South Africa - Personal

South Africa - Personal

Investment views

Opportunities in the energy transition

The global energy mix is changing and presenting investment opportunities.

The Quick Take

- The transition from fossil fuels to renewables for energy generation is driven by climate and security considerations

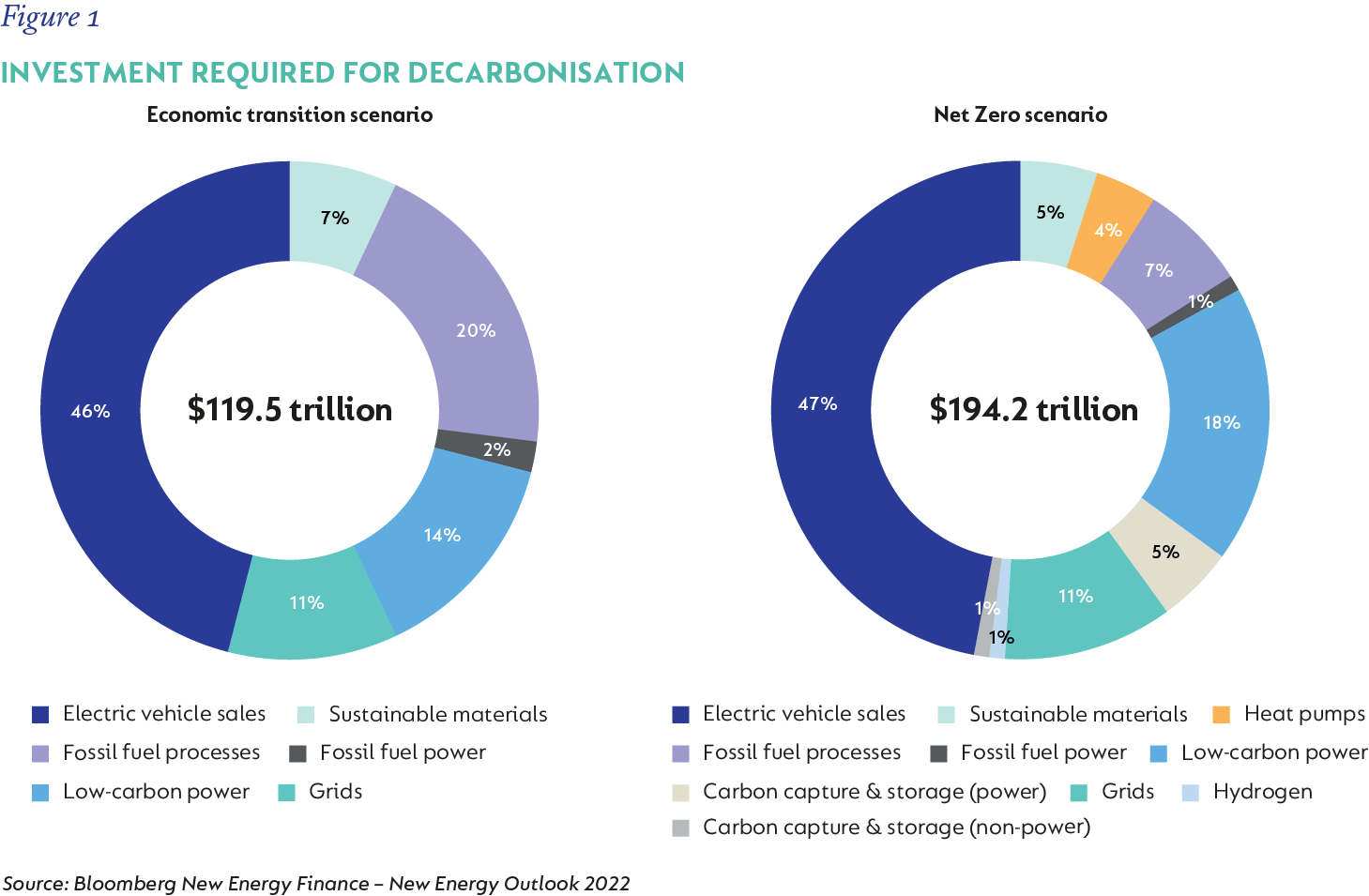

- Near-term renewables growth will be significant and also costly – to achieve Net Zero (if at all) will cost upwards of US$190trn

- While the transition is inevitable, it faces both economic and political headwinds

- We see opportunity in the transmission and distribution grid – new builds and maintenance

We are in the era of electrification. In multiple industries and use cases, the energy mix is undergoing structural change. Energy that was historically provided by burning fossil fuels, such as gasoline in transportation and natural gas in residential heating, is slowly being replaced by electricity generated from renewable sources. The primary reasons for this change are environmental considerations and energy security.

The Paris Climate Accord adopted in 2015 led to widespread agreement amongst countries to co-operate in combating global warming, and prompted nations around the world to adopt Net Zero targets, in the form of commitments to eliminate carbon dioxide emissions within a few decades. Major Western economies, such as the European Union, the UK and the US, have committed to balance their CO2 emissions with removal of greenhouse gases in the atmosphere to reach Net Zero by 2050.

At the same time, geopolitical risks are driving a desire for greater energy independence and resilience in the supply chain. For instance, spikes in natural gas prices as a result of the war in Ukraine have shone the spotlight on European reliance on Russian gas and increased the urgency of diversifying sources of energy.

ECONOMIES OF SCALE IN PLAY; BUT COSTS STILL SIGNIFICANT

These long-term forces are leading to significant growth in renewable generation capacity. While the overall share of energy demand currently being met by renewables is still small, this is projected to grow more than fivefold over the next two decades. For instance, in the UK, renewables account for 38%, with a target for fully decarbonising electricity generation by 2035. In Denmark, wind power already contributes 53% of the total electricity supply. NextEra, a US-based utility, has built three gigawatts (GW) worth of solar generation capacity, enough to power more than half a million homes.

None of this growth is free. Bloomberg New Energy Finance estimates it will cost more than US$190 trillion over the next 30 years to reach Net Zero (Figure 1). Even if the world were to fall short in fully decarbonising, growing electricity demand is likely to absorb almost US$120 trillion in investment by 2050.

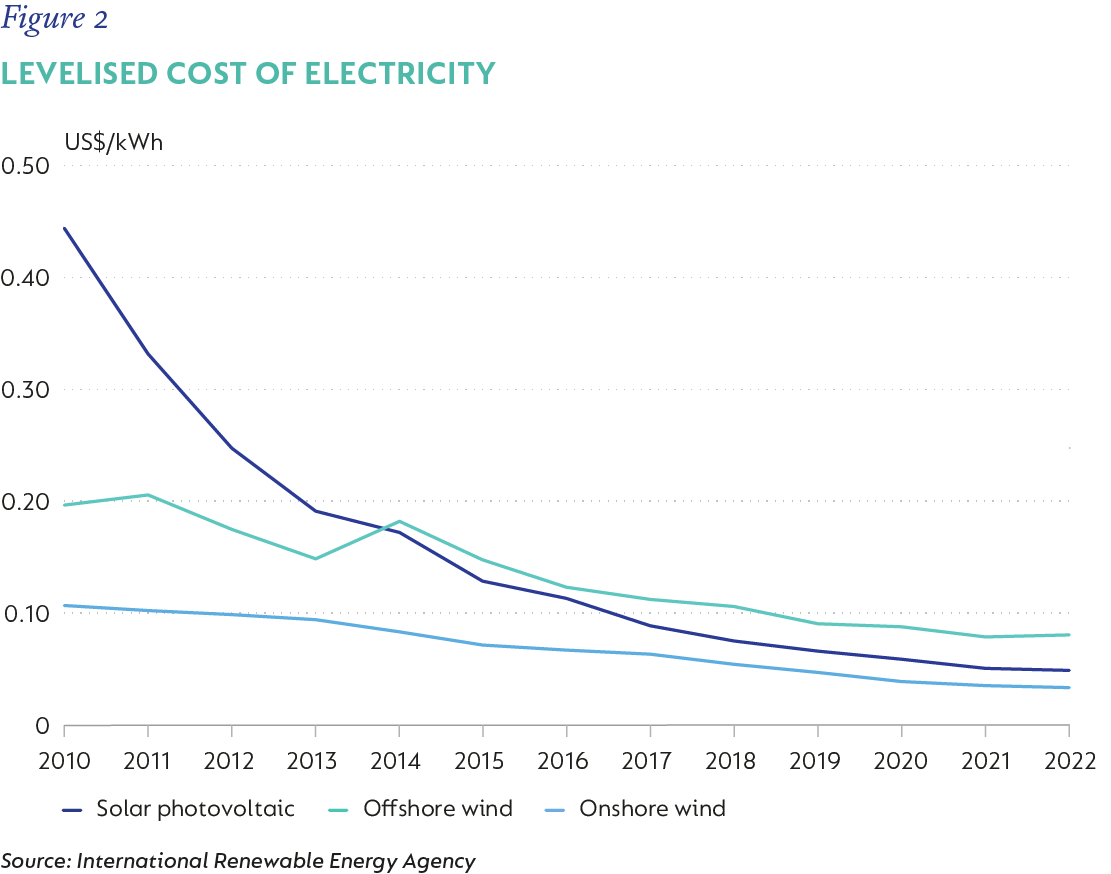

The standalone economics of renewable generation has improved significantly over the past decade and, in many cases, are now cheaper than fossil fuels. For instance, the levelised cost of electricity production for solar in the US is estimated to have fallen from US$0.24/kilowatt hour (kWh) in 2010 to US$0.06/kWh in 2022, and is now cheaper than coal and gas. Likewise, offshore wind in Denmark is producing electricity at US$0.04/kWh. Figure 2 shows how technological advances and manufacturing scale have flattened the cost curve.

However, that is not yet universally true. Across the world, government support has still been necessary to spur the development and ensure the viability of the green energy sector. This has taken the form of support for shifting demand as well as subsidising generation. For instance, in Sweden consumers were offered subsidies of close to US$6 000 to switch to electric vehicles; Europe has proposed a ban on the sale of all internal combustion vehicles by 2035; and, the UK is offering subsidies to households that switch from oil or gas to electric heat pumps for domestic heating. In the US, substantial amounts of funding have been earmarked for the energy transition, with US$400 billion in funding available from the Infrastructure, Investment and Jobs Act, as well as the Inflation Reduction Act.

HEADWINDS TO TRANSITION

Who will ultimately bear the cost of the energy transition is, to some extent, still an open question (with answers that are vulnerable to change depending on the election cycle). In the UK, for instance, disagreement on the timeline and funding for certain Net Zero initiatives has emerged as a potential wedge between the Conservative and Labour Parties ahead of a potential election in 2024.

Renewable generation, which is at the core of the energy transition, is still somewhat boom-bust and remains reliant on government support. For instance, the euphoria that surrounded offshore wind developers has fizzled out, as raw material inflation and rising interest rates have increased the cost of some projects by up to 40% over the past 18 months. Recently, Swedish power giant Vattenfall abandoned a project in the North Sea; Danish player Ørsted announced a major impairment of its US projects (contributing to a 70% share price decline over the past two years); and, the most recent round of auctions in the UK failed to attract a single bid, since the level of price support offered by the government was too low for projects to be viable. While developers have the option to proceed without government support, and assume the risk of volatile wholesale electricity prices, the ability to fund projects with long-term debt is predicated on very stable revenues.

The implication for investors is that while powerful secular forces and large budgets are creating investment opportunities across the value chain, there is still a lot of uncertainty to navigate. Some areas of disruption are very visible, such as the rapid emergence of the electric vehicle industry in China, where more than 100 new original equipment manufacturers (OEMs) are competing for domestic market share, and increasingly becoming contenders in the export market.

Providers of the capital equipment required to build out the infrastructure are likely beneficiaries, such as the manufacturers of wind turbines or solar panels for renewable generation, or transformers and switchgear for additional grid connections. Lastly, utilities will be deploying significant amounts of capital in building out generation, transmission and distribution grid capacity.

OPPORTUNITY LIES IN THE GLOBAL GRID

We see an attractive opportunity for investment in the transmission and distribution infrastructure in a number of markets. Expanded transmission networks are critical for connecting new renewable generation to end users, and in many cases, are a key bottleneck today. Renewable generation is often built in locations without any existing transmission capacity, such as solar plants in the Mojave Desert or offshore wind farms in the North Sea. Renewable energy also tends to be far more intermittent and unpredictable – the sun doesn’t always shine, and the wind doesn’t always blow. This requires a greater degree of resilience and network intelligence to be built into the grid.

Local distribution networks, in turn, are likely to see significantly higher demand from applications like electric vehicle charging, and replacing gas boilers with electric heat pumps. For instance, charging an electric vehicle could increase the average household’s electricity usage by more than a third, and in some cases even more. The higher load will, in many cases, necessitate investment in incremental capacity.

At the same time, much of the existing infrastructure in many developed markets is reaching the end of their useful life, and require replacing. For instance, grid investment in Europe peaked in the 1960s, resulting in close to a third of the grid being older than 40 years, which is the typical lifespan for important network components such as transformers.

As a result, the level of capital investment in electricity transmission networks is likely to meaningfully increase in coming years relative to the past.

The owners and operators of transmission networks are typically regulated entities. They are compensated for maintaining sufficient network capacity, independent of the total amount of power consumed. Generally speaking, investment in expanding the network is recovered through an allowed return on capital, which is set by the regulator in each jurisdiction. Therefore, transmission operators in favourable markets should be able to grow their asset base at a faster rate than they have historically, all while earning a highly secure rate of return in excess of their cost of capital.

Regulators have a difficult trade-off to make in limiting the impact to consumers’ bill, while also providing sufficient incentive for the asset owners to make the necessary investments. The impact of this tension is proportionately less acute for transmission than other portions of the value chain. In the UK for instance, transmission only accounts for around 5% of a customer’s overall electricity bill. Any incremental recovery of expenditure on the transmission network will therefore have a relatively small impact on the overall cost to the consumer and may thus be more easily absorbed than other portions of the energy transition.

SELECTIVE EXPOSURE TO LONG-TERM SECULAR THEME

National Grid is the largest owner and operator of electricity transmission and distribution infrastructure in the UK, as well as in Massachusetts and New York in the US. It was formed through privatisation of the British industry in 1990; originally owned by 12 regional electricity companies, National Grid was listed on the London Stock Exchange in 1995.

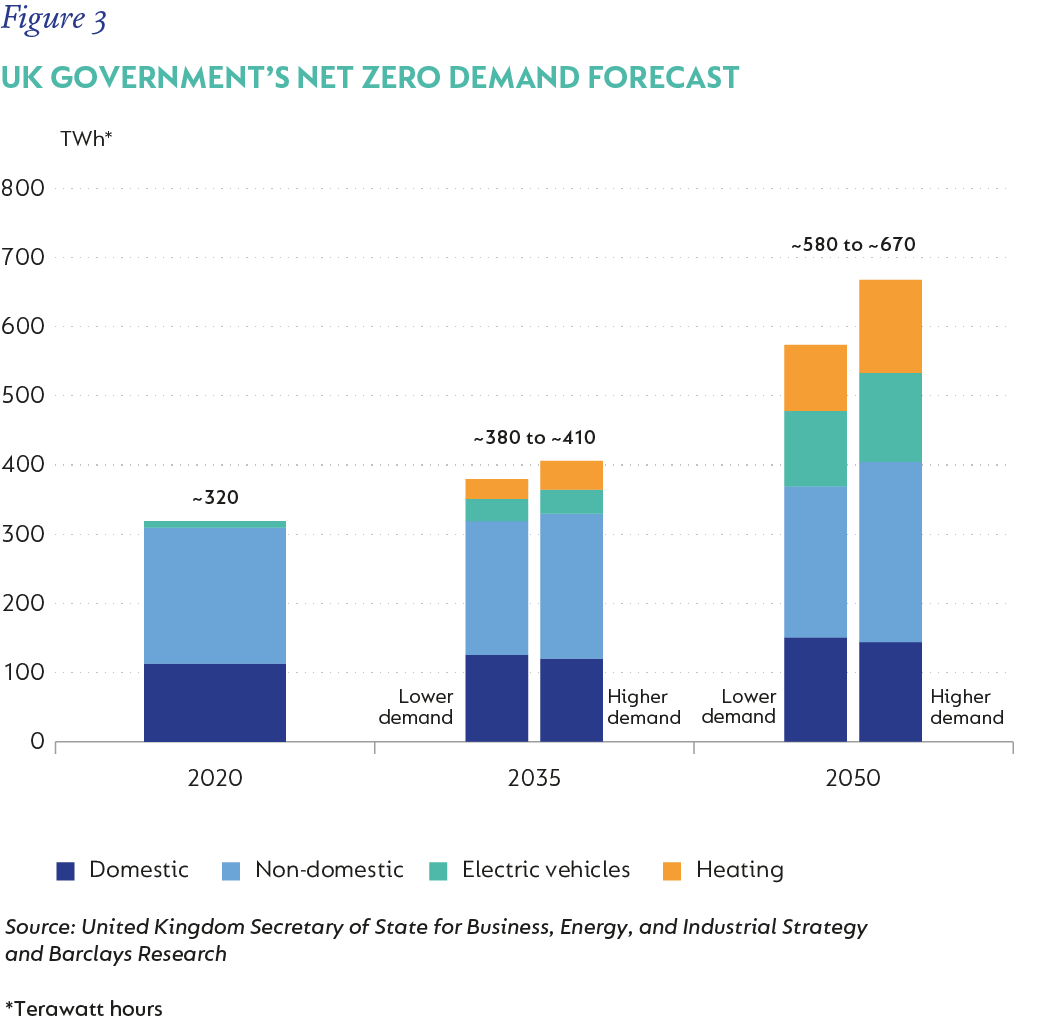

The business operates overwhelmingly in jurisdictions with clear long-term ambitions for decarbonisation, and a stable regulatory environment. For instance, Figure 3 shows how the UK, its largest market, has legislated targets in place to achieve Net Zero by 2050. In order to achieve this, the government has a stated aim of building 50GW of offshore wind capacity, all of which will need to be connected to the transmission network.

National Grid will invest c.£40 billion in infrastructure over the next five years, resulting in approximately an 8% to 10% annual growth in their asset base, while earning a double digit return on its investment. Given the regulated nature of the business, it has a high degree of visibility for this growth. At the same time, the company has a long history of outperformance against its regulatory targets, which results in both higher returns to shareholders, as well as lower bills for customers.

Despite the significant acceleration in investment requirement, National Grid has ample balance sheet capacity, and can fund its growth while maintaining a very generous dividend (currently 6% dividend yield).

The stock is not dearly priced either. At a c.14 times price:earnings multiple, or a 25% premium to the value of its regulated assets, National Grid is trading at a discount to historical levels, and well below the market. Given the structural nature of the energy transition, and the grid’s critical enabling role therein, we see a very long runway for continued reinvestment in growth, offering shareholders a double-digit long-term rate of return, with a relatively low correlation to equity markets.

Disclaimer

SA retail readers

SA institutional readers

Global (ex-US) readers

US readers

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter