South Africa - Personal

South Africa - Personal

TO SET THE tone for the start of the new decade, we have asked our Personal Investments team for their top investment tips. We have published 10 of their contributions in this edition. You’ll notice some common themes coming through. Look out for part two in the next edition of Corospondent, due out in April 2020.

Just get started – Julian Band

If you remember nothing else, remember this. One of the secrets to achieving your goals is simply taking the first step, and it’s no different when it comes to investing. You can start small, from as little as R500 a month, and build up from there. Once you’re comfortable that you are invested in the right fund for your needs, you can ramp up your investment. But get started. Today. Because every day is an opportunity to grow your wealth.

Save first, spend later – Dorette Brits

Looking at the modern era we live in, our world revolves around spending money on experiences instead of things, a need for instant gratification and FOMO (Fear of Missing Out), or the YOLO (You Only Live Once) mentality leading to the “enjoy your money today, don’t worry about tomorrow” way of living. We all spend time trying to discover the key to wealth creation, or how to become rich quick. The simple answer to this question is, there is no such thing as getting rich quickly.

There are, however, two universal truths that will help you to maximise your money:

- Pay yourself first: This means prioritising your savings and investments above other budget items and living on what is left.

- Harness the power of compound interest: Every great force we encounter in our world didn’t always start that way. A snowflake turns into an avalanche by first becoming a snowball.

Even if you start small, say with R500 a month, which might not sound like much, enter the effect of compounding and voilà, your snowflakes may be the start of an avalanche. Assuming a growth rate of 10% over a 20-year period, your small FOMO sacrifice will amount to nearly R360 000. So, what is the moral of my story? “Don’t save what is left after spending, spend what is left after saving.” – Warren Buffett

Have a realistic time horizon – Peter Kempen

Everyone who starts to work for a company starts investing on that day through their mandatory contribution to the company’s retirement fund. Those that work for themselves or derive an income from other sources may only start investing once their business is off the ground, debts are settled, and surplus funds are available. Regardless of the start date, once the process has begun it never ends, as almost everyone will need to have investments till the day they die.

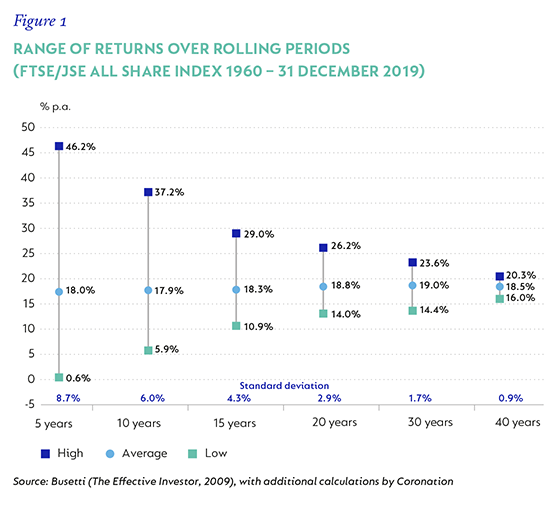

In effect, your time horizon should therefore be from the day you start investing, for your lifetime, and likely beyond. If you start investing in your early 20s that may be a period of 50+ years, and even if you retire at 60 your investment time horizon may be another 25 years. You also need to consider what happens after you die, as investments might be left to beneficiaries who are much younger and have long investment time horizons. Following that logic, the time horizon for many investors should be perpetual. Yet, if you ask most investors what their time horizon is, the bulk of responses will be around the five- or 10-year mark.

Ironically, performance from growth assets becomes a lot more predictable over a longer time horizon and predictability is lowest for periods <10 years, as shown in Figure 1.

Most investors therefore need to reconsider their time horizon carefully. The longer the time horizon, the easier it becomes to manage risk, stick to a strategy, overcome emotions and reap the benefits of compounding, which are discussed elsewhere in this article.

Cash is not king – Amika Pillay

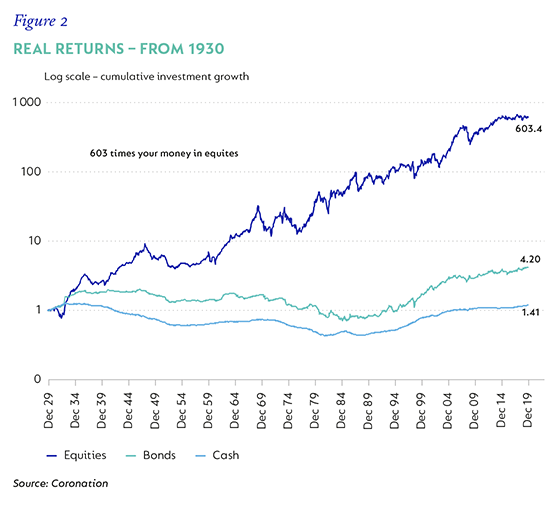

The phrase ‘cash is king’ suggests that money in the bank is more valuable than any other form of investment. In periods when higher risk investments deliver disappointing returns, this belief becomes more widely accepted, with many investors developing a strong preference to hold their money in cash. The desire to not see investment values going backward supersedes every other financial planning consideration. Long-term objectives are sacrificed in the pursuit of ‘safety’ in the shorter term. While this reaction is understandable, it ultimately leads to poor outcomes. Why? While an investment in cash feels safe, it fails to compensate for the impact of inflation. Inflation is the ‘silent killer’ of savings. It slowly erodes the purchasing power of your money. Cash returns are less likely to exceed inflation than equity returns and investing too conservatively dramatically depresses long-term wealth creation, as shown in Figure 2.

So, despite the notion that growth assets are risky, a bigger risk is being too conservative. Maintaining exposure to growth assets over an appropriate time horizon can mitigate the destructive effects of inflation and ensure a more successful investment journey.

Look ahead, not behind you, when making investment decisions – Kim Deane

Investing seems to be the only space where we like to buy things when they are priced at a premium and sell things when they go on sale. This peculiar phenomenon is largely driven by ‘rear-view mirror’ investing, one of the most common investment mistakes to make. We scrutinise our most recent experience in the market and extrapolate this into the future. We seem to believe that what performed well in the past will continue to go up, and what disappointed will never recover. If this was the case, investing would be easy. Unfortunately, although hindsight might be 20/20 vision, investors repeatedly destroy value by buying high and selling low in their attempt to time markets, asset classes or investment managers.

Wise investors know that the fundamentals (future cash flows and the price you are asked to pay for it today), not past performance, will dictate future returns. Ultimately, regardless of asset class, investment manager or timeframe considered, making future investment decisions based on what has occurred in the past is a sure way to destroy value. Focus on the fundamentals and stick to your investment plan!

Investing is a team sport – Anton Pienaar

Imagine Rassie Erasmus picked a team consisting of 23 Cheslin Kolbes or 22 Pieter-Steph du Toits. Both are regarded as the best players in their respective positions in the world, but a team made up of only players with their attributes would not do well. Who will kick the penalties if you only have Pieter-Stephs? How will the scrum perform with 15 Cheslins?

The same goes for investments. It might seem like a good idea to own only the asset classes and funds that are on ‘top form’ and performed well in the recent past. Many investors currently choose to invest only in income and global funds – the recent winners – but this is a similarly flawed response as picking a team full of Kolbes.

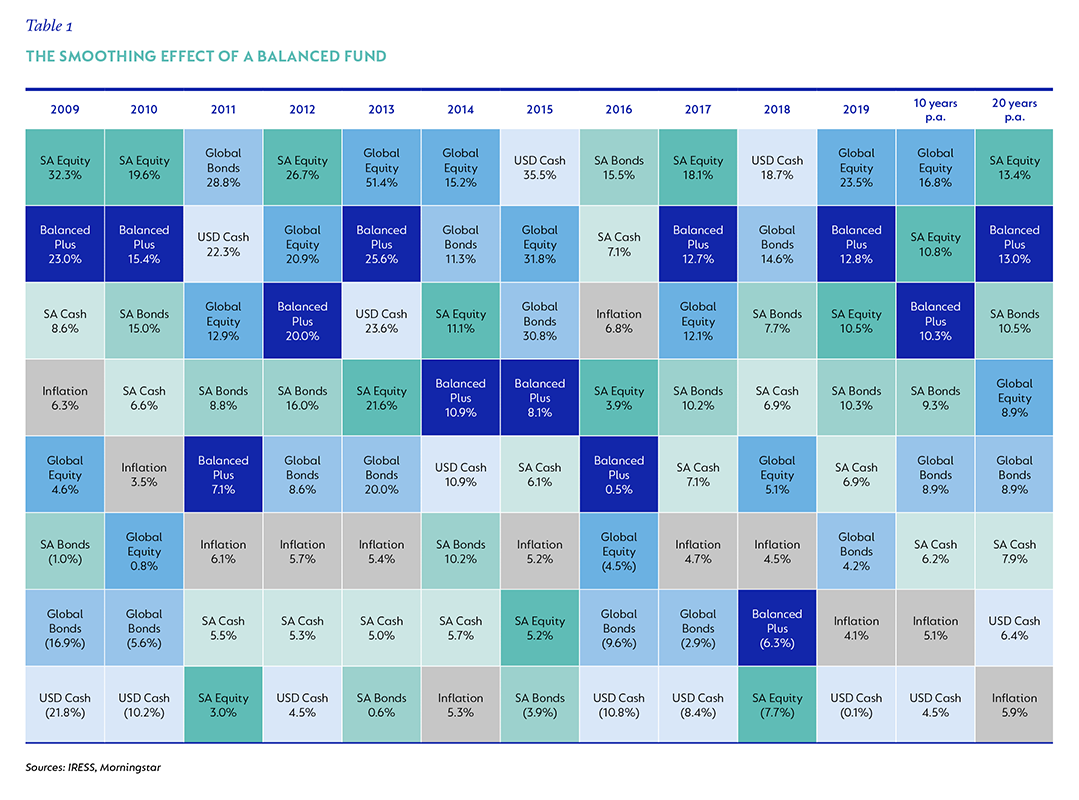

Table 1 shows how different asset classes dominate from year to year, making the chasing of past winners a poor strategy. Rather invest in a well-diversified balanced fund. More diversification means you will never be in the best or worst fund category in any given year, but the reduced volatility makes it easier to stay the course.

Spending time choosing the right fund is an important step in building wealth – Sally Prins

We all know the most powerful ally in wealth building is compounding. We are taught from an early age that compounding is the eighth wonder of the world and the only free lunch in investing. But for compounding to do its job, we need to remain invested.

A study done in the US a few years ago showed the impact of switching unit trust funds. Investors earned half the return of the actual funds they were invested in due to the timing of frequent switching between funds. Instead of allowing your money to compound, wealth is often destroyed as you move from one fund to another, as you are at risk of selling a portfolio of cheaper assets to buy a portfolio of more expensive ones. This can be avoided by doing work upfront to make sure you choose the right fund that suits the amount of risk you are willing and able to take, coupled with the amount of time you want to remain invested.

Do the research, select the fund and stay the course.

How much money do I need to retire? – Bernard Wessels

It depends on how much income you need and for how long. Assuming a sustainable withdrawal rate of 5%, a R500 000 annual income requirement will require a capital base of R10 million (in today’s terms). If you plan to retire in 30 years’ time and you assume inflation in South Africa will average 4.5% p.a. over this period (the midpoint of the South African Reserve Bank’s inflation target range), you will require a capital base of R37 million. This would provide an annual income of approximately R1.9 million in 2050, which is equivalent to the R500 000 annual income requirement today.

The next step is to ask what amount should be invested today to accumulate R37 million in retirement capital. Let’s assume a well-diversified, multi-asset fund, such as the Coronation Balanced Plus Fund, will achieve returns of inflation +5% over the next 30 years (a total return of 9.5% per annum for 30 years). Doing a simple present value calculation, the amount to be invested today to accumulate the required capital base of R37 million upon retirement is only R2.4 million. Assuming a 35-year period until retirement, this amount reduces to approximately R1.5m.

Compounding over long periods ‘bought’ investors the difference between the R10 million required today to produce a R500 000 income and the roughly R2.4 million or R1.5 million required today to grow to the required capital base in 2050. For most retirement plans to work, it is paramount that investors understand, appreciate and capture this long-term benefit of compound growth.

Nothing lasts forever – Mmaba Molefe

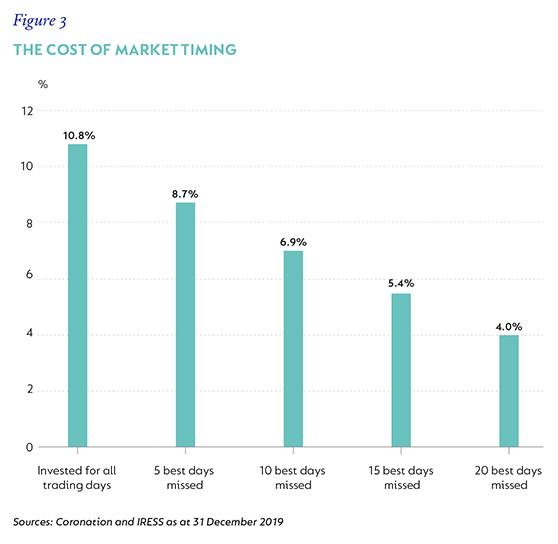

If you have lived long enough, you would know that everything ends. Whether good or bad, nothing lasts forever. Even though we know this to be true, when tough times hit, we immediately feel like it has been going on for a lot longer than it has and we think it will extend into the future, which makes us overly fearful. We therefore feel the need to act quickly, which is sometimes to our detriment. What we can learn from the last decade is that when things are all doom and gloom, have patience and wait; things will change. This is the biggest challenge we face as investors when returns are low – we struggle to sit tight and not do anything to our investments. We want to sell, and we end up selling low just to buy high later. The results can be pronounced, for example, for the last 10 years ending 31 December 2019, the JSE gave you a 10.8% annual total return, but if you missed only the five best days in those 10 years, your return would have been 8.7%, and 4.0% if you missed the best 20 days.

As tough as it may seem, when investing long term, you need to learn to tune out the short-term noise and be patient, because nothing lasts forever.

Think long term: which investor do you want to be in 2030? – Naledi Makiwane

South African growth assets disappointed over the last five years. As a result, more conservative domestic funds delivered better return outcomes than those with more exposure to the riskier asset classes. In response, many disappointed investors moved money out of multi-asset funds and into income funds. This switch was return-eroding in 2019, as the timing of reducing exposure to growth assets coincided with an improvement in equity returns.

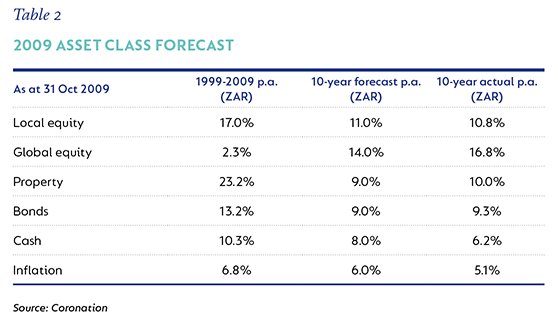

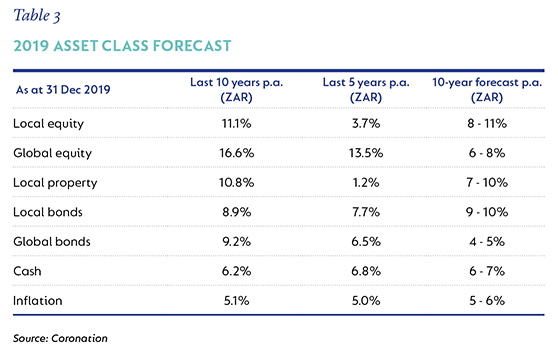

We regularly publish our expected return forecast, comparing the actual return produced by the various asset classes over the previous decade to our expected returns over the next decade. Table 2 shows our forecast towards the end of 2009. Our current forecast, as at 31 December 2019 (a decade later) is presented in Table 3.

The thinking behind our forecasts is informed by the understanding that what you see through the rear-view mirror is different to what you see through the windscreen. The core principle is that higher prices today mean lower returns in future, while lower prices today mean higher returns in future.

As tempting as it may be for South African investors to be conservatively positioned anchoring off the last five disappointing years, we should challenge ourselves to look forward, not backward.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter