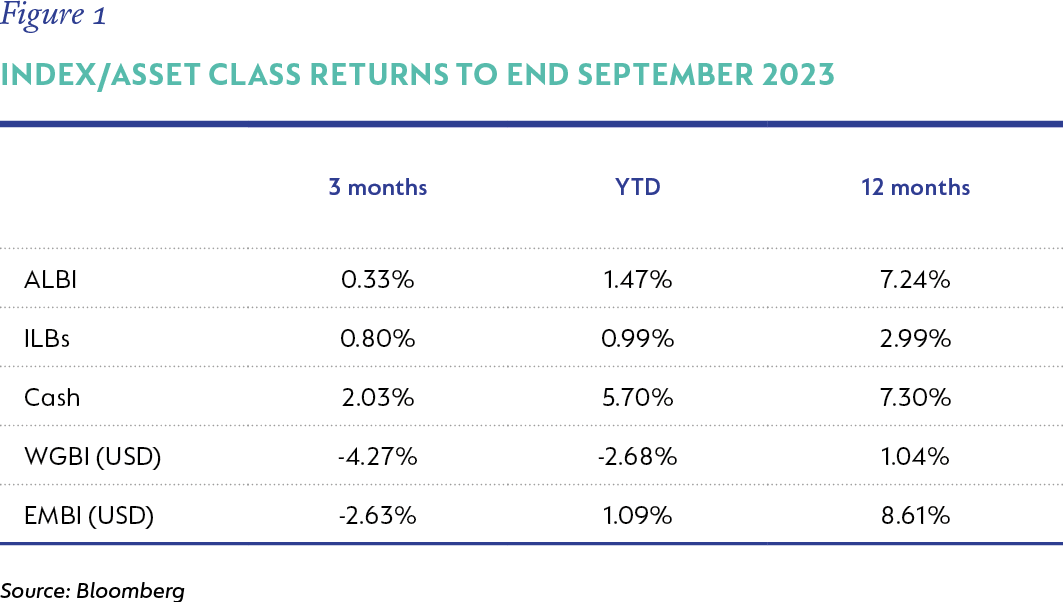

South African (SA) bond yields were 65 basis points (bps) higher than at the end of the last quarter, resulting in a negative FTSE/JSE All Bond Index (ALBI) return of -0.33% over the quarter. This was behind the 0.80% return from inflation-linked bonds (ILBs), which afforded some protection due to elevated real yields. However, the ALBI has still significantly outperformed ILBs both year to date (1.47% versus 0.99%) and over the last 12 months (7.24% versus 2.99%). Despite underperforming cash over the last quarter and year to date, bonds have still eked out a return slightly closer to that of cash over the last 12 months (see table below). Globally, developed market bonds continue to lag the performance of emerging market bonds. Over the last quarter, with the 75bps rise in US 10-year Treasury yields, the FTSE World Government Bond Index (WGBI) was down -4.27% compared to the JPMorgan Emerging Market Bond Index (EMBI), which was down -2.63%. Over the last year, the outperformance is starker at 8.61% (EMBI) versus 1.04% (WGBI).

The rand ended the month at R18.92/US$1. SA’s idiosyncratic problems and the turn in global risk sentiment continued to weigh on the local currency. Offshore credit assets and certain developed market bonds have improved in valuation, making them look very attractive. The Fund has utilised a significant part of its offshore allowance to invest in these assets. When valuations are stretched, the Fund will hedge/unhedge portions of its exposure back into rands/dollars by selling/buying JSE-traded currency futures (US dollars, UK pounds, and euros). These instruments are used to adjust the Fund’s exposure synthetically, allowing it to maintain its core holdings in offshore assets.

In SA, the South African Reserve Bank (SARB) left the repo rate unchanged at 8.25% at the September MPC meeting. There was again a split in the votes, with two members voting for a 25bps increase while three voted to hold. The MPC still assesses risks to inflation to be to the upside, exacerbated by the weak currency, a deterioration in SA’s fiscal position and rising commodity prices. Nevertheless, the SARB revised its core inflation forecast to 4.9% for 2023 from 5.2%, noting that global core inflation remains sticky and risks to rising food prices and weak currency remain a concern. Overall, the MPC maintained its hawkish tone and will likely hold rates high for a long time.

Headline inflation increased to 4.8% y/y in August from 4.7% y/y in July, while core inflation also rose to 4.8% y/y from 4.7%. The main contributor to the headline uptick was the August fuel price hike, partly offset by another easing in food inflation. Rising oil prices will contribute towards high fuel costs in the coming months and will likely limit the moderating path of headline inflation into early 2024.

FUND POSITIONING

At the end of September, shorter-dated fixed-rate negotiable certificates of deposit (NCDs) traded at 9.39% (three-year) and 10.04% (five-year), significantly higher than the close at the end of the previous month. Our inflation expectations suggest that the current pricing of these instruments remains attractive due to their lower modified duration and, hence, high breakeven relative to cash. In addition, NCDs have the added benefit of being liquid, thus aligning the Fund's liquidity with the needs of its investors. The Fund continues to hold decent exposure to these instruments (fewer floating than fixed), but we will remain cautious and selective when increasing exposure.

Fiscally, SA remains in a tight spot. Revenue is expected to deteriorate due to lower growth this year, and pressures on expenditure remain high. The government effectively funds itself at between 8.5% and 9.5% (a combination of short- and long-term borrowing), while nominal growth is, at best, 6.0%. There are only three ways out of this crisis:

- Austerity: we could enter into a period of extreme austerity by cutting spending or placing a limit on spending proportionate to revenue. This seems highly unlikely since unemployment is so high, fixed expenditure (wages, grants, interest costs) is at 64% of total expenditure, and we are heading into an election year.

- Kickstart growth: we could increase the nominal growth rate by increasing the real growth, but this would require real growth in the 3% to 4% range (assuming inflation at 5.5%) so that you are at least growing in line with your cost of funding. This is entirely possible but would require drastic and swift action, which seems unlikely in the short term from the current administration.

- Reduce costs: we could bring our cost of funding down, either by changing the funding mix or by utilising resources that could favour a compression in the funding cost.

A combination of the last two would be optimal, but the process around it needs to start now; otherwise, SA faces the harsh reality of a forced debt restructuring as budget deficits remain stubbornly around 6.0% of GDP and our debt load flirts with the prospect of being 90% of GDP.

Over the recent past, the pricing of SA assets, through performance relative to other emerging markets and increased required risk premium, priced a large portion of this fiscal deterioration in.

SA’s fundamental outlook continues to be plagued by inflation that will remain above the midpoint of the target band, a deteriorating fiscal outlook and very little confidence in the current administration’s ability to correct the trajectory. Local assets have continued to trade poorly, with the risk premium embedded in local bonds remaining elevated. The recent turmoil in global bond markets has added a further spanner to the works as the prospect of higher rates for longer and a deteriorating debt outlook weighs on bond yields. However, the current valuation of global bond yields suggests an increased margin of safety, which could provide some comfort to global bond investors. This, combined with the healthy risk premium on offer in local bond yields, should support our local bond market.

ILBs are securities designed to help protect investors against inflation. They are indexed to inflation so that the principal amount invested and, hence, the interest payments rise and fall with the inflation rate. ILBs have offered protection to investors over the last quarter. However, current breakeven inflation across the ILB curve averages between 5.5% and 6%, which is well above even our expectations for inflation over the medium term. Only the short-dated ILB (I2025, 1.3 years to maturity) flags as cheap from a valuation perspective. Risks on the inflation front remain elevated. However, one has to acknowledge that valuation has shifted more in favour of nominals at this stage. As such, although we still believe ILBs warrant a position in bond portfolios due to their inherent inflation protection, some moderation of that allocation in favour of nominal bonds is prudent at this stage.

Credit markets have remained relatively subdued. Net issuance this year has been paltry, with most of the issuance on the back of refinancing maturing bank-senior and subordinated debt. Despite the poor fundamental backdrop in SA, credit spreads have continued to tighten this year as net supply has dwindled. Senior bank credit has compressed significantly, with the gap between five- and seven-year terms almost non-existent. The compression of term premiums in credit spreads indicates a market hungry for yield at any cost and not what one would expect in the poor economic environment. Subordinated bank credit (AT1 and AT2) has seen a similar compression, with AT2 spreads now just 30-40bps above senior spreads. This compression is quite dramatic, and although banks remain well-capitalised and very far from failure, given the nature of the instruments, we feel current pricing to be too optimistic. Given their tight valuations, we consider current credit spreads unattractive and see better alternatives elsewhere. Current pricing of global interest rates and credit markets offers investors an attractive, risk-adjusted opportunity.

The local listed property sector was down 3.76% over the month, bringing its 12-month return to 12.91%. Operational performance will remain in the spotlight as an indicator of the pace and depth of the sector’s recovery. The current poor growth outlook, combined with an increase in cost base due to higher administered prices and second-round effects on loadshedding, will weigh on the sector’s earnings in the coming year. We believe that one must remain cautious due to the high levels of uncertainty around the strength and durability of the local recovery.

OUTLOOK

We remain vigilant of the risks from the dislocations between stretched valuations and the local economy's underlying fundamentals. However, we believe that the Fund’s current positioning correctly reflects appropriate levels of caution. The Fund’s yield of 10.35% (before fees) remains attractive relative to its duration risk. We continue to believe that this yield is an adequate proxy for expected Fund performance over the next 12 months.

As is evident, we remain cautious in our management of the Fund. We continue to invest only in assets and instruments that we believe have the correct risk and term premium to limit investor downside and enhance yield.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter