South Africa - Personal

South Africa - Personal

INVESTOR NEED: LONG-TERM GROWTH

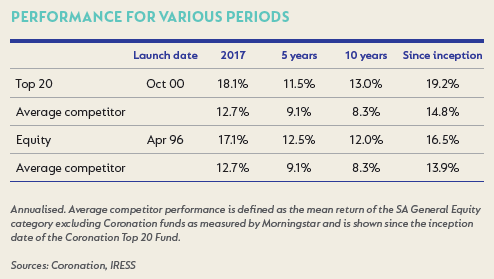

Domestic general equity funds

Domestic equity markets delivered good returns in 2017, reversing the lacklustre performance of the past few years. The FTSE/JSE Capped All Share Index returned 18.1% for the year and 6.5% in the fourth quarter, compared to an annualised 8.9% over three years. The return in US dollar terms was 30.6% over the year as the rand strengthened, reflecting a positive shift in sentiment on the back of the ANC elective conference outcome.

In addition to the positive currency response, domestic shares rallied strongly as short positions were closed and investors tried to hurriedly gain exposure. This was very positive for our holdings in financial stocks such as Nedbank and Standard Bank, and the retail exposures held via Woolworths and Spar. We took this opportunity to lighten some of our pure domestic exposure. While we agree that the outcome of the elective conference was net positive for SA, structurally the economy faces major challenges which are likely to keep a dampener on growth. As a result, we believe that many domestic shares now look quite expensive relative to their growth prospects.

In particular, the past quarter’s rally in domestic banks (+28%) is cause for review, with higher earnings expectations being priced in. While slow advances in growth over the last few years may accelerate, a benign credit cycle leaves little room for credit loss improvements. We have adjusted position sizes to reflect a reduced margin of safety.

A detractor to performance was Frankfurt- and JSE-listed discount retailer Steinhoff, which announced that its CEO would be stepping down and that its financial statements could not be released due to what appears to have been a number of years of misstatement of its audited accounts. For a detailed analysis of our position, please click here.

Over the past year, the Coronation Equity fund benefited from holdings in global businesses including JD.com, 58.com and Porsche. 58.com is a Chinese online classifieds player operating in a growing marketplace as the business drives penetration into lower-tier Chinese cities, expands advertising services to merchants and gains traction in used goods markets. Growing scale and dominance should support margin expansion. JD.com is a Chinese online retailer similarly benefiting from rapidly growing demand as it expands product ranges and invests in its infrastructure and fulfilment services. The vast domestic market with its large number of highdensity cities creates longer-term potential for a very profitable business and the company continues to gain scale and market share.

Calendar 2017 was a relatively robust year for commodity prices, with most strengthening as Chinese demand remained resilient. Supply remained constrained as miners persisted with disciplined allocation of capital and Chinese environmental regulation capped domestic supply. While higher commodity prices have reduced the margin of safety in resource valuations, we maintained a reasonable exposure and have seen contributions to full-year performance from a number of holdings

We enter 2018 with a number of compelling holdings in the portfolios that we believe will continue to deliver strong results in the years ahead and support investor returns over the medium to long term.

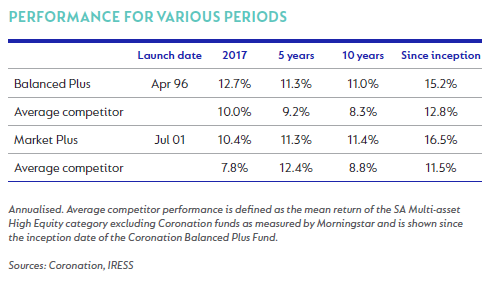

Multi-asset class funds

Over the longer term, significant offshore exposure remains a meaningful contributor to the funds’ performance.

The strong run in global equity markets continued into the quarter, with a quarterly US dollar return of 5.7% (MSCI All Country World Index) supporting the 12-month number at 24.0%. Major markets were broadly strong across the developed and emerging world, with both the US and eurozone reporting healthy growth. This was achieved despite political tensions continuing to boil under the surface – North Korea’s ongoing development of its nuclear agenda, alleged Russian interference in US politics and a tumultuous Middle East.

As the economic outlook for most markets remains good, with Europe, Asia and the US still showing very positive underlying growth metrics, we do not believe we should be underweight equities, but given high valuation levels it is no longer prudent to maintain a big overweight position. Given the strong run in global markets and continued political uncertainty, we have deemed it prudent to trim back these holdings.

Rand strength and a rally in domestic assets meant the large offshore holdings and limited exposure to government bonds detracted from performance in the quarter.

Within the domestic portion of our equity allocation, the majority of our exposure remained to companies with significant operations offshore. The main driver behind this remains the outlook for tepid growth locally and the expensive ratings of many domestic stocks. The strong rally in domestic stocks after the outcome of the ANC

elective conference was not unexpected, but we remain firm in our belief that it is unwarranted, given the massive challenges the local economy faces. The fiscal position is dire and the low productivity of the workforce is unlikely to change given poor educational outcomes. We have taken advantage of the recent run in domestic stocks to lighten our exposure to these equities at what we think are optimistic price levels.

A position in Steinhoff was also a detractor from our performance in the last quarter, as was our very low exposure to government bonds, which saw a very strong rally at the end of the year. The rally presented an opportunity to further reduce our exposure as the domestic bond market faces a number of challenges in the year ahead. SA’s dire fiscal position will require much greater funding, especially as the parlous position of state-owned enterprises’ finances becomes more evident. With debt to GDP spiralling ever higher, worsened by the prospect of free tertiary education, we do not believe current bond yields are sufficient to reward investors. As our debt rating moves to junk status across all rating agencies, we do not see the potential pool of investors getting any bigger. Instead, it will shrink. Importantly, this is happening in an environment where we see government bond yields in developed countries starting to rise, which will put further pressure on domestic bond yields.

Offsetting our low domestic bond position has been our high weighting in domestic property. While domestic property performed better in the last quarter, it has not yet responded to the election of Cyril Ramaphosa as ANC president to the same extent as the bond market. Yields on domestic property stocks remain very attractive, with many in double digits, with the prospect of further earnings growth. We remain overweight this particular asset class, with expectations of decent returns before any capital growth.

Within the offshore component outside of equities, we are also very underweight bonds, with the exception of a few high-yield opportunities where we believe the credit spreads will more than compensate for adverse yield movements. We have increased exposure to property, adding to European retail landlords and, more recently, to a number of large US retail property owners where yields are looking very attractive and the underlying properties are high quality and defensive.

Given the current structure and fund holdings of the funds, we believe we are well positioned to continue to deliver benchmarkand inflation-beating returns in the future, in line with our longterm track record.

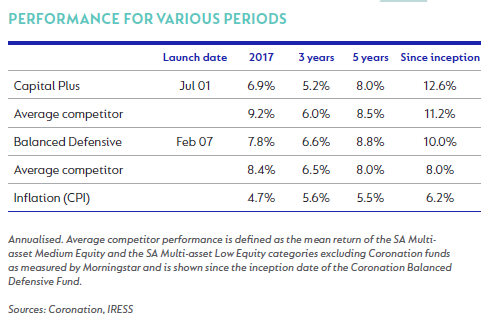

INVESTOR NEED: INCOME AND GROWTH

Multi-asset class funds

Over the course of the year, the biggest contributors to the portfolios’ performance were Naspers, Standard Bank, Anglo American and global equities. However, the strength in the rand towards year-end had a negative effect on performance, as it impacted the value of the funds' offshore holdings totalling 25% of portfolio. Another detractor was Steinhoff, although the impact of its collapse was not crippling.

Listed property company Intu is a stock we have held for many years in the belief that the value of its underlying portfolio of highquality shopping centres far exceeded its market capitalisation. Our view was supported by rival property company Hammerson’s offer to buy Intu at a large premium to its then-current price. The combined portfolio of Hammerson and Intu will make it the largest holder of prime retail shopping centres in the UK. We further believe the Hammerson management team can unlock significantly more value for shareholders over time. As such, we support the buyout enthusiastically.

We were very active in the bond market over the quarter, using the market’s disappointment in the Medium Term Budget Policy Statement to add to government bonds at very attractive yields, and therefore enjoyed the sharp improvement in yields subsequent to the ANC’s elective conference.

Looking forward to 2018, the market will be focused on how Mr Ramaphosa will lead the ANC and, in particular, for how long Jacob Zuma will remain president of the country and therefore in control of key cabinet appointments and government policy. In our view, the deeply divided top six officials of the ruling party and its national executive committee will make it difficult for the new president to act decisively. We think the markets have been too euphoric in its assessment of recent events and expect some retreat in those market sectors that were so buoyant in December.

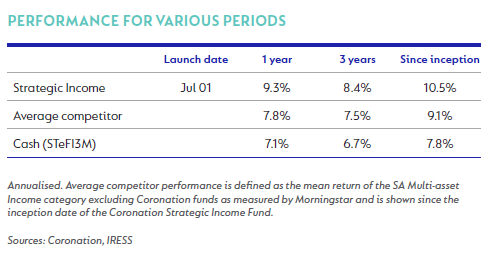

INVESTOR NEED: IMMEDIATE INCOME

Income fund

The last quarter of 2017 was particularly eventful in the local bond market. Following the poor Medium Term Budget Policy Statement in October, when SA’s fiscal deterioration became a reality, the local 10-year bond sold off aggressively, from 8.6% to a high of just above 9.5%. As we have been highlighting for some time, these higher levels better reflect the underlying risks in the local economy, given the policy and political backdrop. Up to the ANC elective conference in December, SA bonds spent most of the quarter at levels of around 9.25% to 9.5%. With Mr Ramaphosa emerging as the new president of the ANC (and possibly the country), the local bond market rallied down to close the year at levels of 8.59%.

Before December, there were expectations that bonds would underperform cash for the year, but the All Bond Index ended 2017 up 10.2% (gaining 5.66% in December alone). This is significantly above the performance of cash and inflation-linked bonds, which returned 7.5% and 2.8%, respectively. The fund has continuously used any spike in yields as an opportunity to add selective exposure to the longer area of the bond curve (more than 12 years) at levels of around 10.25% to 10.50%, given its attractive return prospects relative to cash over the longer term.

The SA economy could be at a key turning point if the newly elected ruling party leadership is able to push through muchneeded growth reforms, stabilise ailing parastatals and restore confidence in the economy. SA’s growth could receive a short-term boost from inventory renewal as corporate SA starts to spend again after a year-long hiatus. Inflation will remain well behaved, with a chance of further downside surprises adding to the case for a lower repo rate. SA government bonds should benefit from this renewed optimism and contained inflation. However, at current levels, they are only at fair value, and with exclusion from the Citigroup World Government Bond Index still a possibility, we choose to be neutral on SA government bonds, looking instead for more attractive levels to extend duration further.

The SA listed-property sector gained 4.21% in December, bringing its return for the year to 17.86%. From our recent interactions with many of the listed property companies, it is clear that poor economic conditions have started to affect the local property market. Still, we remain confident that the sector offers selective value. The changes in the property sector over the last decade (including the increased ability to hedge borrowings and large offshore exposures) have rendered the yield gap between the property index and the current 10-year government bond a poor measure of value. On the surface, it appears quite stretched. However, if one excludes the offshore exposure, the property sector’s yield rises to approximately 8.3%, which compares very favourably to the benchmark bond. The fund maintains holdings in counters that offer strong distribution and income growth, with upside to their net asset value valuations. In the event of a moderation in listed property valuations (which may be triggered by further risk asset or bond market weakness), we will look to increase the fund’s exposure to this sector at more attractive levels.

We remain vigilant of risks emanating from the dislocation between stretched valuations and the underlying fundamentals of the SA economy. However, we believe that the fund’s current positioning correctly reflects appropriate levels of caution. The fund’s yield of 8.98% remains attractive relative to its duration risk. We continue to believe that this yield is an adequate proxy for expected fund performance over the next 12 months.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter