South Africa - Personal

South Africa - Personal

Personal finance

We are bullish yet patient

Leaning into a once-in-a-decade dislocation between price and value.

The Quick Take

- The investment opportunity set is large, regardless of where you look

- The local and global market sell-off has created a rare valuation opportunity for long-term investors

- We have leaned into these dislocations between price and value, and are being patient

- Being invested before the turning points arrive ultimately rewards the long-term investor

When looking back at the first half of 2022, it would be very hard for investors to buy into their fund manager’s optimism about future return prospects. Yet, regardless of where we look across local or global markets – the opportunity set is large. And notwithstanding the many known risks and increasingly unstable world we live in, our conviction levels are high that, with a bit of patience, investors should see strong investment outcomes a few years down the line.

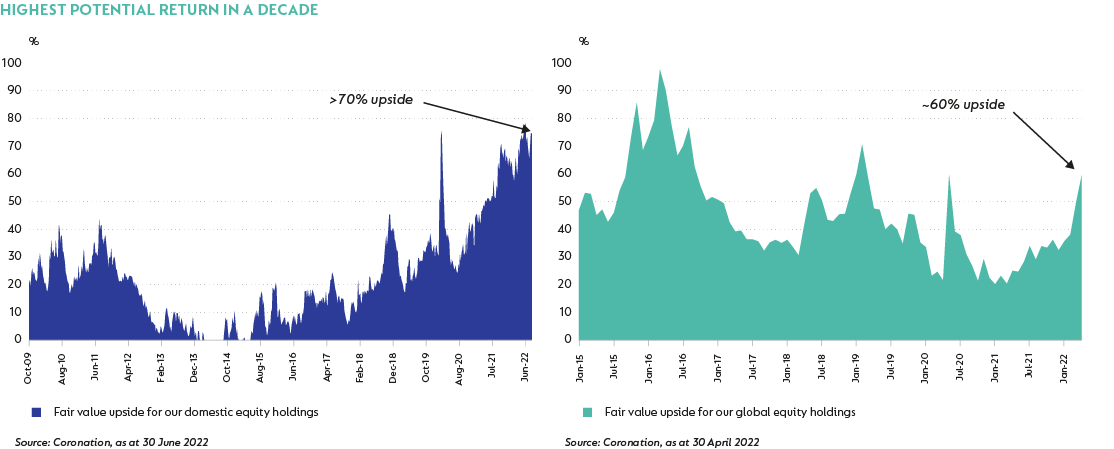

SWIMMING IN A SEA OF OPPORTUNITY, BOTH LOCALLY AND OFFSHORE

Within the local equity markets, five years of recessionary conditions have created valuation levels that are on par with those experienced in the aftermath of the Global Financial Crisis (end-2008/beginning of 2009). As a result, we’ve seen an incredible depth and breadth of value emerging in JSE-listed shares. Unusually, we are finding value in all three major segments of the local market: the resources sector, SA Inc. shares (e.g. financials, insurers, defensive retailers) and the global shares that happen to be listed on the JSE (such as ABInbev, British American Tobacco, Naspers/Prosus and Quilter).

Likewise, after the very indiscriminate sell-off in global equity markets, we also see opportunities across the spectrum. Examples include quality businesses such as Adobe, one of the ultimate software-as-a-service models, that has effectively halved in price, despite the company not experiencing any fundamental changes. The same applies to Nvidia, arguably the best semiconductor business in the world, where its share price too halved, more or less, providing us with an attractive entry point.

Global share price declines have been more spectacular in the long duration growth sector. Our global equity portfolios typically had low single-digit percentage exposure to this sector early in 2022, but we’ve since upped that in response to the acceleration in the sell-off in the second quarter. Our exposure, however, is limited to what we believe are the best long-duration technology businesses that are trading at much less demanding valuation multiples, and despite typically being in a very different part of the capital cycle to businesses that are forced to raise capital in the current more difficult environment. We are also finding opportunities in many high-quality consumer discretionary businesses that are priced for a pending recession, including Capri (the owner of brands such as Versace, Jimmy Choo and Michael Kors) and China internet, where we believe the opportunity remains attractive in our core holdings - Tencent (via Prosus/Naspers) and JD.com.

WE ARE FULLY INVESTED IN EQUITIES

The sell-off in both local and global markets has, in our view, created a once-in-a-decade type moment in terms of the valuation opportunity (as is clear from the two graphs below). As a result, our multi-asset portfolios are fully invested in equities. As an example, our flagship pre-retirement fund Coronation Balanced Plus has ~75% in equities (its maximum limit) and holds almost no cash.

NOT THE TIME TO SIT ON THE SIDE LINES

Owning portfolios that are filled with assets that recently declined in price are never comfortable and goes against one’s natural instincts. Yet, having navigated many unnerving market events for close to 30 years, we know that the only way to grow our investors’ savings into real long-term wealth is to focus on the price we pay for an asset. This means that we need to lean into these dislocations between price and value when they occur and take advantage of the opportunities on offer.

CAUTIOUSLY OPTIMISTIC

Markets often turn when you least expect them to and before the concerns that previously led asset prices to decline have been fully resolved. We saw this again recently. After a tough June, when already depressed markets declined further in response to the highest US rate hike since 1994, markets have recovered strongly in July and August, despite another similarly sized US rate hike during this period.

Sentiment often changes with incredible speed and little warning. Yet, being invested before those turning points arrive are the key moments that ultimately end up rewarding the patient long-term investor.

Disclaimers

SA retail readers

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter